Director,

T.E.(Terry)

Manning,

Schoener 50,

1771 ED

Wieringerwerf,

The Netherlands.

Tel:

0031-227-604128

Homepage:

http://www.flowman.nl

E-mail:

(nameatendofline)@xs4all.nl : bakensverzet

and

"Money is not

the key that opens the gates of the market but the bolt that bars them"

Gesell, Silvio The

Natural Economic Order

Revised English edition,

Peter Owen,

“Poverty is created scarcity”

Wahu Kaara, point 8 of the Global Call to Action Against Poverty, 58th

annual NGO Conference, United Nations,

05.22

PRINCIPLES OF THE MICRO-CREDIT STRUCTURES TO BE CREATED.

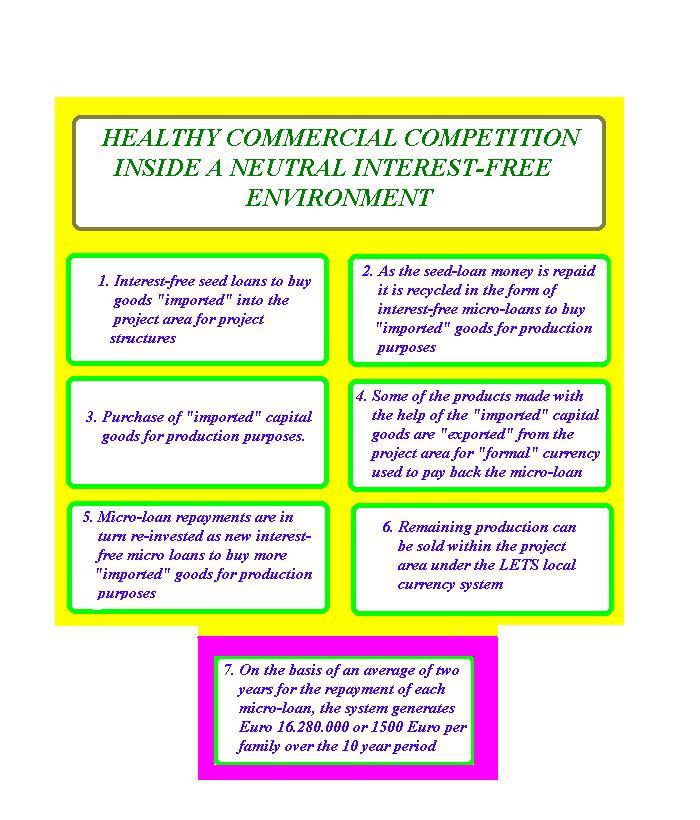

Multiple re-cycled

interest-free micro-credits will provide formal money needed to develop local

production capacity. The rest of the development will be done with the LETS

systems.

The capital available

for re-cycling in the form of micro-credits is made of:

a) Part of the initial seed money until it is needed for the project.

b) Seed loan repayments.

c) Micro-credit repayments.

d) The long term maintenance fund.

e) The system capital replacement fund which will be built up after the ten

years' seed loan has been fully repaid.

For instance, a woman

may need a sewing machine to be able to make clothes. She will need

"formal" currency to buy the sewing machine. That money will be

available in the form of an interest-free micro credit. She will sell outside

the local LETS system some of the clothes she makes to earn the

"formal" money she needs to repay her loan. The rest of the clothes

can be sold within the local currency LETS system.

As she repays her

loan, the repaid capital can be loaned again for another interest free

micro-credit project, so the available seed money repeatedly re-circulates

within the local economy.

The micro-credit

structure will provide each family, on an average, with a total of at least

Euro

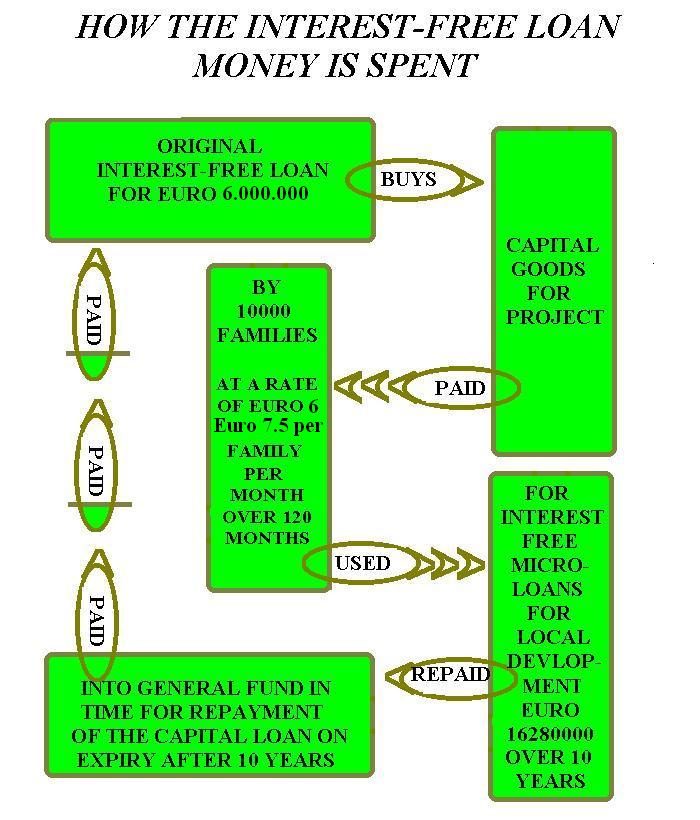

Illustration of the micro-credits system.

How the original grant of seed-loan is used.

Illustration of the interest-free loan cycle.

MICRO

CREDIT SYSTEM STRUCTURES

The Cooperative Local Development Fund will manage formal currency funds

necessary for running the project, acting on instructions of the project

coordinator given on receipt of the indications received from those responsible

at tank commission level. The funds do not belong to the Fund, which will

intervene only in the practical management and transfer of the funds. The

decisions are taken by the users' structures set up under the project. The Fund

formally belong to the users. Where seed funding is by way of an interest-free

loan, the seed money reverts to financing parties at the expiry of the 10

years' interest-free credit term. The interests of the financing parties are

protected by their representatives (if any) nominated to the auditing

commission, auditing procedures, and the on-going monitoring carried out by the

project NGO, who will be invited to participate in the workshop.

The Cooperative Local

Development Fund will be formed during the capacitation workshop.

The services of the

Fund will be paid in local LETS monies at a fixed rate per transaction to be

set during the workshop. The Fund can then use its LETS credits

to pay its staff, and

if it so wishes, to purchase goods and services inside the project area and

sell them for formal money outside the project area to cover any formal money

costs.

Micro-credits will be

granted at tank-commission, well-commission, and central management

levels. How much will be distributed at

each level will be decided during the capacitation workshop.

Loans at tank

commission level will be handled during a fixed agenda-point at each

tank-commission meeting, during which monthly contributions and loan repayments are collected, and new

loans distributed. Credit balances are

transmitted to the local well-commission.

Each tank commission has a micro-credits delegate and a substitute.

Loans at well

commission level will be handled during a fixed agenda-point at each

well-commission meeting, during which loan repayments are collected, and new

loans distributed. Credit balances are

transmitted to the central management group. Each well commission has a

micro-credits delegate and a substitute.

Loans at project level

will be handled during a fixed agenda-point at each micro-credit management

meeting, during which loan repayments are collected, new loans distributed, and

statistics and policy decisions discussed.

Rules

for the organisation of the Micro-Credit meetings will be set up during phase

two of the various project applications with the full participation of the

beneficiary communities. These rules must lay down the general principles

behind the systems. These would, for example, presumably include the following

principles:

1) All loans are to enable the beneficiary to extend

his/her LETS and formal currency income by producing more goods and services

2) The goods and services must benefit the general

interests of the community and encourage exchanges under the local LETS

systems.

3) Some of the goods and services must be saleable

outside the LETS systems to earn formal currency to repay the micro-loans.

4) The Micro-Credit loans must promote the rapid circulation

of formal money within the beneficiary communities. For example, using formal

currency to build a clinic or hospital would not qualify for micro-credits

because the capital invested cannot be re-circulated. On the other hand, buying

equipment for testing water quality (foreseen in the Model) would qualify, as

the formal currency cost can be recovered by charging in formal currency for

water analyses conducted for users outside the project area until the micro

loan has been repaid.

5) Special priority will be given in the first

instance to micro-loans to start the collection and transport of compost,

urine, and grey water, and establish the recycling centres that will collect,

store, and export non-organic waste products from the project area. The formal

currency micro-loans will be recovered by sale of the waste outside the project

areas.

6) Beneficiaries will provide

at least 3 family members and/or friends

to guarantee the timely repayments of the micro-credit loans.

7) Beneficiaries will provide

due backup for their micro-credits to ensure continuation of their investments

and repayments in case of disability or death caused by accident or illness.

(With thanks to Ms Angela Eikhout,

Eindhoven, Netherlands for her contribution.)

Some do’s and don’ts.

Indian micro-finance banker Harishchandra

Sukhdeve wrote the following contribution to the Micro-Finance Gateway

resources list on 26th September 2007. His words have been edited with his

permission for inclusion in this Model.

“Group formation and its

nurturing in a right way is a key to not only poverty alleviation but also

conflict resolution and women’s empowerment.

Women’s groups are found to

be more efficient and professional.

However, while forming groups

certain Do's and Don'ts are must.

A list of do’s

01.Inter act with people

through village level meetings.

02.Encourage groups to hold

regular meetings.

03.Educate them about

community living, public hygiene, education, nutrition, etc.

04.Proactively pass on all

legitimate benefits to farmers/villagers.

05.Ensure trouble-free timely

finance to farmers as well as other group members.

06.Promote farmers groups for

collective farming.

07.Promote share-croppers'

groups.

08.Ensure/facilitate

appropriate training for entrepreneurship development.

09.Encourage innovation and

self regulation by the groups.

10.Encourage inclusiveness.

11.Encourage young volunteers

to promote the culture of the groups.

A list of don'ts:

01.Do not allow groups to be

formed of the same family members except for farmer’s groups for collective

farming.

02.Do not allow groups to

finance to non-members.

03.Do not allow one person to

become member of more than one group.

04.Discourage control of

groups by any single person.

05.Do not try to regulate the

groups too much as this may hamper their ingenuity,

06.Do not stretch

hand-holding for too long a period. ”

Micro-credit

workshop.

One Moraisian

workshop will be held to prepare the Fund structures.

Indicative

participation

The Moraisian

trainers.

A member of the project coordination team.

General consultant.

2 Representatives of the project NGO.

Representative of the Finance Ministry.

Representative of the Rural Development ministry.

At least 5 observers (possible coordinators for future projects).

At least 6 qualified persons, 3 indicated by the NGO and 3 by the project

coordinator.

400 persons, indicated by the tank commissions, interested in participating

with responsibility for credit arrangements at tank commission, well-commission

and central management levels.

Duration of the

workshop: about six weeks.

The Workshop will be

expected to produce the following structures:

a) Definition of the

social form

- statutes

- rules

- professional and administrative structures

- financial aspects

- relations with the LETS local money systems

b) Physical aspects

- land

- office

- safety

- communications

c) Financial aspects

(Definition of initiatives at each structural level. How much money is to be

distributed at each level?)

- funding of

initiatives at general project level (recycling structures, important productivity

initiatives, public works)

- funding of initiatives at intermediate, well commission, level

- funding of initiatives at local tank commission level

- funding of socially based initiatives (clubs, interest groups etc)

- traditional banking activities

a) Central structure

b) De-centralised

structure

- Preparation operators

- Meetings at tank commission level

c) Coordination

- With LETS structures

- With tank commissions

- With project coordinator

d) Financing of

specific projects

- Relations with financiers

e) Communications

structure

-Vertical, at project level (project coordinator, transactions operators, tank

commission level operators, end users)

Commercial, radio, website

THE MICRO-CREDIT

FUND AND EMERGENCIES.

How would the cooperative micro-credit fund work in

conditions of extended drought or other emergencies? The project creates

social, financial, productive and service structures. These structures are

permanent. They are run by the management cooperative set up for the purpose,

and they remain in place as long as people continue to live in the project

area. This is so even where inhabitants return to the project area after a

temporary migration outside of the project area for survival purposes.

The situation with the Cooperative Local Development

Fund at any given point of time depends on the decisions taken by those chosen

to manage it. It is reasonable to expect

that in times of extended drought and similar crisis conditions that families

have difficulties making their monthly contributions to the Fund and that

beneficiaries (and their guarantors)

have problems repaying the micro-credit loans they have received.

The micro-credit fund is cooperative. Should a point

be reached where as a result of Act of God outside the control of the parties,

families are unable to make their monthly payments or beneficiaries are unable

to repay their debts, the managers of the Fund may decide to waive payments of

contributions meantime or to leave it up to the families whether to make their

payments or not. In any case the Fund would remain intact. It would continue to be systematically recycled

interest-free. But the total amount in the Fund would not continue to increase

as it would otherwise have done. In case of projects financed by interest-free

ten year credits, the situation could arise that the monies collected in Fund

turn out to be insufficient to pay the whole of the original loan back at the

close of the first ten year period. On the other hand, where a productive

period follows one of extended drought or crisis, the Fund management could

require an increase in the monthly contribution of families to reinstate the Fund

in time for repayment at the end of the ten year period.

In times of drought and scarcity, beneficiaries and

those guaranteeing them may also face great difficulty in making repayments of

their micro-credits. What happens in such a situation depends on the decision

of the Fund management which is chosen by the Central Committee of the Project.

Logic would suggest in such situations to grant more time to beneficiaries and

those guaranteeing them to make their payments. This would lead to a slowing

down in the rate of recycling of the monies in the funds, and therefore to a

(temporary) slow-down in the rate of development in the project area. However,

the capital in the Fund would still remain intact.

Yet another situation which might arise is that the drought

or other environmental condition in the project area is so serious that the

Fund management team decide to gradually reimburse the monies in the Fund to

the inhabitants to supplement their extra costs for purchase of drinking water

or food supplies for survival purposes. In practice this means that as monies

are (with great difficulty) repaid by beneficiaries into the Fund, the

repayments are for a period of time re-distributed amongst all of the

inhabitants, or amongst the most needy. The cooperative local development fund

would in this case operate as an Emergency Fund. The consequences of this use

would depend on the reactions of donors and funding organisations and on the

real and just possibilities of subsequent recovery taking the cooperative nature

of the Fund into account. In the worst imaginable situation, the Fund might

find itself without any capital left. However, even in that case the structure

of the Fund would remain in place. Upon improvement in the climatic situation,

families would recommence making their monthly contributions to the Fund, which

would build up to full strength again after ten years.

Refer also to section 4.15 The effects of inflation on the Cooperative

Local Development Fund and gift content and to section 4.16 Project insurance and forfeit in the form of

gift in case of loss of capital structures.

Next file :

05.31 Units for the production of items made

from gyspum composites.

Back to:

05.21

Interest-free cooperative local money structures.

{kind=link}

{kind=link}