NGO Another Way (Stichting Bakens

Verzet), 1018 AM

SELF-FINANCING,

ECOLOGICAL, SUSTAINABLE, LOCAL INTEGRATED DEVELOPMENT PROJECTS FOR THE WORLD’S

POOR.

|

FREE E-COURSE FOR DIPLOMA IN INTEGRATED DEVELOPMENT |

|||||

Edition 02 : 08 August, 2011.

Edition 03 : 09 February,

2013.

(VERSION EN FRANÇAIS PAS DISPONIBLE)

Summaries of monetary reform

papers by L.F. Manning published at http://www.integrateddevelopment.org

NEW Capital is debt.

NEW Comments on the IMF (Benes and Kumhof) paper “The

Chicago Plan Revisited”.

DNA of the debt-based economy.

General summary of all papers published.(Revised edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

The Manning plan for permanent debt reduction in the national economy.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

THE

DNA OF THE DEBT-BASED ECONOMY.

The following

three-dimensional diagram represents the DNA of the debt-based economy. It is

tilted forward from the top to make its features easily understandable.

Click here to view

a drawing showing

the DNA of the debt-based economy.

{kind=link}

Click

here to view a schematic drawing of a debt model of the debt-based economy.

{kind=link}

The diagram is made

up of two mirrored helical strands of financial DNA. The blue strand represents

the total accumulated GDP output for a given period while the red strand

represents the total outstanding productive investment principal. The vertical

axis of the helices represents time. The diagram shows a random period of four

years.

On the blue helix,

Vy bases of production output My are added over the time

span needed to make one full turn of the blue helix (usually a year). On the

red helix, Vy bases of national saving Sy (net new

productive investment) are added over the time span needed to make one full

turn of the red helix (usually a year). For ease of consultation, the bases are

shown only for year three. The drawing shows nineteen of them, as this is the

approximate speed of circulation Vy of productive deposits My in

The helices

replicate by extension. The blue helix showing GDP “dies off” at the end of

each period. The helices grow exponentially by the transfer of National Saving

Sy from the blue helix to the red one over each notional production

cycle.

For each of the

bases the national saving Sy is returned to the next production

cycle on the blue helix in the form of net new capital investment Sy

(Saving = Investment) as shown. Individual bases can vary in size (up or down)

reflecting the state of the economy.

The annual length

or growth ring Lz of the blue helix shows the GDP as it

accumulates during that year. The

nominal, usually annual, GDP growth in the blue DNA is the change in length Lz

of the DNA spiral over the period z compared with the corresponding length L z-1

over the previous period. In the diagram, the length (and therefore the

diameter) of the GDP spiral is shown to be increasing exponentially from year

to year.

The annual increase

in the length of the growth ring Lz of the red helix shows the

annual increase in outstanding

investment principal S which also equals the nominal GDP growth for that year.

The total length of the red helix at any time is the sum of all outstanding

investment principal. It equals the

current (annual) GDP at any time.

At the end of each (annual)

period z (and only then) the value of output represented by length Lz

of the blue helix (the GDP for that year) equals the value represented by the

whole of the red helix (its total length representing the sum of all

outstanding investment principal).

The plan diameter

of the helices typically expands exponentially. The helices vary together with

the state of the economy. In the case of recessions they show up as changes in

the annual rate of increase of the

helix diameters, and therefore the length of the spiral loops. In the case of

depressions they would show up as an actual

annual decrease in the helix diameters.

Click here to view

a drawing showing

the DNA of the debt-based economy.

Click

here to view a schematic drawing of a debt model of the debt-based economy.

"Money is not the key that opens the gates of the market but the

bolt that bars them."

Gesell, Silvio, The Natural Economic Order, revised English edition,

Peter Owen,

“Poverty is created scarcity.”

Wahu Kaara, point 8 of the Global Call to Action Against Poverty, 58th

annual NGO Conference, United Nations,

“You shall not crucify mankind upon a cross of gold.”

William Jennings Bryan, Official Proceedings of the Democratic National

Convention Held in Chicago, Illinois, July 7, 8, 9, 10, and 11, 1896, (Logansport,

Indiana, 1896), pp.226–234.

“Where is the thicket?

Gone. Where is the eagle? Gone. The end of living and the beginning of

survival.”

Speech (as later reported) by Si’ahl,

‘Chief Seattle’, Seattle, 1854.

![]()

This work is

licensed under a Creative Commons Attribution-Non-commercial

Share-Alike 3.0 Licence.

THE DNA OF THE DEBT-BASED ECONOMY

BY

EMAIL: manning@kapiti.co.nz

VERSION

3 31/7/2011

CONTENTS PAGE

01. THE REVISED FISHER

EQUATION.

02. DEBT AS MONEY.

03. INTEREST AND BANK

SERVICES.

04. DEPOSIT INTEREST AND

SYSTEMIC INFLATION.

05. THE CURRENT ACCOUNT.

06. SAVING AND INVESTMENT.

07. CREATION OF AND PAYMENT

FOR CAPITAL GOODS.

08. THE DEBT MODEL.

09. DIFFERENTIAL ANALYSIS

DEPRESSIONS AND RECESSIONS.

10. EQUITY IN SOCIETY.

11. THE RELATIONSHIP BETWEEN

SAVING, INVESTMENT AND GROSS DOMESTIC PRODUCT.

12. SUMMARY.

01.

THE FISHER EQUATION.

The basic mechanisms at the heart of the “modern” financial system have never

successfully been put into a logical framework enabling the underlying

relationships of its mechanical components to be quantified.

One effort to do so was provided by Irving Fisher in 1912

MV = PQ (1)

Where:

M = the amount of money in

circulation.

V = the speed of circulation of that money; the

number of times M is used over a given period T.

P = the

price level of goods and services an economy produces during time T,

Q= the

quantity of monetised goods and services an economy produces during time T.

The product PQ is

what is known today as Gross Domestic Product or GDP.

1. Irving Fisher “Elementary

Principles of Economics” 1912. The

Fisher equation has been very widely discussed in relation to the economic

difficulties arising from the sub-prime mortgage defaults in the

At first sight, the

Fisher equation seems to be self-evident. People have to be able to produce and

exchange goods and services. To the

extent money is used to do this, the total produced must bear a relationship to

the amount of money and the frequency with which it is used.

In practice, very little money

is needed if the speed of circulation V is high. In a very simple market

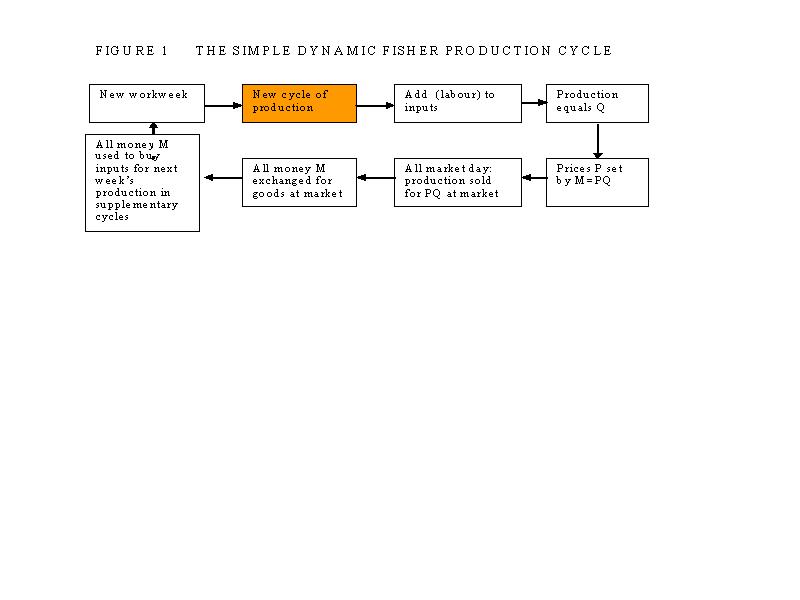

economy all the money could be exchanged every weekly market day. This is shown

in Figure 1.

Click here to view FIGURE 1 : THE SIMPLE DYNAMIC FISHER

PRODUCTION CYCLE.

{kind=link}

Figure 1 is cash-based. In it, factors M, P and Q have been assumed

to be constant. The available money supply remains in circulation.

If, in Figure 1, PQ were greater

than M, not all of the goods for sale could be sold. Either M would have to be higher or P lower.

Over a year, the money M in

Figure 1 is circulated 52 times because there are 52 weekly markets, so V in

the Fisher Equation would be 52.

The V in the Fisher

equation refers to the speed of circulation of 100% of the money supply.

Humans are, by

nature, hoarders. Ever since money was first used, and especially after durable

metals like gold and silver were used for the money supply, people have “saved

for a rainy day.” The money physically

circulating at the market in Figure 1 was just a part of the total money

supply, not all of it. The rest was

“stored” 2. Instead of V in

the Fisher equation being 52 as shown in the simple example in Figure 1, it was

in fact much less because most of the money supply was hoarded. Despite that,

the value of V seems to have been more or less stable over long historical time

periods 3, suggesting the human tendency to hoard is psychological

as much as functional.4

3. Studies by the author

suggest that the speed of circulation V in

4. When the

amount hoarded is “enough” people will spend more.

Where the speed of

circulation V is constant it becomes more a structural than a dynamic component in the Fisher relationship. The immediate

response to a change in the money supply M will therefore tend to be a change

on the production side of the equation PQ.

If the change in M is rapid, the response will be a change in prices P

until production and demand adjust to compensate for the change in the money

supply. That’s different from what happens with fresh produce in the

supermarket after bad weather. In that case the money side of the equation

remains unchanged and prices rise because production falls. That happens in the

shops regularly and from season to season. Changing the speed of circulation V

would reflect either a change in people’s behaviour toward money, or changes in

the way the financial system works.

2.

DEBT AS MONEY.

Structural changes

in the money supply M began with the creation of new debt as money. When the Bank

of England was established in 1694, the money supply, for the first time,

became relatively independent of the supply of gold and silver.

When a bank issues

a new loan the loan becomes an asset in the accounts of the bank. The new loan

asset is offset by an equal bank liability in the form of a money deposit in

favour of the borrower. Money has been created “out of nothing” by way of a

bookkeeping entry. In the debt-based

financial system, for every dollar of money M there is a dollar of debt. Every loan must be repaid over time. As it is repaid, the outstanding loan is

reduced and the corresponding outstanding money deposit is also reduced by the

same amount. When the loan has been repaid both the loan and the debt have been cancelled out of existence.

Unlike gold and

silver coins, debt cannot be hoarded. The debtor must repay the loan from

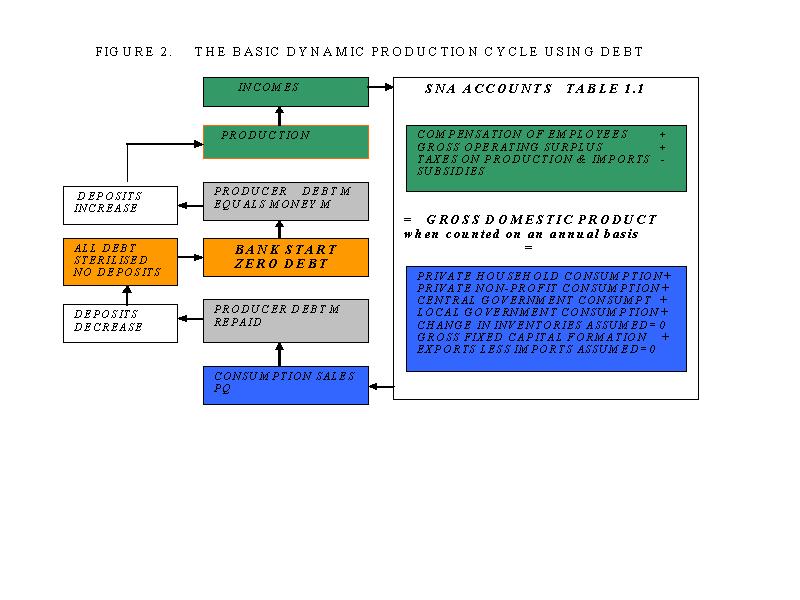

whatever deposits he or she can earn. That creates the production cycle shown

in Figure 2. For simplicity, the debt M

in Figure 2 is interest-free. Production and consumption are shown on the right

hand side of Figure

A fundamental

structural change has taken place. Whereas in Figure 1, the money M remains in

circulation, in the simple debt system shown in Figure 2 there is no money and

no debt left at the end of each cycle because each cycle is self-cancelling.

Click here to view FIGURE 2 :THE BASIC DYNAMIC

PRODUCTION CYCLE USING DEBT.

{kind=link}

In aggregate, it is impossible

to save debt. It is, therefore, impossible to hoard or “save” money issued in

the form of debt in the debt system shown in Figure 2 without also increasing

debt. The cash component of a given money supply can, however, be hoarded. 5

In the real world,

production and consumption are going on all the time. There is always an amount

of debt M and its corresponding “money” deposits in use in the

dynamic economic

system. In this paper, the dynamic production

debt will be called My and its speed of circulation Vy.

Vy has

not been constant in the debt-based system because there have been structural

changes to the financial system itself. In industrialised societies, the role

of debt in the productive economy has increased over time. Cash transactions

now contribute very little to the measured GDP.

The proportion of employees paid weekly and the distribution of income

among employees, businesses and taxation shown in the upper right hand side of

Figure 2 have also changed 6.

There are also shorter-term variations. During recessions, business bill

payment time increases compared with the average while, during economic

expansions, it tends to decrease 7.

6. Indicatively

for

3.

INTEREST AND BANK SERVICES.

Interest has been

paid on loans ever since the use of money became widespread thousands of years

ago. People would loan their hoarded cash savings to someone else and expect

their savings to increase by the amount of interest they received. The borrowers would usually borrow in the

expectation that doing so would increase their productivity or their fortune in

some other way. For example, buying an ox or workhorse might dramatically

increase production from a farmer’s land.

The increased production created by using the ox or

the workhorse would more than offset the interest on the loan. Both parties

were better off as a result of the investment made by using the borrowed money.

The operative word

is “investment”. Investment is the use of money (originally cash, now mostly

debt) to increase production. The problem with the formation of the Bank of

England in 1694 was twofold. First, the

loans it made to the government of the day were not to increase production but

to help pay the war debts of the crown. Secondly the Ways and Means Act 8

that authorised the Bank of England provided for a perpetual fund of interest

charged on ships’ “tunnage” and liquor duties. Not only was the loan for

current spending instead of investment, it would never be repaid because the

Bank of England directors were happy to receive risk-free interest payments

forever. Since then, governments have found it very easy to borrow perpetual

debt in this way and its use has increased steadily over time.

The major change to the financial system brought by

the formation of the Bank of

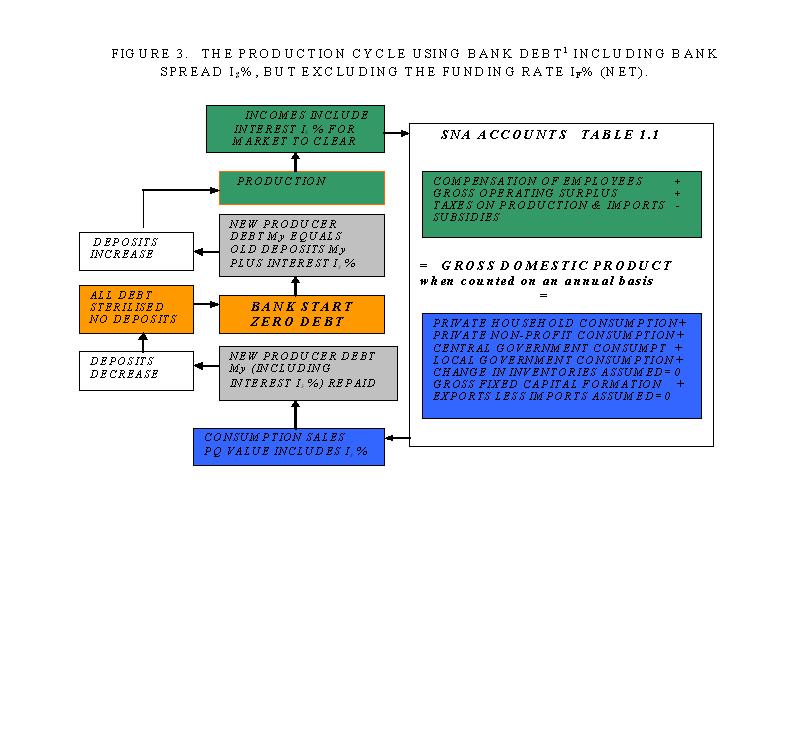

In the basic

dynamic cycle using interest-free production debt as shown in Figure 2, there

is no residual debt after any individual production cycle, and no residual

deposits.

The basic debt

system incorporating bank interest as part of the productive economy is shown

in Figure 3. There, the bank interest Is % is the bank spread 9. It does not include the funding interest If

% banks pay on deposits. Bank interest Is % is part of the

productive economy. Funding interest If % paid by banks on deposits

(net after tax) held by their clients is not productive.

8. 5 & 6

William and Mary C.20

9. The bank spread is the difference between the total loan interest (called the claims rate) and the interest the banks pay on deposits (called the funding rate). In this paper, bank spread is denoted by Is%, the bank funding rate by If % and the claims rate by Ic %, where Is%, = Ic - Ic .

Banks provide goods

and services just like any other business. Those goods and services are part of

the gross domestic product (GDP). The bank spread is a large part of the

“price” of banking. The only difference between Figure 2 and Figure 3 is that

in figure 3 bank services become part of Q in the Fisher equation output PQ and

the interest Is becomes part of the production debt My

already referred to on page 8. The production cycle is therefore still

self-cancelling as in Figure 2.

Click here to view FIGURE 3. THE PRODUCTION CYCLE USING BANK DEBT 10

INCLUDING BANK SPREAD IS%, BUT EXCLUDING THE FUNDING RATE IF%

(NET).

{kind=link}

10. Figure 3 does not take

into account the effects of the current account.

The interest Is

banks charge to provide goods and services and the tax paid on funding interest

If is part of productive economic activity and does not cause

inflation.

4.

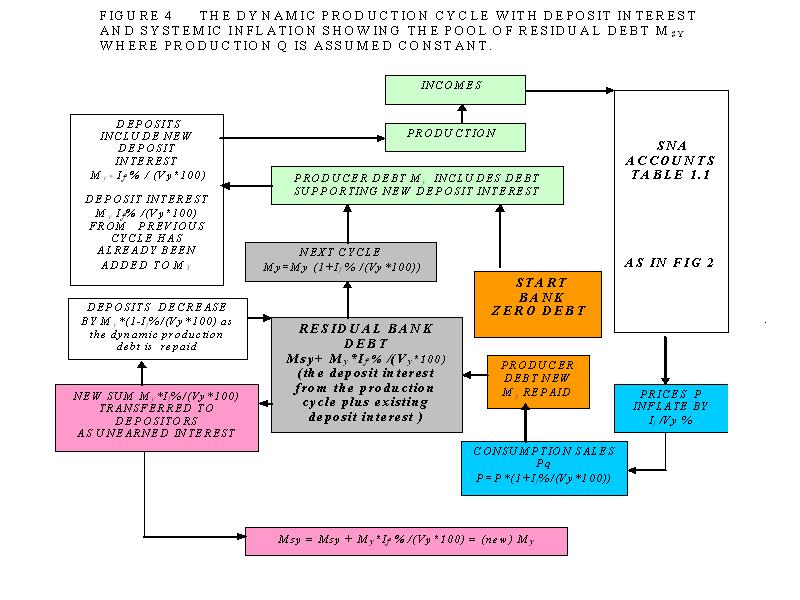

DEPOSIT INTEREST AND SYSTEMIC INFLATION.

Click here to view FIGURE 4 : THE DYNAMIC PRODUCTION CYCLE WITH DEPOSIT

INTEREST AND SYSTEMIC INFLATION SHOWING THE POOL OF RESIDUAL DEBT MSY WHERE

PRODUCTION Q IS ASSUMED CONSTANT.

{kind=link}

Figure 4 shows what

happens when funding interest If % is paid on bank deposits. The

dynamic production debt My is all repaid in full to the bank at the

end of each cycle. The funding interest If % paid by a bank is a

bank liability, not an asset. The deposits belong to deposit holders. The bank

must transfer to them the deposit interest it receives when the production debt

My is repaid. At first sight the bank would be losing money because

it would be left in debt by the same amount as the deposit interest.

In practice, the

production system does not “pulse” as shown for simplicity in Figure 4. Instead, there is an ongoing dynamic flow of

production and consumption funded by the dynamic production debt My.

The pool of residual debt (My in this paper) shown at the lower

centre of Figure 4 is the accumulated interest component My*If % /(Vy*100)

created through each nominal business cycle. 11 Since the

price P itself is the sum of the price increases shown at the bottom right of

Figure 4, price P must represent the total price inflation.

Assuming production

Q is constant, the deposit interest If

% (less tax) can be paid to depositors only if prices P increase as

shown. Otherwise the production debt My

cannot be cleared when the

economic production Pq 12 is sold. In this paper, the inflation

caused by the deposit interest on the dynamic production debt My is

called systemic inflation.

In an economy based on

interest bearing debt, almost all price is inflation.

11. My is a dynamic variable similar to those used in almost every iterative

computer program. The new total becomes the

old total for that variable plus the increment added to it each cycle.

12. The quantity

of production q is what is produced in the single nominal production cycle

shown in Figure 4. The amount q must be multiplied by the speed of circulation

Vy to get total output Q.

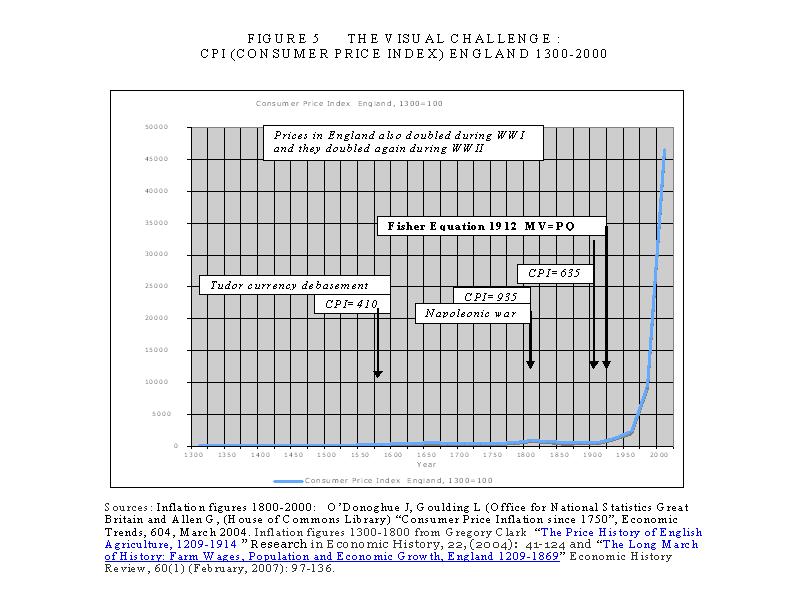

Click here to view FIGURE 5 : THE VISUAL CHALLENGE. CPI (CONSUMER PRICE

INDEX) ENGLAND 1300-2000.

{kind=link}

Figure 5 gives a historical

overview of inflation in

By the beginning of

the 20th century prices had increased by just 6 times in 600 years,

with nearly all the increases due to the “great debasement” of the mid-Tudor

period and the Napoleonic wars around the turn of the 19th century.

Prices fell by about one third between 1800 and 1900 during the industrial

revolution due to vast improvements in productivity. Higher productivity means more goods and

services are produced for the same input costs leading to lower prices P if

money M and speed of circulation V remain constant.

![]()

![]() The price change

formula P=P*(1+ If % /(Vy *100)) shown at the bottom

right of Figure 4 refers to a single production cycle producing the (constant)

economic output q. Figure 6 shows that, assuming the deposit interest rate If

and output Q are more or less constant, physical inflation is half of If

%. The figure P* If % /(Vy *100) is the rate of change of

P. It must be mathematically integrated to give the total change in P. This

increase in price in called systemic inflation.

The price change

formula P=P*(1+ If % /(Vy *100)) shown at the bottom

right of Figure 4 refers to a single production cycle producing the (constant)

economic output q. Figure 6 shows that, assuming the deposit interest rate If

and output Q are more or less constant, physical inflation is half of If

%. The figure P* If % /(Vy *100) is the rate of change of

P. It must be mathematically integrated to give the total change in P. This

increase in price in called systemic inflation.

Click here to view FIGURE 6 : SYSTEMIC INFLATION.

{kind=link}

Systemic inflation

is a structural part of the debt-based financial system whenever interest is

paid on deposits.

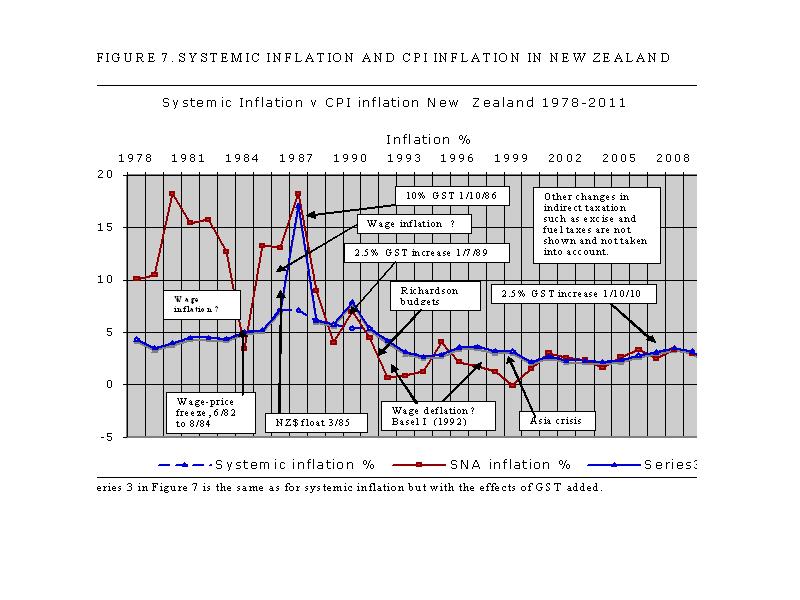

Figure 7 compares

systemic inflation with consumer price inflation (CPI) in

Click here to view FIGURE 7. SYSTEMIC INFLATION

AND CPI INFLATION IN NEW ZEALAND..

{kind=link}

Rapid wage

increases increase the debt for production My faster than would

normally be the case. From the original Fisher Equation (1) MV=PQ, if M rises

while V and Q stay the same, P must rise in proportion to the rise in M. This is what happened before the debt-based financial

system became dominant after WWII as shown in Figure 5. It also seems to have

happened in

13. This raises

an interesting debate about comparing averages with indices and the

relationship between price indices and measured economic growth. The saw-tooth

form of the official SNA data in Figure 7 suggests serious issues with economic

management from 1978-1999.

14. The 1983 and

1985 years will still have been affected by wage factors even though they fell

partly within the period of the wage-price freeze.

When economic productivity

increases, more goods and services are produced using the same productive debt

My because, in aggregate, the unit cost of each item produced is a

little less than it was previously. In

the original Fisher equation

(MV=PQ), if M and V remain constant and Q increases then

P must decrease.

The price of many

items has fallen dramatically over the years as shown, for example, in Figure 5

during the industrial revolution in

Productivity growth

is inherently deflationary.

Labour productivity

is often measured by dividing the value of total production, the gross domestic

product (PQ), by the total number of paid hours worked. Capital productivity is often measured by

dividing PQ by the total current productive investment.. Education and skill

levels play a major in both measures because they allow new ideas and new

technologies to be introduced. Caution

needs to be used when applying productivity figures because the methods used to

measure them can be inaccurate. Typically, employees with higher education and

skill levels are paid more. That tends

to increase some incomes at the expense of others, distorting the income

distribution in most western economies.

The most extreme form of this is the very high compensation packages now

being paid to the executives of large corporations.

This paper assumes

that, in aggregate, wages inflate at systemic inflation plus the rate of productivity

growth to maintain overall price levels.

One key reason why so many employees in modern industrial economies feel

and are in fact worse off is because the benefits of productivity increases are

skewed as discussed above 15.

The increasing skew can be corrected only by income redistribution

within the economy.

15. Discussion of

the income skew is outside the scope of this paper, but one common way to

measure it is by using GINI coefficients.

The higher the coefficient the more skewed he income structure is. Over

the past 30 years

In a debt-based

economy where interest is paid on deposits, systemic inflation is half the

interest rate If paid on deposits provided adjusted incomes rise in

line with inflation and productivity growth and there are no changes to

indirect taxes.

Distributing the

benefits of productivity increases throughout the economy by improving real

wage levels and purchasing power requires socially mandated income redistribution.

Many developed

countries have failed to redistribute the benefits of increased productivity,

with consequent loss of consumption capacity in the wider economy. The classic

case of this in recent years is the tax cuts made by recent republican

presidents in the

Deposit interest

rates declined in

16.

17. Other possible

explanations are the backward “smoothing” of official data after the

introduction of the revised System of National Accounts (SNA93) in 1996 and the

implementation of the

5.

THE CURRENT ACCOUNT.

The current account

process is shown in Figure 8. The purple

box at the lower left shows how payments made on the current account in debtor

countries like

Click here to view FIGURE 8 : THE CURRENT ACCOUNT PROCESS.

{kind=link}

18. The

Foreign ownership

of a debtor nation’s economy drains its domestic economic growth through

outgoing current account payments of interest on commercial paper and dividends

and profits arising from the physical foreign ownership of its assets.

Foreign ownership

of a debtor nation’s economy exposes it to high interest rates and the

permanent risk of capital flight.

In a debt-based

economy, it is not possible to both consume domestic production and pay for the

remittances to foreign countries covering interest and profit because that

would mean spending the same deposit twice. The cost of remittances for

interest and profit payable abroad must therefore be borrowed within the

domestic economy of the debtor country to enable the value of goods and services

produced there to be consumed.

The surplus goods

and services produced in a creditor country are part of its gross domestic

product and are counted towards its economic growth. When they are exported, so is the

growth.

A positive balance

on external trade exports domestic growth in exchange for foreign assets.

The deposits from

the sale of capital goods by a debtor country do not return to those who

borrowed the debt to pay for the surplus goods and services and remittances

sent offshore. They finish up, instead,

in the hands of those in the debtor country that have sold assets (or an

indirect claim on those assets) to settle the current account deficit. This means the debtor country’s capital

account must be reduced accordingly.

Contrary to popular

opinion, the direct borrowing of foreign currency by debtor country banks does

not increase asset inflation in the debtor country. This is because the

creation of the additional domestic debt used to fund the current account

deficit precedes the banks’ offshore borrowing. The bank “borrowing”

the foreign exchange simply “avoids” creating some of the deposits that would

otherwise result in the direct sale of assets in the debtor country to settle

its current account imbalance. If the creditor country banks chose not to lend

their foreign currency to the debtor country, the additional domestic deposits

that would necessarily arise from the sale of an equal amount of assets to

foreigners would further inflate domestic asset values in the debtor country.

Many, if not most,

of the debtor country deposits arising from the foreign “investment” as shown

at the upper left of Figure 8 fail to qualify as productive investment as

defined under the international System of National Account (SNA). They cause,

however, additional structural inflation through the payment of deposit

interest on the extra deposits. In that indirect sense, current account

deficits are always inflationary in the debtor country. The amount of inflation

depends on the interest rate paid on deposits in the debtor country and the tax

rate on interest income there.

The main

determinant of the exchange rate is the opportunity cost of capital in the

debtor country. It has to be “worthwhile for the creditor to “invest” in the

debtor country. When there is a free capital market the debtor must “match”

other investment options around the world. Otherwise the debtor country’s

exchange rate would need to fall until the investment prospect becomes “good”

enough for the creditor to “invest”. The base-line opportunity cost of capital

is the long-term bond rate in the debtor country. because bonds can be freely

traded. Almost the only determinant of the bond rate is the deposit interest rate

that must take foreign assessments of lending risk into account.

The main component

of the current account deficit in debtor countries is by interest paid on the existing accumulated current account

deficit.

At any point of

time, the current account deficit in heavily indebted debtor countries is

approximately the sum of the accumulated current account deficit x the average

bond rate - the trade balance for the preceding period + the net profits of

foreign-owned banks for the preceding period.

6.

SAVING AND INVESTMENT.

The use of the term

“saving” to describe a current account surplus is misleading. A creditor

country uses the surplus deposits on its current account to buy foreign assets

not because it has saved but because it has sold surplus production offshore

and received remittances from offshore. It is a trading dynamic, not a

conscious decision to forgo or defer consumption. It can be more a function of

overproduction than under-consumption.

The assets the creditor country buys mostly represent existing wealth

like equities, businesses, property, and related loans, rather than new

investment in bonds and business expansion in the debtor country that would be

defined as productive investment in the SNA. They are not “saving” as defined

in orthodox economic theory because most purchased foreign assets do not relate

to new domestic production in the creditor country and do not alter its gross

domestic product.

The purchase of

offshore assets and the provision of loans to offshore banks is, from the point

of view of the creditor country, income earning and “productive” at the price

paid for them, otherwise the exchange would not take place. That “income” is

not national income for the creditor

country because it cannot be remitted there. It forms part of the creditor

country’s current account surplus that is, in turn, swapped for more foreign

assets, and so on as long as the current account surplus continues.

From the debtor

country’s point of view, deposits arising from foreign capital inflows on the current

account qualify as “saving” in the debtor country national accounts only when they

are committed to new productive capacity. In reality, most capital inflows that

appear as domestic deposits in the debtor country represent “investment” in the

unproductive investment sector that serves to inflate the value of existing

assets or “wealth” there. That

“investment” neither adds to nor reduces production capacity in the

debtor country. It does not qualify as

investment under the System of National Accounts (SNA) and is therefore not

“saving” as defined in orthodox economic theory. Any deposits from the capital

inflows used to retire existing debt in the debtor country reduce debt and

deposits by the same amount. They do not affect the domestic economy of the

debtor country other than to reduce the systemic inflation caused by interest

payments on the domestic deposits a little.

Taking the current

account balance (CA) in creditor countries and debtor countries in turn the

sequence of the exchange that takes place is:

Any gross fixed

capital formation from return capital flows invested by a creditor country as

foreign direct investment in new capital goods in the debtor country is

automatically included in the GDP of the debtor country 19. The increase in the total

capital value in the creditor country contributed by the capital goods it

receives in payment of the debtor country’s CA deficit should be recorded in

its capital account. If it is to be treated as income, it must also be shown in

the creditor country’s income and outlay account.

In a debtor

country, gross fixed capital formation arising from any return capital flows

invested by the creditor country in new capital goods in the debtor country is

automatically included in the GDP of the debtor country 20. The decrease in the total capital value of

capital goods in the debtor country resulting from its sale of capital goods to

the creditor country in payment of the debtor country’s CA deficit should be

recorded in its capital account. If it is to be treated as negative income, it

must also be shown in the debtor country’s National income and outlay account.

19. It is assumed

that, since the debt that gives rise to the sale of capital goods in the debtor

country already exists, the deposits created from that debt also exist at any

point in time. Any productive investment arising from those deposits returned

to the debtor country in payment for its capital assets is therefore automatically

included in the debtor country’s domestic gross fixed capital formation.

20. It is assumed

that, since the debt that gives rise to the sale of capital goods in the debtor

country already exists, the deposits created from that debt also exist at any

point in time. Any productive investment arising from those deposits returned

to the debtor country in payment for its capital assets is therefore

automatically included in the debtor country’s domestic gross fixed capital

formation.

When the current

account balance is included as income in the national income and outlay account

of the SNA an entry of equal value entitled “purchase of capital assets on the

current account” should be included on the “use of income” side of the national

income and outlay account.

The National income

and outlay account of the SNA needs to be restructured to reflect orthodox

economic theory as follows:

Use of income side:

= Final

consumption C

+ Purchase

abroad of non-productive capital investment goods (=CA)

+ Saving for productive investment S. (2)

Income side:

= GDP

+ Current account balance (CA)

less the balance on external

goods and services

less repayments of principal

on outstanding productive investment. (3)

The National capital account

of the SNA needs to be restructured.

There is no “saving” residual on the “use of

income” side of the National income and outlay account because the items

“Purchase abroad of non-productive capital investment goods (=CA)” and the Current Account

Balance (CA) in equations (2) and (3) cancel each other out.

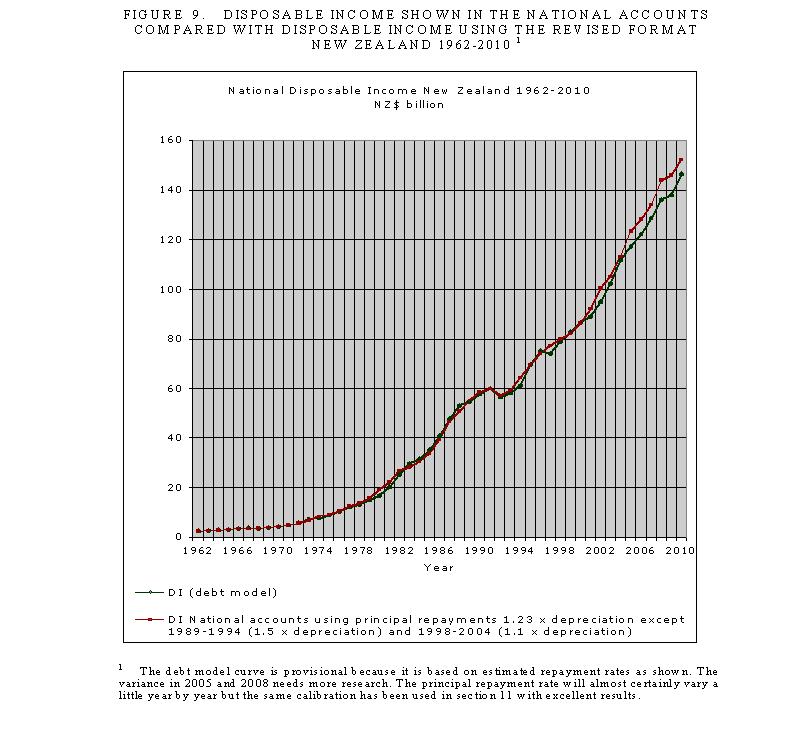

When Saving is

calculated as gross capital formation less principal repayments as shown in

equations (2) and (3) and used in Figure

Click

here to view FIGURE 9 : DISPOSABLE INCOME SHOWN IN THE NATIONAL

ACCOUNTS COMPARED WITH DISPOSABLE INCOME USING THE REVISED FORMAT NEW ZEALAND

1962-2010 21.

{kind=link}

Click here to view FIGURE 10. NATIONAL SAVING S, AND NATIONAL SAVING S AS A PERCENTAGE OF

GDP* NEW ZEALAND 1962-1010. The GDP used in Figure 10 is

GDP as presented in the national accounts. Saving is gross capital formation

less the principal repayments calibrated as in Figure 9.

{kind=link}

Saving in developed

countries, particularly debtor countries like

While higher

depreciation may in part reflect technological innovation and “planned

obsolescence”, its main effect has been to increase the ratio of principal

repayments to productive investment.

Higher repayment rates lead to a lower net operating surplus after debt

servicing and therefore a lower saving rate 23.

21. For example,

if the depreciation rate on a purchase of $10000 is increased from 20% to 25%

(therefore repaid in about 3 years) the extra depreciation is $500/year,

whereas the interest saved (at 10%) is just 10% of, say, a $650 extra annual

repayment, or $65 per year for 3 years; about $200 altogether. The firm’s

profit increases by roughly $300/year.

22.

United Nations, 2008 par. A.3.88 p.589 states: “The 2008 SNA

recommends that the consumption of fixed

capital should be measured at the average prices of the period with respect to a constant-quality

price index of the asset concerned”.

This appears to exaggerate the “depreciation “ effect on saving.

23. The debt

model curve is provisional because it is based on estimated repayment rates as

shown. The variance in 2005 and 2008 needs more research. The principal

repayment rate will almost certainly vary a little year by year but the same

calibration has been used in section 11 with excellent results.

Until now, there has been

little or no mention in economics literature of this structural impact on

saving.

National saving has been swapped for

short-term business profit, typically boosting stock and existing property

prices instead of longer-term investment.

Increased depreciation

allowances speed up principal repayments and reduce Saving S and Investment I.

7.

CREATION OF AND PAYMENT FOR CAPITAL GOODS.

Click here to view FIGURE 11 : INVESTMENT AND CAPITAL FORMATION.

{kind=link}

Figure 11 shows how

capital goods are created and funded.

The basic economy without capital goods is shown in blue. The funding of

capital goods and subsequent repayments are shown in orange. The fundamental

orthodox investment equation (Savings= Investment) is shown in red.

The production of

goods and services giving rise to new capital goods is included in the

productive debt shown as My in Figure 11 24. Those new capital goods must be sold to clear

the market. Since the income earners in the productive sector who want to buy

the capital goods are not usually the same as those who produce the capital

goods, they are exchanged through bank intermediation.

24. See The interest-bearing debt system and its economic impacts for details of the debt model. The model is in

the process of being modified to separate the dynamic production debt My

physically needed to produce the GDP from the productive debt Mcd as defined in

the referenced paper.

The buyers of the

capital goods borrow part of the production incomes of employees (employee

incomes) and businesses (gross operating surplus) Sy=S/Vy where Vy is the speed of

circulation of Mv, as shown in the upper part of Figure 11. That

enables the original producer loans My to be retired, thereby

clearing the market.

In aggregate, some

employees and businesses have notionally swapped their share of the sale price

of the capital goods that they do not want to consume with others in the

productive sector (the investors shown

at the lower left of Figure 11) that do want to consume them. This creates

lending within the productive sector. There is a debt created in favour

of the “savers” in return for their deposit. After using the “savers’” deposits

to repay the production debt the investor has a debt as a liability and a

capital good as an asset, while the “savers” have an interest-bearing loan to

the investor as an asset to replace the deposit they had in the bank.

Whatever bank

intermediation takes place, in aggregate, the process shown in Figure 11 must always be true if the goods and services

Q produced by the productive sector are all to be sold to clear the market.

Where that does not happen, there will be consequential changes in

inventory.

The main feature of

the exchange discussed above is that the investor debt is interest-bearing and

accumulates with each production cycle.

The investment and

capital formation shown in Figure 11 is dynamic. The faster the rate at which

investors repay their debt, the less Saving there will be, because Saving = New

investment less repayment of outstanding capital.

Increased repayment

of debt, including household debt, reduces Saving and reduces net new

productive Investment.

Any attempt to withdraw

any part of deposits S/Vy for

non-productive investment purposes (“savings”) reduces purchasing power in the

productive economy or leaves capital goods unsold, leading to increases in inventory, and

subsequent unemployment and recession.

In

“Savings” schemes

such as Kiwisaver in

It is impossible to

increase GDP or Saving without increasing production loans My and

new productive investment.

Increases in

inventory, other than what is needed to allow for inflation and population

growth, have very little, if any, value despite their being entered in the

National Accounts as “investment” at cost.

Added inventory and subsequent production must later be discounted to

clear the build-up, otherwise inventory would continue to grow.

There is always an outstanding production debt My

that is continually being recycled through the production system and there is

always a corresponding flow of Saving Sy = S/Vy and

investment Iy = I/Vy for the production of capital goods.

Economic policy planning and implementation must

be based on a progressive dynamic supply of new productive debt My

to make use of spare labour and resources in the economy or to increase the

skills of, and re-employ existing resources.

Capital formation takes place by new debt

formation within the productive sector itself and domestic productive

investment in terms of the SNA can be viewed as the redistribution of

production incomes to clear the capital goods market in the productive sector.

Capital formation as it is shown in Figure 11 of this

paper follows the basic tenet of orthodox economics that Savings=Productive

Investment.

Investment in new residential housing consumes

part of the Savings Sy=S/Vy

in Figure 11. As noted at the lower right of Figure 11, most housing investment

is, however, economically unproductive once it has been built. Furthermore,

the more new housing investment there is, the less is available from Sy

for other productive investment. Assume, for example, that in

Not only does housing construction slow the

growth of economic consumption, it is very difficult for the buyers of new

homes to repay their mortgage debt without decreasing their own existing

consumption. As shown in Figure 4, incomes nominally increase at only the rate

of systemic inflation. As discussed in section 4, systemic inflation is half

the deposit interest rate. The increased income of homeowners is therefore not

enough to repay the interest on their mortgages, let alone repay any principal. It follows that to own their new homes

homeowners must consume less by an amount equal to their principal repayments

plus their mortgage interest.

In the absence of productivity gains, new

homeowners must reduce their domestic consumption by an amount equal to

principal repayments plus their interest cost.

In the distant past, the income deficit could

have been met by large labour productivity gains. Increasing labour

productivity is deflationary because, unless extra incomes are injected into

the economy to cover the purchase of the extra production, it makes available

more goods and services for the same production cost.

Consumption could be maintained as long as the

productivity increase was enough to offset, in aggregate, the additional

interest and principal payments being made by households

25. Suppose for example,

outstanding home mortgage debt is $100b and GDP is $200b and that interest

rates are 7%, bank spread 2% and principle repayments 3%. The total productivity increase would need to

be 7% + 3% or 10% x S100 b = S10 b. $10b/200b = 5% of GDP. Productivity increases like that do not occur

in developed economies because developed economies are largely service-based.

Allowing 1% for productivity increases means a deficit of 4% of GDP before

taking into account population changes and changes in the balance of trade.

More recently, indebted homeowners have instead been

working longer hours, often by switching from single-income households to

two-income households. While indebted households may manage to keep up their

mortgage payments by working longer and/or with two members working instead of

one, there is a corresponding structural decrease in consumer demand that

cannot be satisfied within the productive economy. That structural decrease in

consumer demand is the result of interest and capital payments homeowners must

make to repay their household debt. Either consumers in aggregate must be

induced to borrow outside of the productive economy to maintain demand (for

example, by re-mortgaging their homes) or there will be growing structural

unemployment as production is reduced because of the oversupply of consumption

goods and services. The only other option is to export the surplus consumption

goods and services.

In practice there is a combination of outcomes

with some productivity increase, perhaps 1% annually in New Zealand, developing

structural unemployment and some (extra) consumer debt to temporarily maintain

demand. There should also be an improvement in the balance of trade. Additional

debt can be generated using house price inflation as the security for new

loans. However, the additional consumer

debt cannot be repaid out of existing incomes any more than the indebted

homeowners can repay their loans from their incomes. In both cases the extra

debt makes the productive economy worse and not better off in the longer term

due to falling consumption capacity. The classic result of this was the

sub-prime crisis in the

In the long run, homeowners cannot repay their

mortgage debt without causing increasing structural unemployment in the

productive economy. They can export the surplus consumption goods and services

they cannot themselves consume This will alter the balance of foreign ownership

of the domestic economy but not the wellbeing of its people.

Residential housing

investment that does not generate income is fundamentally incompatible with a

financial system based on interest-bearing debt.

SECTION

8. THE DEBT MODEL.

The first version

of the debt model was published in the paper:

Manning, L “The Ripple Starts Here: 1694-2009 : Finishing the

Past”, presented at the 50th

Conference of the New Zealand Association of Economists (NZAE),

While the debt

model is based on the volume of debt, it is unrelated to earlier volume-based

reform proposals like those of Social Credit that failed to offer a viable

theoretical basis to support them.

The premise in both

the debt model and Figure 4 is that the circulating deposits and cash My

= Prices P x output q where q is the quantum of domestic output produced by My

over a single cycle. Taken over a whole

year, the SNA definition of Gross Domestic Product GDP is given in the debt

model by mathematically integrating the expression Pq* Vy, where Vy

is the number of times the circulating deposits and cash My are used

during the year 27.

The SNA should

reflect an expression of the original Fisher Equation of Exchange as shown in

Figure 2 28. The only

difference is that the money supply M in the Fisher equation of exchange included

hoarded cash, whereas in the debt system shown in Figure 2 for practical

purposes there is now very little cash contributing to measured GDP.

In Figure 4 My

cannot include hoarding of debt beyond the term of the production cycle because

all the productive bank debt giving rise to My is conceptually

repaid at the end of the cycle 29.

26. http://www.nzae.org.nz/conferences/2009/pdfs/The_Ripple_starts_here_1694-2009__Finishing_the_Past.pdf

. Non-members can access the paper by Google search: NZAE The Ripple Starts

Here (use “quick view”).

27. The

contribution of cash transactions in industrialised countries is now (very) small.

28. The Fisher

equation has been very widely discussed in relation to the economic

difficulties arising from the sub-prime mortgage defaults in the

29. As previously

noted, in practice there is a continuous flow of production and consumption so

the deposits and cash My are always

present, but they are being used in the production cycle, not hoarded.

At any point in

time there are five broad blocks of deposits in the domestic financial system.

They are:

Mt The transaction deposits representing the

productive debt My - M0y so:

My

= Mt + M0y (4)

Mca The

accumulated domestic deposits representing the sale of assets to pay for the

accumulated current account deficit (see section 5 of this paper for

details).

M0y The cash in

circulation included in Mv and used to contribute to productive

output.

Ms The net after

tax accumulated deposits arising from unearned deposit income on the total

domestic banking system deposits M3 (excluding repos) 30.

(M0-M0y) Cash hoarded by the public and not used

to generate measured GDP.

In this paper the

total of these deposits, that is, Mt + Mca + M0y

+ Ms , is provisionally assumed to be the M3 (excluding repos)

monetary aggregate published by most central banks monthly less the amount of

cash in circulation M0 except for the part M0v that is included in My. In this paper M0y is assumed to

have the same speed of circulation as My. In industrialised countries, the contribution

of cash transactions to the measured output of goods and services (GDP) has

been declining in recent decades and their contribution to the GDP has been

provisionally calibrated for the purposes of this paper 31.

In this paper, the

total debt in the domestic financial system is assumed to be the Domestic

Credit, DC debt aggregate published by most central banks monthly.

At any point in

time there are four broad blocks of domestic debt in the domestic financial

system. Three of them together add up to DC such that:

DC = Dt + Dca 32 + Ds

(5)

Where

Dt The

productive debt supporting the transaction deposits Mt.

Dca The whole of the debt created in the

domestic banking system to satisfy the accumulated current account deficit 33.

Ds The residual debt to balance equation (5)

30. Repos refer

to inter-institutional lending

31. More accurate

assessment of the cash contribution to GDP over time requires further detailed

study.

32. Arguably the

accumulated sum of capital transfers could be included here, in which case the

net international investment position (NIIP) would be used instead of the

accumulated current account. The decision affects the size of the “residual” Db.

33. This is

greater than the monetary deposits Mca because the

banking system may have sold commercial paper to borrow foreign currency to

satisfy the foreign exchange settlement as shown in Figure 8.

The fourth block of debt is :

Db, the virtual “bubble” debt, the excess

credit expansion or contraction in the banking system such that Ds - Db = the debt supporting the accumulated deposit interest Ms defined

above. Db can be positive or

negative as discussed further below in relation to Figure 5.

There is also a

fifth block of debt Is that is, conceptually, not bank debt .

Is, the

total debt accumulated by investors arising from Saving Sy = S/Vy.

In Figure 11, the

investor pays the investment Iy =I/Vy = Sy =

S/Vy to the producer and the

money is used to retire the outstanding part of My relating to the

investment in question. Conceptually the investor borrows the purchase price

from employee incomes and the business operating surplus as discussed in

section 7. Except for households buying new homes discussed separately on pages

27-28, the investor then becomes a producer, and the interest on investment Iy

is included as a production cost in the subsequent production cycle loans My.

The predicament of

new homeowners is quite different. They cannot service their debt because they

cannot, conceptually earn more than they were before they bought their new

home, because the home itself is nearly always unproductive. There is no new

income stream from their housing investment. If economic demand is to be

maintained, homeowners must, in aggregate, rely upon increasing house prices

and refinancing of their properties, creating an aggregate “pass the baton”

systemic increase in debt.

When non-productive investment assets are

traded there is typically a capital gain because of asset inflation on

investment (Dca + Ms + the property component of Is). The new purchaser pays more for the asset

because of asset inflation, allowing the seller to retire the outstanding

mortgage debt on the property.

By definition in this paper :

My x Vy

= GDP

Ms = Ds

The cash contribution to GDP =

M0y * Vy. Therefore :

DC = (GDP)/Vy - M0y + Ms + Dca

+ Db (6)

Ms =Ds =

(DC – Dca ) – GDP/Vy + M0y - Db (7)

GDP = Vy *(DC - (Ms +Dca

+Db ) + M0y ) (8)

My = GDP/Vy

= DC - (Ms +Dca + Db) + M0y (9)

Where the terms are as defined

on pages 28-29.

Equations (6 ) to

(9) are all forms of the debt model developed in previous papers 34.

34. Links

are provided in the conclusion to this paper.

Ms is

the same format as Ms in the earlier forms of the model. It has been freshly

calibrated. Unlike the previous forms of the model equations (6) to (9) are

general and include the contribution made to the economy by cash transactions.

In equation (7),

all the terms except GDP/Vy = My and Db are

known or can be estimated with reasonable accuracy. For the purposes of

equations (8) and (9) My can

be approximated using trend-lines because it is small compared with Ms.

Db is unknown but can be approximated through the calibration as in

Figure 5. The calculations in equations (8) and (9) involve the subtraction of

large numbers to get relatively small numbers, which leaves them sensitive to

modelling and data error.

If Ms,

calculated as “the accumulated deposits arising from unearned deposit income on

the total domestic banking system deposits M3(excluding repos) ” as

defined on page 30, agrees more or less with that calculated in equation (7),

bearing in mind the value of Mb, the proposition that debt growth is

determined by deposit interest will be proven.

The model will require further calibration as further data becomes

available. Despite that, it is

self-evident Db will be positive during periods of rapid expansion,

particularly as bubbles form, and will become negative during periods of rapid

contraction, particularly as bubbles collapse. The classic case of this in

The dependence of

the gross domestic product (GDP) on the Domestic Credit DC and the interest

rate on bank deposits in the modern cash-free economy from which Ms

is calculated has profound implications for economics.

In the light of the

worldwide financial chaos of 2007-2009 the indicative debt model shown in

Figure 12 provides a powerful argument in support of public control of a

nation’s financial system.

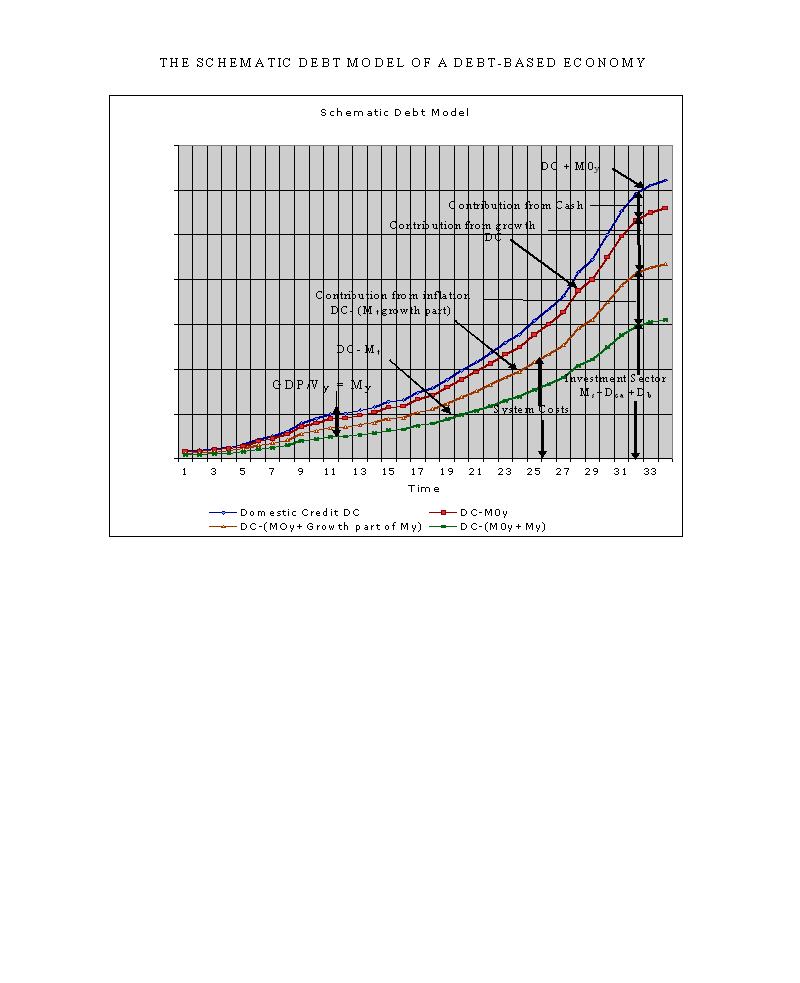

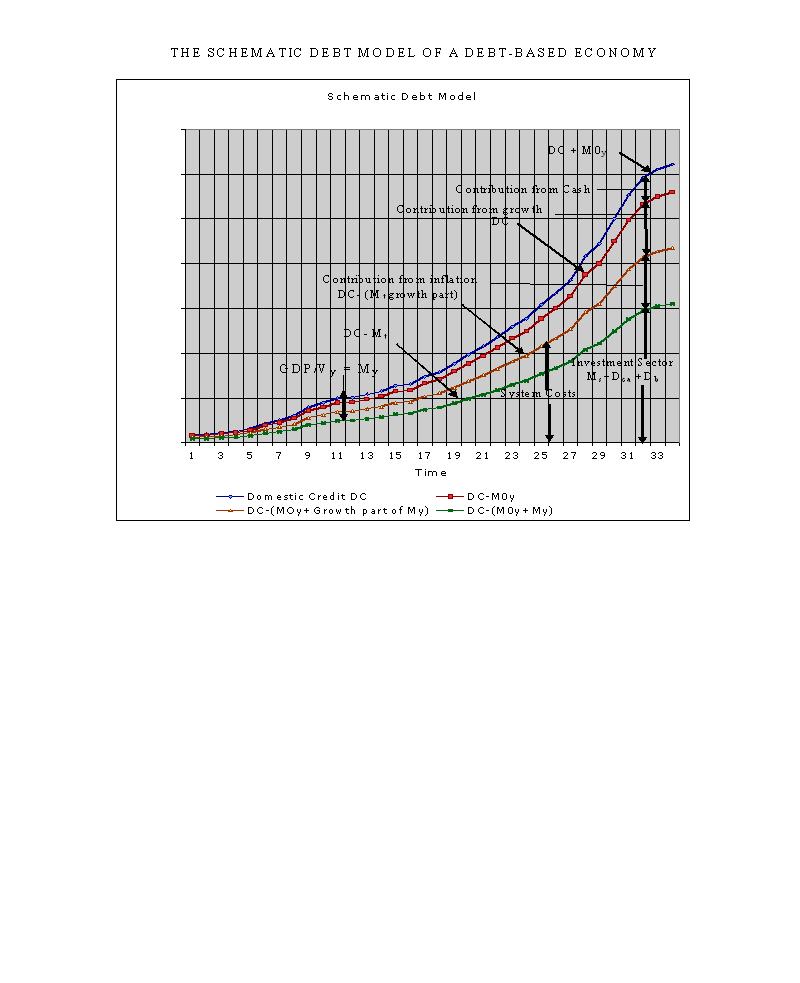

Click here to view FIGURE 12 : THE SCHEMATIC DEBT MODEL OF A DEBT-BASED ECONOMY.

{kind=link}

The vertical axis

in Figure 12 applies to the Domestic Credit for

It isn’t possible

to have a simpler model of the economy than equation (8):

My

=Nominal GDP/Vy equals domestic credit DC less (unearned net deposit

income Ms + the accumulated current account Dca + the

cash contribution to GDP M0y plus a correction for bubble activity Db

(+/-))

Domestic

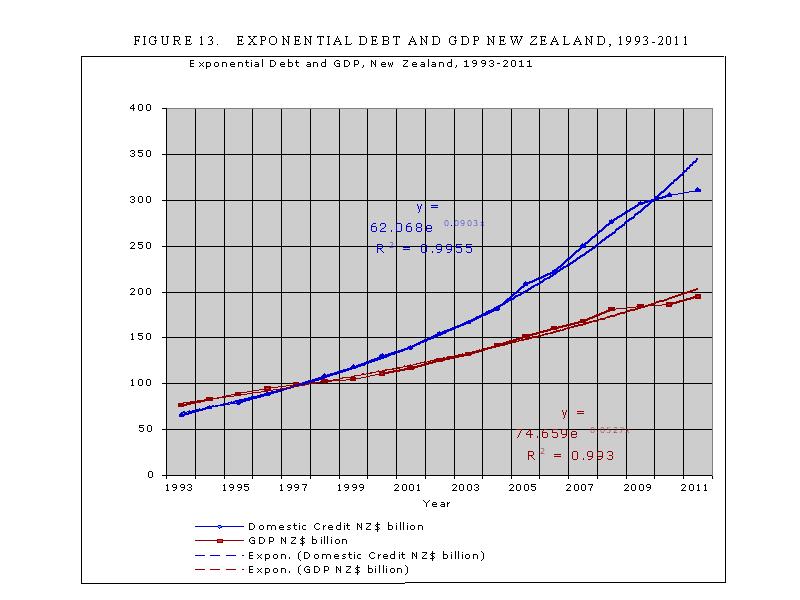

Click here to view FIGURE 13 : EXPONENTIAL DEBT AND

GDP NEW ZEALAND, 1993-2011.

{kind=link}

It is theoretically impossible

to maintain exponential debt expansion faster than GDP expansion over an

extended period because the added debt servicing costs will always leave the

productive sector insolvent.

To avoid national

bankruptcy, each nation must maintain, in aggregate, a zero accumulated current

account deficit.

A first

approximation for the speed of circulation Vy of productive debt

plus cash transactions My is given in Figure 14. Vy varies with the change in the

payments systems. Minor secondary shorter-term cyclical variability also occurs

through changes in the average time taken to pay bills. When times are tough people take longer to

pay their bills, and each change of a day in the time taken to pay them can

alter Vy by perhaps 0.25%. The process is usually reversed in better

times. Otherwise Vy reached a constant value of about

35. Vy is estimated at the moment so the present figures are indicative. Once

further research accurately refines the present estimates, Vy will be sufficiently accurate for predictive purposes.

Click here to view FIGURE 14 : SPEED OF CIRCULATION Vy NEW ZEALAND 1978-2011.

{kind=link}

Note that in Figure

14, no correction has been applied to Vy for secondary increases in

payment time during recessions or decreases in payment time during economic

boom periods. The maximum correction in Vy appears to be in the

order of +/- 0.3 or up to 1.5%. The series shown is less stable from 1978 to

1989. This is possibly due to distinctly different growth exponentials

1978-1989 arising from the very high interest rates that were typical during

those years.

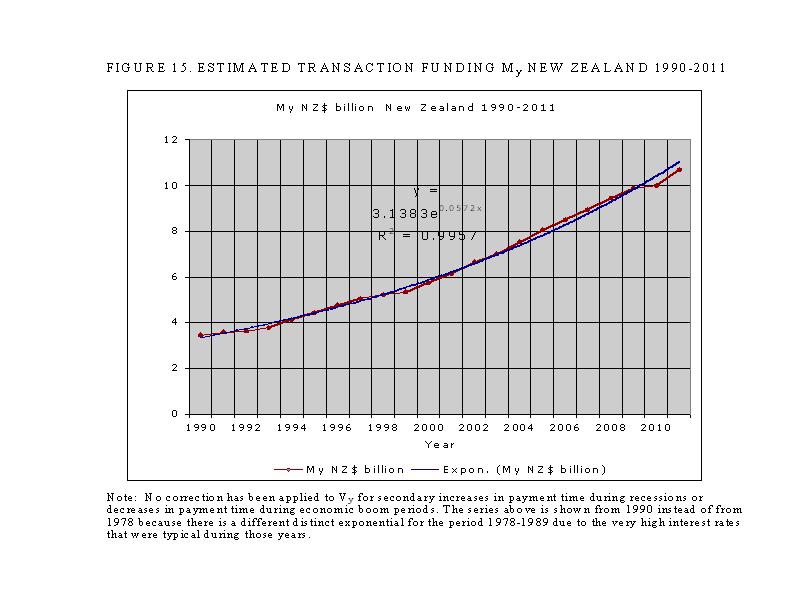

As shown in Figure 15, My in

Click here to view FIGURE 15 : ESTIMATED TRANSACTION FUNDING My NEW ZEALAND 1990-2011.

{kind=link}

The methodology

used to calculate Vy in Figure 15 is as follows. The GDP in

Businesses pay

suppliers monthly, and indirect payments are usually made on a monthly basis

too, so their speed of circulation is about 12 on average. Most workers get

paid fortnightly (though some get paid weekly and some monthly) so an average

speed of circulation of 26 has been assumed for that.

When the above figures are

weighted the weighted average speed of circulation is (12x(42.7+12.3)+45 x

26)/100 = 18.3.

A similar estimate

of payment trends and a separate Vy calculation was made for each of

the other years, and a polynomial best fit curve was drawn as in Figure

15.

My was

then obtained by dividing the official GDP figure by the speed of circulation

taken off the best fit trend curve. This

gives the data series shown in Figure 16 and used when applying the debt model discussed in

section 8.

The methodology is

easily replicable using better information about payment trends and is

applicable to any country.

Figure 15 shows the

preliminary estimate for estimated production debt and cash My in

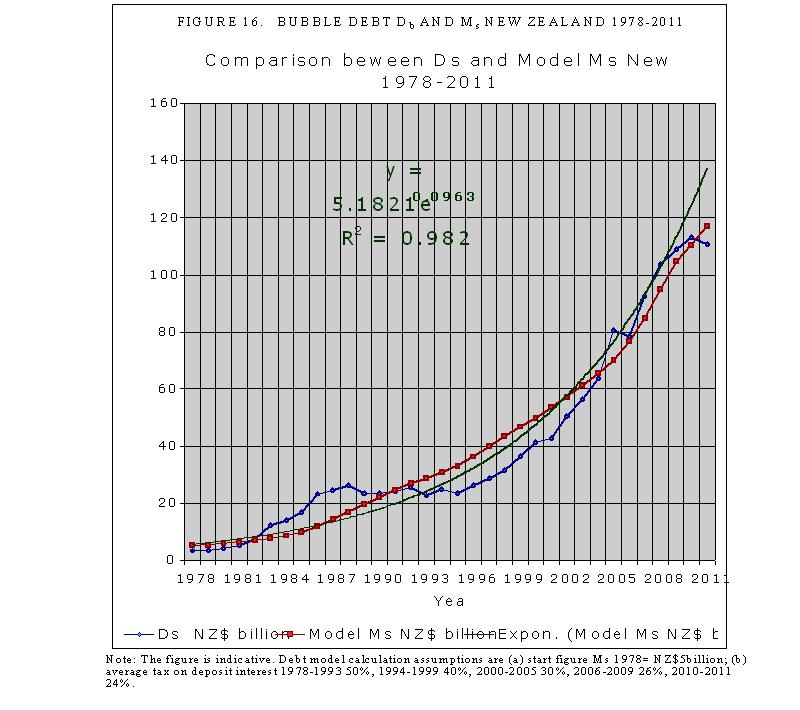

Figure 16 shows an

indicative comparison between the residual debt Ds for New Zealand

calculated from equation (5) and plotted against the model Ms

calculated as the accumulated after tax deposit interest on M3 (excluding

repos). The curve for Ms is a first approximation because

assumptions have been made on the average tax deducted from the gross payments

of unearned income (M3 (excluding repos x the average interest paid on

deposits). The tax is the average tax

paid by each income-earner on his or her total income. It is not the marginal

tax rate 36. The losses from

the 1987 share market crash in

Once the tax rates

on Ms have been accurately calibrated, the size of any debt bubble Db

can be immediately calculated.

Measures can then be taken to eliminate the bubble without risking any economic

downturn.

Click here to view FIGURE 16 : BUBBLE DEBT Db AND Ms NEW ZEALAND

1978-2011.

{kind=link}

9. DIFFERENTIAL ANALYSIS DEPRESSIONS AND

RECESSIONS.

Equations (6) to

(9) can equally be applied in their differential form by calculating

differences from one period to the next.

For example, over

any small period of time dt, the change in the total debt DC = the change over

the same time dt of ( GDP/Vy - M0y + Ms + Dca + Db ).

There is quite a

lot more variability in the figures calculated this way compared with equations

(6) to (9) because

additional error is introduced by multiple subtractions of large numbers.

Using the

differential approach (and Newtonian notation) allows the new debt model to

show how the economy is performing in practice. With better data economic performance

could be assessed monthly, or even, theoretically, in real time. The

differential equations are:

d/dt DC = d/dt ( GDP/Vy - M0y

+ Ms + Dca +

Db )

(10)

d/dt Ms =d/dt Ds

= d/dt ((DC – Dca ) – GDP/Vy + M0y - Db ) (11)

d/dt GDP = d/dt (Vy *(DC

- (Ms +Dca + Db ) + M0y

)) (12)

d/dt My = d/dt GDP/Vy = d/dt (DC - (Ms +Dca + Db) + M0y (13)

where:

DC = Domestic Credit debt aggregate published monthly by central

banks.

GDP = Gross Domestic Product

(the same as economic output PQ in the original Fisher Equation

Vy = The speed of circulation of the

productive debt My

My = The dynamic productive debt used to

generate output (see Figure s 3 and 4)

My is interchangeable

with GDP/Vy in equations (10) to (13).

M0y = The cash in circulation included in Mv

and used to contribute to productive output.

Mt =

The transaction deposits representing the productive debt My - M0y

so:

Ms = The

net after tax accumulated deposits arising from unearned deposit income on the total domestic banking system

deposits M3 (excluding repos) 37.

Dca = The whole of the debt created in the

domestic banking system to satisfy the accumulated current account deficit 38.

Ds = The

residual debt to balance equation (5)

Db =The virtual “bubble” debt, the excess credit

expansion or contraction in the banking system such that Ds - Db = the debt supporting the accumulated deposit

interest Ms.

37.

Repos refer to inter-institutional lending

38. This is

greater than the monetary deposits Mca because the

banking system may have sold commercial paper to borrow foreign currency to

satisfy the foreign exchange settlement as shown in Figure 8.

For example, in

d/dt DC =

d/dt (GDP/Vy - M0y

+ Ms + Dca + Db) (10)

NZ$ 26.4b

= 0.73 + 0.02 + 10.01 + 13.34 +

d/dtDb

=

NZ$24.1b + d/dtDb .

This shows the credit bubble

grew by about NZ$ 2.3b in the March 2008 year.

Figure 16 shows the

bubble surplus Db growing in the March 2008 year (upward slope of Ds

relative to Ms), accounting for the difference between the official

figure and the derived one. The example above is within the statistical error

of the official data even before taking Db into account. More

calibration work is needed before using the differential method for predictive

purposes, particularly in equation (12) that requires a small number to be

multiplied by Vy to get the change in GDP 39.

39. There are

periodically quite large revisions in the official statistical data, too, that

make all the national account data estimates rather than facts.

An approximate

check of the calibration is readily available because in Figure 16, Db

should be zero where the model Ms curve intersects the Ds

curve. Some obvious years to check are 1982, 1992, 2004 and 2009 though the two

curves do not cross exactly at the data points.

In Figure 16 using

the nearby data points the “error” between Ds and Ms in

1982 is -1.0% of GDP (Ds slightly larger than Ms). In

1992 the error is + 1.7%, in 2004 +1.4%, and in 2009 -1.8%. The error between

the Ds curve and the Ms curve is within acceptable limits

given the preliminary nature of the model calibration and the accuracy of the

official data series.

A non-zero figure

for Db in the debt model represents an imbalance between existing

debt and economic performance, and it indicates unsatisfactory financial

management.

When Db

in the debt model is negative a credit bubble exists and when Db is

positive an economic contraction is taking place. When the slope of the bubble

is rising (upwards over time) the bubble is intensifying and when it is falling

(downward over time) it is dissipating. The bubble is not fully dissipated

until the Ds curve meets the Ms trendline and Db

has returned to zero. When the slope of the recession is falling (downwards

over time) the recession is intensifying and when it is rising (upward over

time) the economy is in recovery. The recovery is not complete until the Ds

curve meets the Ms trendline and Db has returned to zero.

Figure 16 shows

that in

From equation (12), when d/dt

GDP = 0

d/dt GDP = d/dt (Vy *(DC

- (Ms +Dca + Db ) + M0y)) (13)

Since in a fully debt based

financial system M0y is zero and d/dt Db is usually small,

d/dt DC =

d/dt (Ms+Dca

) approximately (14)

In a debt-based

financial system, if there is no increase in the total economic output,

domestic credit must still increase by the amount of unearned income that has

to be transferred to the investment sector Ms plus any current

account deficit that has to added to Dca. Unless there is residual

bubble debt Db in the financial system, failure to maintain

sufficient domestic credit as in equation (14) would be accompanied by economic

collapse because GDP would necessarily fall by any shortfall in domestic credit

x Vy.

The provision of

new debt for inflation in the debt model together with unearned income and the

current account deficit can together be considered financial system costs.

Economic growth occurs only when and to the extent that d/dt DC exceeds the

financial system costs as shown in Figure 12.

A recession

provides for inflation but not economic growth, while a depression provides for

neither economic growth nor inflation.

A recession occurs

when the change in the total debt over time is less than what is needed to

service the financial system costs made up of the net unearned interest that

has to be paid on all bank deposits plus any new current account deficit plus

any increase in the productive debt used to generate new economic output. In

that case, d/dt DC is less than d/dt

(Ms+Dca ) plus provision for inflation.

A depression is a

deep recession. It occurs when the change in the total debt over time is less

than what is needed to service the unearned interest that has to be paid to the

accumulated net deposit interest Ms plus any current account deficit

that has to be added to the accumulated current account deficit Dca,

that is, when there is no provision for either inflation or growth.

The model can be

used to provide specific measurable monetary targets to avoid recessions and

depressions. The targets can easily be identified in advance and new debt

injected into the system to maintain growth limited only by the resources

available and the productive capacity, education and knowledge of employees and

businesses.

The amount of new

productive debt d/dt My needed to fully utilise the available

resources and the productive capacity, education and knowledge of employees and

businesses is very small. In

40. It may even be that all is needed is a public guarantee that any excess production during the recovery period will be purchased, in other words a state guarantee to give businesses the confidence to produce.

The collapse in the

capitalist system is caused, in part, by its failure to recognise that

production must, just by a little bit, lead consumption to provide the incomes

that enable consumption to take place.

In recent decades

it has been assumed that lower interest rates would be enough to restart a

stalled economy. That is no longer true. The exponential growth of debt required

by the debt-based system itself means that the increase in consumption

capacity generated by an interest rate cut is no longer sufficient to allow an

economy to recover.

For example, in

March 2011, domestic credit in

Interest rate

reductions only work to stimulate an economic recovery when asset inflation

remains high enough for the debt generated by refinancing and trading of

existing assets to offset the systemic debt requirements of the financial

system.

The logical outcome

of the existing debt system in creditor countries is zero deposit interest and

stable or falling asset prices (as in

In the absence of

strong capital controls, the logical outcome of the existing debt system in

debtor countries is bankruptcy because debtor countries must maintain high

rates of interest to avoid capital flight. The debtor status of debtor countries

can only be reduced if their exchange rates are reduced so their current

accounts become positive enough to reverse the foreign ownership of their

assets.

There is a powerful

theoretical incentive for public investment in new production to assist a

market economy out of recession or depression. That investment in the first

instance needs to be in new means of production to provide incomes and

employment to relieve the fiscal pressure on public social welfare expenditure.

Once the market economy fails, as it does in recession, it cannot recover

without a stimulus sufficient to encourage the private sector to invest and

produce. Until the private sector does so, the production cycle is effectively

broken.

Government has a

fundamental role to stimulate an economy when it enters a recession by directly

investing in new production.

Infrastructure investment is too slow to be useful because there is a

long lead-time before increased productivity exceeds the infrastructure costs.

10. EQUITY IN SOCIETY.

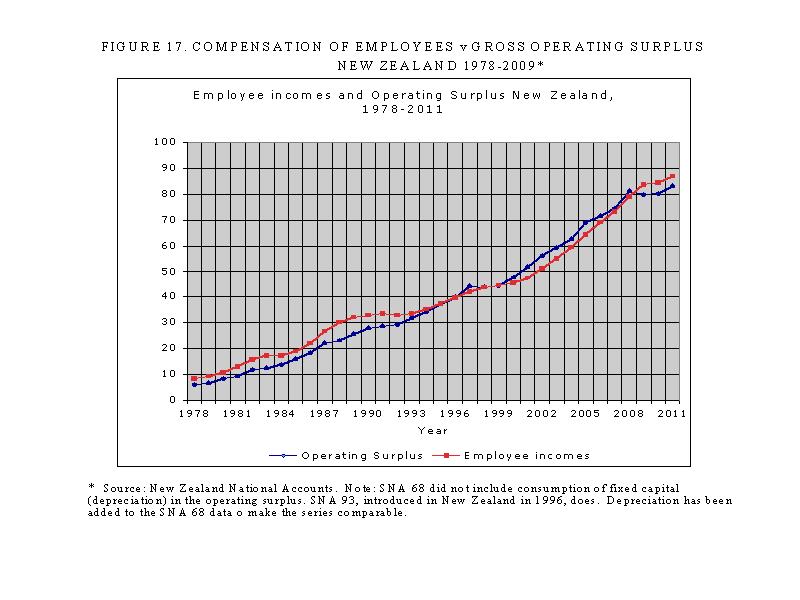

Figure 17 shows

compensation of employees plotted against the operating surplus for

Click here to view FIGURE 17 : COMPENSATION OF EMPLOYEES v GROSS OPERATING SURPLUS NEW

ZEALAND 1978-2009.

{kind=link}

The System of

National Accounts (SNA) version 68 (1968) did not include consumption of fixed

capital (depreciation) in the operating surplus. Version SNA 93, introduced in

One common way of

measuring income equality is by using the Gini coefficient

Over recent decades,

Since 2007, the

Gini coefficient for

Poor income

distribution suppresses demand for domestically produced goods and services.

People with low incomes have relatively little to spend on domestic

consumption, especially on services, which make up the bulk of monetised

economic activity. Income concentration encourages relatively high demand for

imported “luxury” products adding to

41. It remains

possible the relationship between the numbers of entrepreneurs and the numbers

of wage and salary earners has altered, for example if firms became bigger on

average. Such changes would not be disclosed in Figure 17.

42. The Gini coefficient

is developed from the Lorenz curve, which is a plot of incomes against

population starting from the poorest groups in the population, There is a good

introduction at http://en.wikipedia.org/wiki/Gini_coefficient. The coefficient usually excludes investment

income.

43. The Gini

curve used for these figures was taken from the NZ Green Party website 19/6/10

because it is reasonably current. http://blog-greens.org.nz/2010/04/06/inequality-in-aotearoa-a-brief-history-of-inequality/ Various organizations like the UN and the CIA

calculate Gini coefficients which can vary depending on the way the basic data

is compiled.

44. This does not

suggest

There are just two

ways to avoid large earned income imbalances. The first way is to increase

lower end wages and salaries, especially minimum incomes. The second way is to

reconsider taxation policy, not for political reasons but because the existing

income distribution structure has not been working well. Both the debt model

referred to Section 8 of this paper and the analysis in Section 4 show that

inflation and growth must be reflected in incomes for the production cycle to

clear. Heavily skewed income distributions make the process of clearing the

market from each production cycle more difficult. Some people have “too much”

(and growing) income in relation to domestic consumption and many others “too

little” (and falling) income. “Ordinary” employment gets squeezed. That’s why

the economies of social democracies have tended to perform better than the more

capitalistic ones in recent times.

Every economy can

be thought of as having its own physical shape. That shape reflects the degree

of “reasonable self-sufficiency” the economy possesses. Reasonable

self-sufficiency describes how well domestic production matches the consumption

patterns of the population as a whole taking into account its income structure.

The less of its own domestic product an economy can afford to consume and the

more reliant that economy becomes on importing what it needs but does not

produce, the more skewed the economy becomes. The more skewed the economy the

more dependent it is likely to be on foreign trade, globalisation, and in some

cases, on the foreign ownership that arises from large accumulated current

account deficits.

Income distortions

have become structural, especially in industrialised capitalist economies.

According to the debt model, increased incomes are inflationary unless they are

accompanied by corresponding increases in productive output. Since the employed

workforce is already producing goods and services, the SHAPE of the economy,

the basket of goods and services produced in relation to incomes and

consumption patterns, will have to change if it is to improve the lot of the

people as a whole so that everyone gets a “fair” share 45. Increasing incomes without increasing

production would just increase prices.

Changing the shape

of the economy means eliminating excessive debt, especially the domestic

debt arising from current account deficits. It also suggests changing the tax

structure.

Tax structures in