NGO

Another Way (Stichting Bakens

Verzet), 1018 AM Amsterdam, Netherlands.

01. E-course : Diploma in Integrated

Development (Dip. Int. Dev.)

Edition

04:13 December, 2010.

Edition

15 : 18 October, 2014.

Quarter

2.

SECTION B :

SOLUTIONS TO THE PROBLEMS.

Value: 06

points out of 18 .

Expected work

load: 186 hours out of 504.

The points

are finally awarded only on passing the consolidated exam for Section B : Solutions

to the Problems.

Fourth

block: The structures to be created.

Value : 03 points out of 18

Expected work load: 96 hours

out of 504

The points

are finally awarded only on passing the consolidated exam for Section B :

Solutions to the Problems.

Fourth

block: The structures to be created.

Section 3:

Financial structures.[24 hours]

20.00 hours :Financial structures.

04.00 hours : Preparation report.

Section 3:

Financial structures.[24 hours]

20.00 hours :Financial structures

: analysis.

1. The basic concepts - introduction.

[ 2.5 hours]

2. The basic concepts – more

details. [ 2.5 hours]

3. The local money systems -

introduction [ 2.5 hours]

4. The local money systems –

more details. [ 2.5 hours]

5. The interest-free

micro-credit systems -

introduction.[2.5 hours]

6. The interest-free

micro-credit systems -

more details.[2.5 hours]

7. The cooperative purchasing groups -

introduction. [2.5 hours]

8. The cooperative purchasing

groups – more details. [2.5 hours]

04.00 hours : Preparation report.

Section 3:

Financial structures.[24 hours]

20.00 hours :Financial structures

: analysis.

5. The interest-free

micro-credit systems -

introduction.[ at least 2.5 hours]

The cooperative interest-free micro-credit structures

provided for in integrated development projects are innovative. They are

complementary to the local money structures covered in the preceding sessions,

under the framework of which they are created. They are fundamentally different

from those described by Nobel Prize winner Muhhamad Yunus in his book Banker

to the Poor, (Public Affairs, New York, 2003) in relation to his Grameen Bank. A good summary of Yunus’s

book is available at Banker to the Poor, The Economist,

Get Abstract, 2007. Yunus

and his work have recently been subjected to a more critical analysis than was

the case in the past. There are reports on

harsh methods for obtaining repayments, high interest rates, and

falsification of default rates, which were often claimed to be less than two

percent. The Brennpunkt programme by the National

Norwegian Television, Oslo,

transmitted its documentary on Yunus Caught in Micro-debt

on November 30, 2010.

The original version, in Norwegian, is available at Fanget i Mikrogjeld.

Suggestions of possible misuse by Yunus of

aid-funds made in the documentary were officially refuted by the Norwegian

government. Nevertheless the film . shows in detail how microfinance works and

its consequences on the borrowers. The Norwegian Minister of Development and

Environment at the time “left the post” at the end of March 2012, and the

Norwegian government “will no longer

finance new MFIs [micro-finance institutions] ” (T.Heinemann, No more financing of MFIs, NRK Brennpunkt, Oslo, 19th June, 2012.)

“There has been a

collective delusion that microfinance and its link to entrepreneurial activity

is a powerful tool to alleviate poverty despite little evidence to show that

this model works.” (Parminder Bahra,

Microfinance

: Is Grameen Founder Muhammad Yunus a

Bloodsucker of the Poor?, The Source, Wall Street Journal, New York, 6 December,

2010.)

In his Ph. D.

thesis Enslaving Development

: An Anthropological Enquiry into the World of NGO, (Chapter 8 pp.

267-303), (Durham University, Durham 2010) M.Mannan

describes how neo-liberal market ideas have come to “colonise” the development

sector in Bangladesh.

“Micro-credit did not do much to improve the well-being of women but released

the elite from their religious and social obligations to help the poor and

women in need” (p. 300).

At p. 286 cites a BRAC client :

“You came to help

us. Why are you charging interest?”

At p. 298 :

“I accepted money

to become rich, but now happiness has disappeared.”

The “cautious” conclusion 1 of a comprehensive review

on microfinance in sub-Saharan Africa reads :

“We conclude that some people are made poorer, and not richer, by

microfinance, particularly micro-credit clients. This seems to be because: they

consume more instead of investing in their futures; their businesses fail to

produce enough profit to pay high interest rates; their investment in other

longer-term aspects of their futures is not sufficient to give a return on

their investment; and because the context in which microfinance clients live is

by definition fragile.” (Stewart, R. and others, What is the impact of microfinance

on poor people? A systemic review of evidence from sub-Saharan Africa, EPPI Centre, Social Science

Research Unit, University of London, London, 2010. ISBN 978-1-907345-04-3.)

The negative effects of

“financial inclusion” of the poor are discussed by M. Bateman in Why Doesn’t Microfinance Work? The

Destructive Rise of Neoliberalism,

Overseas Development Institute (ODI), London,

July 2010. (Book launch presentation). Book : Zed Books, London, 2010. ISBN 978-1-848133327.

“A microfinance

customer is overindebted if he/she is continuously

struggling to meet repayment deadlines and structurally has to make unduly high

sacrifices related to his/her loan obligations”. (Schicks,

J., Over-indebtedness in microfinance

– An empirical analysis of related factors on the borrower level, Université Libre de Bruxelles, Solvay Brussels School of Economics and

Management, Centre Émile Bernheim,

CEB Working Paper 12/017, Brussels, 2012, p. 3.)

Appendix 2 (p. 38) of the Schicks paper lists the

borrower sacrifices and acceptability levels :

“1) Reduce

food quantity/quality (cut down eating)

2) Reduce

education (e.g. taking children out of school)

3) Work more

than usual (e.g. take additional labor, work longer

hours, on Sundays, and when ill)

4) Postpone

important expenses (e.g. for health, housing, business assets etc.)

5) Deplete

your financial savings (e.g. money in the house or in a savings account)

6) Borrow

anew to repay (take an additional loan from another lender)

7) Sell or

pawn assets (e.g. jewelry, cattle, productive or

household assets)

8) Seizure of

assets (MFI takes property by force to make up for missed payment)

9) Use

family/friends' support to repay

10) Suffer

from shame or insults (also gossip about you/exclusion from a contract)

11) Feel

threatened/harassed by peers/family/loan officer

12) Suffer

psychological stress yourself or in your marriage

13) Other

Respondents

ranked the acceptability and frequency of each sacrifice on a scale from 1 to

4.

■

Easily acceptable, Only just acceptable, Not really acceptable, Not acceptable

at all.

■ Once

in past year, 1-3 times in past year, > 3 times but not often, Frequently in

past year.”

Bateman’s

criticisms appear to be taken seriously even in The Micro-Finance

Illusion : The Post 2015 Development Agenda Should Rethink its Development

Approach for Local Financing, Published by the Global Policy Forum through the United

Nations Non-Governmental Liaison Service, New York, 14 February, 2013.

Official approach

to profit-making Micro-credit finance at the cost of the poorest is changing.

As Claire Provost wonders whether the microcredit story was

“a convenient guise, at least for some, to pursue personal gain and other aims”

(The rise and fall of

microcredit, Guardian, Poverty Matters Blog, London,

21 November, 2012.)

Furthermore, “all impact

evaluations of microfinance suffer from weak methodologies and

inadequate data” (Duvendak, M. et al, What is the evidence of the impact

of microfinance on the well-being of poor people?, Report 1912, EPPI Centre, Social Science Research Unit, Institute of

Education, University of London, London, August, 2011 for the Department for

International Development. (ISBN 978-1-907345-19-7), conclusions p. 4). The

authors point out on p. 75:

“Microfinance

activities and finance have absorbed a significant proportion of development

resources, both in terms of finances and people. Microfinance activities are

highly attractive, not only to the development industry but also to mainstream

financial and business interests with little interest in poverty reduction or

empowerment of women, … it remains

unclear under what circumstances, and for whom, microfinance has been and could

be of real, rather than imagined, benefit to poor people.”

Accurate

information on interest-rates applied by micro-finance institutions is not easy

to find.

As one report

wryly puts it : “Collection of data is labor-intensive

and depends on the willing cooperation of micro-lenders who might occasionally

find the publication of their pricing specifics embarrassing. ” (Rosenberg, R. et

al, Microcredit Interest

Rates and Their Determinants 2004-2011, Consultative Group to Assist the Poor (CGAP),

and its partners, Washington, Report 7, June, 2013, p. 4)

Micro Finance

Transparency, Lancaster (PA), however, lists information for 17 countries in [Information on microfinance interest rates] All countries :

Introduction. When accessed on 24th July 2014, the

following information applied to the

major “markets” amongst the 17 countries. There is a wide variation of rates

amongst the lenders. Sometimes, but not always, this depends on the original

source of funding. Funding from the open money market will usually be more

expensive than that provided under aid programmes. In general, the smaller the

loan, the higher the rate of interest. The following shows typical ranges of

variations for small loans. Some rates are much higher still, and have been

discounted.

1. India : 23%

- 40%.

2. Ethiopia: 14% - 38%.

3. Philippines : 20% - 200% (up to

450% for very small loans).

4. Colombia : 25% - 43%.

5. Kenya : 20% - 50% (very small loans

more than 50%)

6. Ghana : 45% - 150% (even more for

very small loans)

7. Cambodia : 3% - 40%.

8. Bolivia : 20% - 70%.

Information is still not available

for many major markets including Bangladesh,

Mexico and Nigeria.

Just how much of a

burden micro-finance in Bangladesh

is is

discussed in detail in D.Hulme and M. Maitrot, Has Microfinance Lost its Moral Compass?, (Brooks World Poverty Institute, Working Paper 205, University

of Manchester, Manchester, August 2014) :

“..the compelling

narrative [in Western media] of the

success of microfinance–of millions of heroic and entrepreneurial women lifting

themselves and their children out of poverty (and into relative affluence)

through small loans and self-employment- is not supported by serious

evaluations of microcredit.” (p.5).

“…for poor

households a small loan from an MFI is the beginning of a long and winding road

of increasing debt and, for some, over-indebtedness (a debt burden that cannot

be serviced from household income). A

majority of poor MFI clients reported through interviews and focus group

discussions extreme livelihood compromises – sending children out to work,

reducing quantity and quality of food and distress sales of essential

productive assets. For some households weekly repayments to multiple MFIs had reached up to US$50 a

week, a staggeringly high figure for people on rural wage rates in Bangladesh (Maitrot, 2013).” (p.7) [Bold added by Stichting

Bakens Verzet]. Other

pressures include those to postpone burying their husband; take children out of

school; and, take loans from other MFIs (to repay the

loans officer’s MFI).” (p.7).

The Hulme and Maitrot paper contains

some 50 references for further study.

J. Ghosh provides a detailed discussion of the problems

related to traditional for-profit and not-for-profit microfinance practices,

especially self-help group (SHG) initiatives in

India, in his article Microfinance and the

challenge of financial inclusion for development, published for the Cambridge Journal

of Economics, 13 September 2013 by Oxford University Press, Oxford, 2013.

MICRO CREDIT SYSTEM STRUCTURES IN

INTEGRATED DEVELOPMENT PROJECTS.

Micro-credit loans

under the Model are interest-free and free from all formal money costs, as they

are managed under the local money systems set up. They offer a viable

alternative to the business-based micro-finance industry.

This section

refers to micro-credit systems in general. The following section 6. Interest-free micro-credit systems : in depth

analysis refers to the actual setting up of the micro-credit structures.

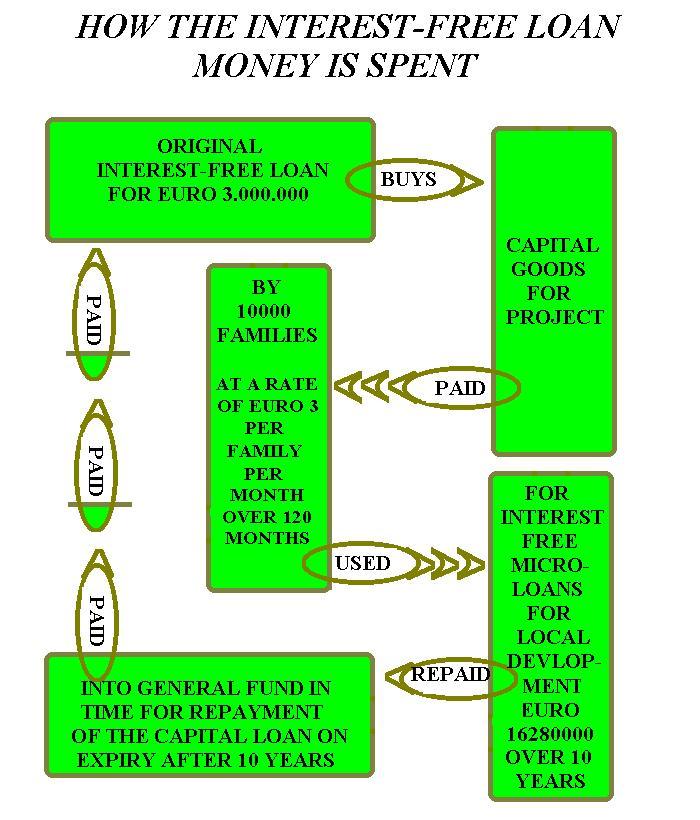

Here is a

drawing showing the interest-free micro-credit loans cycle.

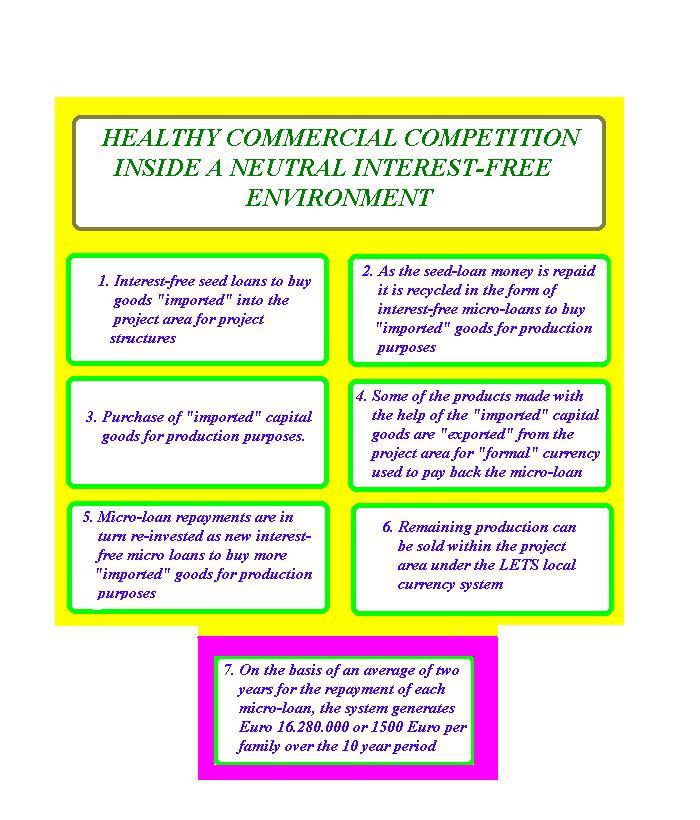

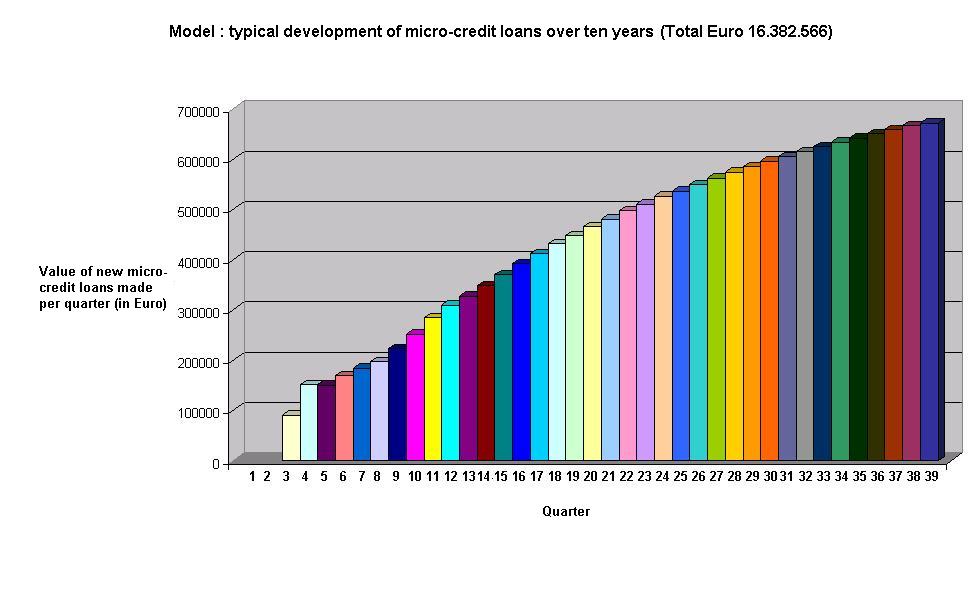

Multiple re-cycled interest-free micro-credits will

provide formal money needed to develop local production capacity. The rest of

the development will be done with the LETS systems.

The capital available for re-cycling in the form of

micro-credits is made of:

a) Part of the initial seed money until it is needed

for the project.

b) Seed loan repayments.

c) Micro-credit repayments.

d) The long term maintenance fund.

e) The system capital replacement fund which will be built up after the ten

years' seed loan has been fully repaid.

For instance, a woman may need a sewing machine to be

able to make clothes. She will need "formal" currency to buy the

sewing machine. That money will be available in the form of an interest-free

micro credit. She will sell outside the local LETS system some of the clothes

she makes to earn the "formal" money she needs to repay her loan. The

rest of the clothes can be sold within the local currency LETS system.

As she repays her loan, the repaid capital can be

loaned again for another interest free micro-credit project, so the available

seed money repeatedly re-circulates within the local economy.

The micro-credit structure will provide each family,

on an average, with a total of at least Euro 1500 in micro-credits for

productivity purposes during each period of operation of ten years.

Illustration of the micro-credits system.

How the original grant of seed-loan is used.

The Cooperative

Local Development Fund will manage formal currency funds necessary for running

the project, acting on instructions of the project coordinator given on receipt

of the indications received from those responsible at tank commission level.

The Fund intervenes only in the practical management and transfer of the funds.

Funding decisions are taken by the users' structures set up under the project.

The Fund formally belongs to the users. In principle, all monies paid into the

fund are contributed by the users themselves. Formal money budget costs (€

30.000) are needed only to physically set the micro-credit system structures

up.

Where seed funding

for a given integrated development project is by way of an interest-free loan,

the seed money reverts to financing parties at the expiry of the 10 years'

interest-free credit term. The money to be repaid is collected in the

Cooperative Local Development Fund and continuously recycled for interest-free

micro-credits until repayment falls due. In that case, the interests of the

financing parties are protected by their representatives (if any) nominated to

the auditing commission and by prescribed auditing procedures. On-going

monitoring will be carried out by the Cooperative for the on-going maintenance

of project structures.

The Cooperative

Local Development Fund will be formed during the capacitation

workshop held in each project area for that purpose.

The services of

the Fund will be paid in local LETS monies at a fixed rate per transaction to

be set during the workshop. The Fund can then use its LETS credits to pay its

staff, and if it so wishes, to purchase goods and services inside the project

area and sell them for formal money outside the project area to cover any

formal money costs.

Micro-credits will

be granted at tank-commission, well-commission, and central management

levels. How much will be distributed at

each level will be decided during the capacitation

workshop.

Loans at tank

commission level will be handled during a fixed agenda-point at each

tank-commission meeting, during which monthly contributions and loan repayments are collected, and new

loans distributed. Credit balances are

transmitted to the local well-commission.

Each tank commission has a micro-credits delegate and a substitute.

Loans at well

commission level will be handled during a fixed agenda-point at each

well-commission meeting, during which loan repayments are collected, and new

loans distributed. Credit balances are

transmitted to the central management group. Each well commission has a

micro-credits delegate and a substitute.

Loans at project

level will be handled during a fixed agenda-point at each micro-credit

management meeting, during which loan repayments are collected, new loans

distributed, and statistics and policy decisions discussed.

Rules for the

organisation of the Micro-Credit meetings will be set up during phase two of

the various project applications with the full participation of the beneficiary

communities. These rules must lay down the general principles behind the

systems. These would, for example, presumably include the following principles:

1) All loans are

to enable the beneficiary to extend his/her LETS and formal currency income by

producing more goods and services.

2) The goods and

services must benefit the general interests of the community and encourage

exchanges under the local LETS systems.

3) Some of the

goods and services must be saleable outside the LETS systems to earn formal

currency to repay the micro-loans.

4) The

Micro-Credit loans must promote the rapid circulation of formal money within

the beneficiary communities. For example, using formal currency to build a

clinic or hospital would not qualify for micro-credits because the capital

invested cannot be re-circulated. On the other hand, buying equipment for

testing water quality (foreseen in the Model) would qualify, as the formal

currency cost can be recovered by charging in formal currency for water

analyses conducted for users outside the project area until the micro loan has

been repaid.

5) Special

priority will be given in the first instance to micro-loans to start the

collection and transport of compost, urine, and grey water, and establish the

recycling centres that will collect, store, and export non-organic waste

products from the project area. The formal currency micro-loans will be

recovered by sale of the waste outside the project areas.

6) Beneficiaries

will provide at least 3 family members and/or friends to guarantee the timely repayments of the

micro-credit loans.

7) Beneficiaries

will provide due backup for their micro-credits to ensure continuation of their

investments and repayments in case of disability or death caused by accident or

illness. (With thanks to Ms Angela Eikhout, Eindhoven, Netherlands for her contribution.)

Some do’s and don’ts.

Indian

micro-finance banker Harishchandra Sukhdeve wrote the following contribution to the

Micro-Finance Gateway resources list on 26th September 2007. His words have

been edited with his permission for inclusion in this Model. [ The original

internet source for this article is no

longer available.]

“Group formation

and its nurturing in a right way is a key to not only poverty alleviation but

also conflict resolution and women’s empowerment.

Women’s groups are

found to be more efficient and professional.

However, while

forming groups certain Do's and Don'ts are must.

A list of do’s

01. Interact with

people through village level meetings.

02. Encourage

groups to hold regular meetings.

03. Educate them

about community living, public hygiene, education, nutrition, etc.

04. Proactively

pass on all legitimate benefits to farmers/villagers.

05. Ensure

trouble-free timely finance to farmers as well as other group members.

06. Promote

farmers groups for collective farming.

07. Promote

share-croppers' groups.

08.

Ensure/facilitate appropriate training for entrepreneurship development.

09. Encourage

innovation and self regulation by the groups.

10. Encourage

inclusiveness.

11. Encourage

young volunteers to promote the culture of

the groups.

A list of don'ts:

01. Do not allow

groups to be formed of the same family members except for farmer’s groups for

collective farming.

02. Do not allow

groups to finance to non-members.

03. Do not allow

one person to become member of more than one group.

04. Discourage

control of groups by any single person.

05. Do not try to

regulate the groups too much as this may hamper their ingenuity,

06. Do not stretch

hand-holding for too long a period. ”

THE MICRO-CREDIT FUND AND EMERGENCIES.

How would the

cooperative micro-credit fund work in conditions of extended drought or other

emergencies? The project creates social, financial, productive and

service structures. These structures are permanent. They are run by the management

cooperative set up for the purpose, and they remain in place as long as people

continue to live in the project area. This is so even where inhabitants return

to the project area after a temporary migration outside of the project area for

survival purposes.

The situation

with the Cooperative Local Development Fund at any given point of time depends

on the decisions taken by those chosen to manage it. It is reasonable to expect that in times of

extended drought and similar crisis conditions that families have difficulties

making their monthly contributions to the Fund and that beneficiaries (and

their guarantors) have problems repaying

the micro-credit loans they have received.

The

micro-credit fund is cooperative. Should a point be reached where as a result

of Act of God outside the control of the parties, families are unable to make

their monthly payments or beneficiaries are unable to repay their debts, the

managers of the Fund may decide to waive payments of contributions meantime or

to leave it up to the families whether to make their payments or not. In any

case the Fund would remain intact. It

would continue to be systematically recycled interest-free. But the total

amount in the Fund would not continue to increase as it would otherwise have

done. In case of projects financed by interest-free ten year credits, the

situation could arise that the monies collected in Fund turn out to be

insufficient to pay the whole of the original loan back at the close of the

first ten year period. On the other hand, where a productive period follows one

of extended drought or crisis, the Fund management could require an increase in

the monthly contribution of families to reinstate the Fund in time for

repayment at the end of the ten year period.

In times of

drought and scarcity, beneficiaries and those guaranteeing them may also face

great difficulty in making repayments of their micro-credits. What happens in

such a situation depends on the decision of the Fund management which is chosen

by the Central Committee of the Project. Logic would suggest in such situations

to grant more time to beneficiaries and those guaranteeing them to make their

payments. This would lead to a slowing down in the rate of recycling of the

monies in the funds, and therefore to a (temporary) slow-down in the rate of

development in the project area. However, the capital in the Fund would still

remain intact.

Yet another

situation which might arise is that the drought or other environmental

condition in the project area is so serious that the Fund management team

decide to gradually reimburse the monies in the Fund to the inhabitants to

supplement their extra costs for purchase of drinking water or food supplies

for survival purposes. In practice this means that as monies are (with great

difficulty) repaid by beneficiaries into the Fund, the repayments are for a

period of time re-distributed amongst all of the inhabitants, or amongst the

most needy. The cooperative local development fund would in this case operate

as an Emergency Fund. The consequences of this use would depend on the

reactions of donors and funding organisations and on the real and just

possibilities of subsequent recovery taking the cooperative nature of the Fund

into account. In the worst imaginable situation, the Fund might find itself

without any capital left. However, even in that case the structure of the Fund

would remain in place. Upon improvement in the climatic situation, families

would recommence making their monthly contributions to the Fund, which would

build up to full strength again after ten years.

Refer also to

section The effects of inflation on the Cooperative Local

Development Fund and gift content and to section Project insurance and forfeit in the form of gift in

case of loss of capital structures.

1. Research.

Give a detailed

two-page comparison between the micro-credit structures foreseen in the Model

for integrated development projects and those of micro-credit agencies such as

the Grameen Bank. First provide a short introduction.

Then discuss the reasons for high interest rates charged in traditional systems

and how they are eliminated in integrated development structure. Discuss the

contrast between micro-credit loans seen as “business” and the cooperative

system foreseen in integrated development projects. Discuss the nature and the difference between the target

beneficiaries and the aspects concerning their exclusion (traditional systems)

and non-exclusion (Model) from the system benefits. Discuss the indirect

financial leakage from project areas under traditional systems and the way this is blocked by integrated

development projects. Draw your conclusions.

2. Opinion.

On two pages

take the results of your research and use them to make a presentation of the

Model system to the representatives of Civil Society in your project area. Make a note of their reactions.

3. Opinion.

The previsions

in the Model for integrated development take an average two-year pay-back time

into account. After having spoken to the population in your chosen project

area, explain on one page the average payback time you would foresee in your

area and the consequences this would have on the on-going re-cycling of funds.

4. Research.

Provide a

one-page explanation to the women in your chosen area of a 20 year cycle of

management of the Cooperative Local Development Fund there What are their

reactions?

◄ ►

◄ Fourth block

: Section 3: Financial structures.

◄ Fourth

block : The structures to be created.

◄ Main index for the Diploma in Integrated Development

(Dip. Int. Dev.)

>◄ List of key words.

◄ List of references.

◄ Course chart.

◄ Technical aspects.

◄ Courses available.

◄ Homepage Bakens Verzet

"Money

is not the key that opens the gates of the market but the bolt that bars

them."

Gesell,

Silvio, The Natural Economic Order, revised English

edition, Peter Owen, London

1958, page 228./span>

“Poverty is created scarcity”

Wahu Kaara,

point 8 of the Global Call to Action Against Poverty, 58th annual

NGO Conference, United Nations, New

York 7th September 2005.

This work is licensed under a Creative Commons

Attribution-Non-commercial-Share Alike 3.0 Licence.

{kind=link}

{kind=link}

{kind=link}