NGO Another Way

(Stichting Bakens Verzet), 1018 AM

SELF-FINANCING,

ECOLOGICAL, SUSTAINABLE, LOCAL INTEGRATED DEVELOPMENT PROJECTS FOR THE WORLD’S

POOR

|

FREE

E-COURSE FOR DIPLOMA IN INTEGRATED DEVELOPMENT |

|||||

Edition 02: 18 November, 2010.

Edition 04 : 08 August, 2011.

Revised edition 05 : 22 August, 2011.

Edition 08 : 09 February, 2013.

(VERSION EN FRANÇAIS PAS DISPONIBLE)

Information on

monetary reform :

Summaries of monetary reform

papers by L.F. Manning published at http://www.integrateddevelopment.org

NEW Capital is debt.

NEW Comments on the IMF (Benes and Kumhof) paper “The

Chicago Plan Revisited”.

DNA of the debt-based economy.

General summary of all papers published.(Revised edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

The Manning plan for permanent debt reduction in the national economy.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

THE

INTEREST-BEARING DEBT SYSTEM AND ITS ECONOMIC IMPACTS.

By

Sustento

Institute

We are

almost blind when the metrics on which action is based are ill-designed or when

they are not well understood 01 .

01 Stiglitz et al 2009 p9.

Key Words: accumulated current account deficit, CPI,

current account deficit, debt, debt model, debt growth, deposit interest,

domestic credit, exponential debt growth, Fisher equation, inflation, national

accounts, revised Fisher Equation, structural debt growth, systemic debt

growth, systemic inflation, unearned income.

CONTENTS:

EXECUTIVE

SUMMARY.

01. INTRODUCTION.

02. The

DEBT PROBLEM.

03. The

simple economy.

04. The unsustainable

economy.

05. The

unsustainable economy with foreign debt.

06. The

debt model.

07. Systemic

Inflation AND INFLATION POLICY.

08. THE

DEBT EXPLOSION AND FINANCIAL STABILITY.

09. CULTURE

AND INSTITUTIONS.

10. CONCLUSIONS.

11. BIBLIOGRAPHY.

12. ACKNOWLEDGEMENTS.

EXECUTIVE SUMMARY.

This paper shows how debt evolves in the

interest-bearing debt-based financial system and why debt growth is

exponential. It analyses the fundamental

mechanisms of debt growth and provides a sound theoretical base to support the

analysis. The theoretical foundation is a revised form of the Fisher Equation

of Exchange that, for the first time, takes the structural effects of interest

bearing debt on the financial system into account.

Some earlier work [such as Snyder, (1940);

Danks/Social Credit (1955); Friedman, (1962)]

may at a superficial first glance appear to have some common grounds

with the analyses set out in this paper. This is not so. The only common ground

of this paper with the cited works is that it supports a quantitative approach

to the supply of money and credit in the economy. With some exceptions, mostly relating to war

and economic crises, the world’s money supply has always been based on the quantity

of money rather than the price of money.

The change to a price-based monetary system

accelerated after US President Nixon abandoned the

This paper shows how the price of money paid as

interest on deposits in the banking system produces a pool of unearned income that

causes self-reinforcing exponential debt growth.

The price-based financial system has not

prevented economic growth around the world, but that growth has come at

incalculable human and environmental cost. It has led to economic, political

and environmental instability and a widening gap between rich countries and

poor countries as well as between rich and poor within countries.

The figures given in the paper are preliminary.

They suggest that price-based debt expansion in developed economies is gradually

becoming unstable. The gross cost of

paying interest on the pool of unearned income Ms is about twice the systemic inflation in the

economy. Were it not for taxation on interest,

The immediate effects of crises like the current

one in New Zealand are large-scale loss of “savings “ (S in the debt

model) and equity, reduced incomes and

purchasing power in the productive economy

with associated job losses, growing income inequality and a declining

quality of life.

The paper shows that the current price-based

financial system based on interest bearing debt is self-destructive. It will

destroy the global economy unless it is changed. The world must return to a

financial system based on quantitative principles that remove or at least

reduce to a minimum the growth of unearned income that is causing the

unsustainable debt growth.

01: INTRODUCTION.

Recent financial crises around the world,

beginning in the

In recent decades, thousands of learned papers

and articles have been written about the phenomenon of rapidly expanding debt

but little work has been done on debt growth from a structural or systemic

point of view. Credit expansion has long been seen as a function of the demand

for new credit moderated predominantly by its price, the risk perception of the

borrower by the lender, the reserves financial institutions have to hold to

manage their lending risks and, in some cases, deposit withdrawals.

There is now overwhelming evidence to suggest

the existing debt management system is dysfunctional. The best efforts of the

world’s monetary authorities have failed to prevent excessive debt growth. Debt

levels have continued to expand much faster than measured nominal economic

output despite periods of turmoil in the world economy, high or low interest

rates, widespread changes in financial regulation and even bank bailouts. This

suggests a more fundamental cause of debt growth exists outside the present

financial architecture that has either been taken for granted or overlooked by

existing economic theory and practice.

This paper will explore the underlying causes of

rapid debt growth and what can be done to prevent excessive debt growth in the

future. Later papers will examine other initiatives that might then be taken to

improve

Section 2 of the paper proposes that debt growth

in modern debt-based economies is predominantly caused by the generation of

unearned income in the form of interest paid on bank deposits 03. Modern developed countries operate on a

debt-based financial system whereby nearly all deposits arise from borrowing

debt at interest through the banking system.

The paper shows how unearned income arising from the payment of interest

on deposits causes exponential debt expansion 04.

02 Arguably Northern Rock in the

03 Earned income is the income generated from

the production of goods and services that form part of the Gross Domestic

Product (GDP). Unearned income is income arising from the payment of interest

on bank deposits that is unproductive and does not add to GDP.

04 The decision whether to save or invest

unearned income depends on the real interest rate (the difference between the

interest rate paid and inflation) and the perceived risk weighted financial

returns available in the investment sector. If real interest rates are very

low, as in

To test the unearned income hypothesis, Section

3 models a simple economy. Figure

Section 4 examines the economic transformation

that occurs when deposit interest is introduced into the simple economy model

shown in Figure 1. In Figure 2, deposit

interest in the form of unearned income introduces inflation into the model and

also stimulates debt growth, thereby proving the basic hypothesis linking

deposit interest to debt growth.

Equations are provided to show the debt growth is exponential. The

analysis of Figure 2 shows that debt expansion and inflation are both readily

quantifiable, and it demonstrates why, in practice, almost all price is

inflation 05. Figure 2 shows

how the pool of unearned income arises incrementally from payment of interest

on bank deposits but, in aggregate, remains outside it. The increment of

unearned income from each production cycle is permanently transferred to the

investment sector while the debt giving rise to it remains a burden on the

productive sector.

Section 5 describes what happens when a country

such as

Having proven the main thesis about debt growth,

theoretical support for it is offered in Section 6 by introducing a new debt

model that has been derived from Irving Fisher’s well-known Equation of

Exchange that dates back to 1912 (Fisher, 1912, Manning, 2009). The revised

Fisher Equation supersedes the original Fisher Equation of Exchange because it

takes into account the growth of an independent investment sector based on

unearned deposit income 06. My* Vy mirrors MV in Fisher’s original equation, which didn’t take into account

the effect of interest-bearing debt. The paper shows how debt interest is

compounded exponentially.

05 The simple economy of Figure 1 has very

little if any inflation while in the economy shown in Figure 2 inflation

in the productive economy is linked directly to the deposit interest

rate. Figure 3 shows how total inflation

has accelerated as developed economies have become more and more dependent on

interest-bearing debt. This paper proposes that nearly all the inflation shown

in Figure 3 arises from unearned deposit interest so that in practice all price

arises from inflation.

06 Quite the opposite of previous work (such

as Snyder, 1940) whose early support for monetarism was based on empirical

statistical analysis.

In the following Section 7, an entirely new

concept of systemic inflation is

discussed in some detail. In the debt

model annual systemic inflation is roughly 0.5*(M3 minus repos)* I*K caused by the

interest rate I% paid on deposit interest and K is (1 – the tax rate T paid on

the gross deposit interest). The study shows there is no mechanism within the

existing debt-based financial system to directly manage inflation and that

orthodox interest rate policy works through the debt servicing requirements of

the investment sector. It establishes two primary concepts:

-Individually it is possible to save debt-free

money but in aggregate, it appears difficult, if not impossible, to save earned

income generated from debt.

Conceptually, from Figures 2 and 4, non-productive “saving” in the debt

system reduces the money available for consumption, resulting in either a fall

in prices or a fall in consumption. In practice consumption usually falls much

faster than prices because incomes are “sticky” 07. Earned savings 08 therefore tend

to produce a loss of consumption capacity from the productive economy unless

they are replaced by net non-income capital borrowing and consumer debt 09, Db in the revised Fisher Equation of Exchange.

- Inflation in the existing debt system is

systemic and unavoidable. Orthodox interest rate policy only briefly suppresses

systemic inflation at great economic cost to the real productive economy and

the wider community.

Section

8 sets out the historical debt growth in

Instead

of being used for consumption where it would cause rampant inflation as it is

represented by systemic inflation .

Section

9 contains a brief review of the way culture and institutions have contributed to

the lack of awareness of the issues addressed in this paper.

The

overall conclusions from the paper are that unearned income in the form of

deposit interest is the direct cause of the problem of excessive debt, and that

consequently, debt growth and its accompanying systemic inflation can only be

managed effectively by greatly reducing and preferably removing the payment of

interest on bank deposits.

Section 8 sets out the historical debt growth in

Section 9 contains a brief review of the way

culture and institutions have contributed to the lack of awareness of the issues

addressed in this paper. Historically,

The overall conclusions from the paper are that

unearned income in the form of deposit interest is the direct cause of the

problem of excessive debt, and that consequently, debt growth and its

accompanying systemic inflation can only be managed effectively by greatly

reducing and preferably removing the payment of interest on bank deposits. In

the absence of multilateral agreements 12 to reduce or eliminate

deposit interest, unilateral action is feasible 13 but it requires

carefully constructed financial instruments to manage cross border capital

flows 14.

07 “Sticky” is the term used in economics to

describe resistance to downward pressure on variables like incomes and prices.

For example, wages are “sticky” because it is very difficult in many countries

to lower them once they have been increased.

08 Not to be confused with savings arising from

UNEARNED income referred to above.

09 As happened in the United States where

until recently consumption was maintained by growing household and consumer

debt until consumers became debt-saturated and could no longer meet their

debt-servicing obligations as discussed briefly in section 4 of this paper.

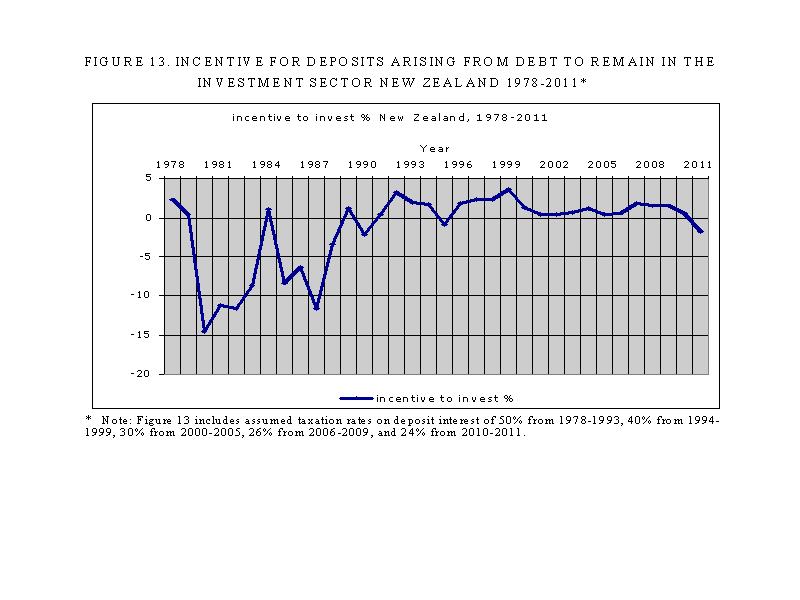

10 See Figure 11. The incentive to invest is

(M3 minus repos)*I*K/GDP(d) – Inflation% where I is the interest rate on

deposits and K is (1-the tax rate on interest). When I =0 there would be little

incentive to invest other than human nature. Man has always “saved for a rainy

day” and that would continue. When I is close to zero there will be little or

no inflation.

11 There was arguably a housing bubble but that

arose directly from the mechanics of the debt system as described in this paper

and not from speculative debt (see paper section 6 and Db in the debt

model)

12 For example, through the Bank for

International Settlements, the International Monetary Fund and the World Bank.

13 As will be shown in Papers 2, 3 and 4 of

this series.

14 The situation is different for different

countries.

02. THE DEBT

PROBLEM.

The interest-bearing debt financial system in

use all over the world today evolved from the fear King William III of England

had in 1694 for the wrath of his subjects were he to increase their taxes to

pay for his wars in Europe. Afraid of a

political backlash and bereft of the will to responsibly address his financial

difficulties, King William borrowed from a group of wealthy citizens. In doing

so, he put off the day of reckoning by pledging future taxes in perpetuity to

fund his debt. Future taxes had to be pledged because previous experience had

taught lenders the Crown was not fully creditworthy 15. The lending

arrangements were written into law in the Tonnage Act of 1694. By that means

“modern” banking was born in the form of the Bank of England. Since then, debt

expansion has gradually accelerated, more recently aided by increased

automation within the banking sector and on-going financial deregulation. The point has now also been reached where the

role cash transactions play in generating measured economic activity has all

but been eliminated in the developed western economies. That has happened

despite the fact that cash, being debt free and interest free, provides a

continuous and costless means of exchange as long as it is in circulation.

Instead, cash has progressively been replaced by expensive interest-bearing

debt created for profit by the commercial banking system 16. In most developed countries, cash makes

up 3% or less of the broad money supply,

and much of that circulates outside the productive economy 17.

Unlike the famous greenbacks printed and spent into circulation by the

15 The previous King, James II, defaulted on

his debt ruining many of those who had lent him money.

16 The elimination of cash is quite recent. In

17 In the “black” unmeasured economy for

example, such as drugs, gambling and other illicit activities. In

18 The central bank/treasury makes a profit

from selling notes and coins that cost much less than their face value to

produce. The profit is called

seigniorage.

Many trillions of dollars of interest-bearing

debt are now being added to the world’s economies every year. It is now widely

acknowledged such rapid debt growth is unsustainable because debt costs are absorbing

a disproportionate and growing share of earned incomes. The existing monetary

authorities have proved incapable of managing debt growth short of financial

collapses such as the one that occurred during the recent worldwide crisis that

began in 2007. Logically, if the present financial system is unable to cope

with excessive debt growth, there must be some other mechanism at work that

does not fall within existing economic theory.

This paper proposes the alternative view that

debt growth in modern economies is predominantly caused by unearned income in

the form of interest paid on bank deposits 19. The paper shows that

whenever interest is paid on deposits a corresponding debt is created somewhere

else, usually in the productive economy.

That makes most of the debt giving rise to deposit interest a structural part

of the productive economy. The interest has to be paid by the productive

economy or from asset inflation and must be included in prices. The only ways to keep prices stable when

interest is being paid on deposits are to increase productivity or to reduce

disposable incomes 20.

In the debt system the debt is created before

its corresponding money deposit 21. Since unearned deposit income

cannot come out of thin air it must arise from new debt. Without new debt there

can be no new money. Paying unearned income in the form of deposit interest

demands that new debt be created within the productive economy to fund it.

Otherwise deposits in the productive economy would keep falling 22

as they are transferred from the productive sector to the investment sector or

paper economy. In the debt system there isn’t enough money in the productive

economy to pay depositors interest on their deposits, unless it is first created

into existence to pay to them. As long as unearned income deposits continue to

increase, so must their corresponding debt be carried as a permanent burden

either in the productive economy or through asset inflation. The generation of

new debt in the productive economy has been growing beneath the modern economic

radar screen for many decades. If this new view of debt growth can be proved to

be correct, either a way must be found to slow or stop paying interest on

deposits or the world’s debt-based economies must face imminent financial

collapse as the debt servicing demands become unsustainable in the productive

economy.

In practice the collapse has already begun in

the

Some readers may at first sight see some

similarity between parts of this paper and earlier proposals 23

supporting the inflationary issue of interest-free credit. This analysis,

especially section 4 of this paper clearly demonstrates that is not the case.

19 Deposits and debt go together but they are

not the same. For every dollar of debt there is a dollar deposit somewhere.

First someone signs a loan (debt) agreement with the bank. When the loan is

drawn down (activated), a corresponding deposit is entered into the borrowers

account. The debt (loan) and the deposit are numerically equal but the debt is

an asset in the bank’s books and the corresponding deposit is a liability in

the bank’s books. Deposit interest usually, though not always, makes up a large

part of the interest borrowers pay on their loans. Loan interest = Deposit

interest + the bank margin or spread.

20 Raising interest rates to manage inflation

causes a reduction in consumption capacity (Manning, 2009)

21 The loan agreement with the bank always

precedes the deposit appearing in the borrowers account.

22 This would produce a deflationary spiral in

the productive economy because there would be less money circulating there to

produce the same amount of goods and services.

23 Such as C.H. Douglas’ ideas on

social credit

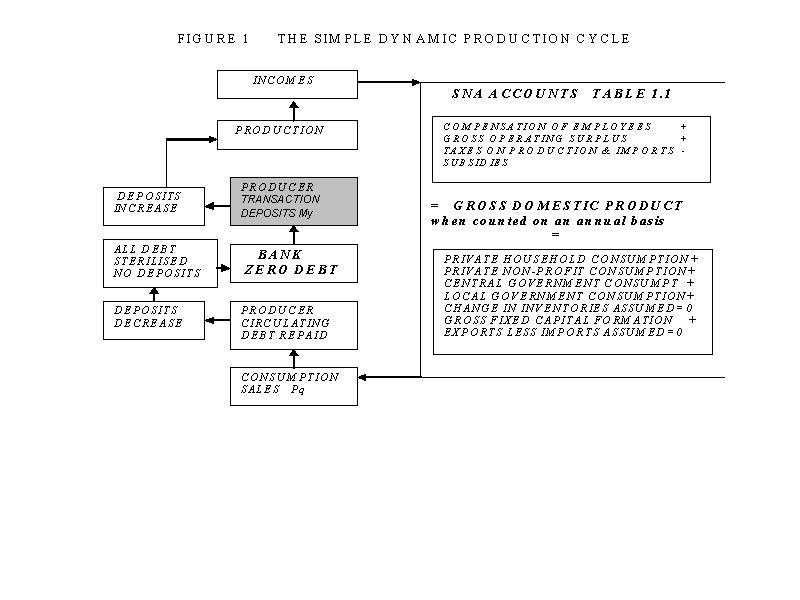

03. THE SIMPLE ECONOMY.

The

first step in revealing how the present debt system works is to show how a

simple debt economy can function without large-scale

debt expansion and without deposit interest 24. It’s close to the

way economies used to work when they were based on cash rather than debt.

The

simple dynamic debt economy is shown in Figure 1. Figure 1 satisfies the

international System of National Accounts (SNA) in use worldwide except that it

assumes for simplicity that a country has a balanced international trade

account and that business inventories are stable.

The

first step in revealing how the present debt system works is to show how a

simple debt economy can function without large-scale

debt expansion and without deposit interest. It’s close to the way economies

used to work when they were based on cash rather than debt.

The

simple dynamic debt economy is shown in Figure 1. Figure 1 satisfies the

international System of National Accounts (SNA) in use worldwide except that it

assumes for simplicity that a country has a balanced international trade

account and that business inventories are stable.

Click here to see FIGURE 1 :THE SIMPLE DYNAMIC PRODUCTION CYCLE.

{kind=link}

Conceptually,

there is no residual debt after any individual production cycle, and no

residual deposits. Each cycle in Figure 1 is self-clearing and the debt is self

–cancelling 25. Nor can there be any aggregate earned savings 26. If there were, the cycle would not be self-clearing.

Inventories would change and/or prices P would change and/or output q would

change. In sum, what is produced is sold,

including new capital goods. Figure 1 allows for the transaction deposits My to change over time and for

prices P and output q to also change according to the institutional rules in

place for the time being, productivity growth and population changes. As

described below, the simple model in Figure 1 does not need to make specific

provision for a “market” in existing capital goods or for their progressive

depreciation over time. In practice, the basic production cycle doesn’t

literally “pulse” as shown in Figure 1. Instead there is an ongoing stream of

production and consumption, a corresponding quantum of transaction deposits My continuously in circulation

and an equivalent quantum of deposits always in bank accounts.

24 The simple model economy assumes that no interest is

paid to depositors on the account balances.

25 Interest on any production debt is included in both

the income (production) and consumption sides of Figure 1 and so is self

cancelling, but increases in interest (bank spread) will lead to cost inflation

and vice versa.

26 For each individual who has “earned

savings” others must carry a corresponding amount of consumer debt.

It does not matter how many transactions there

are in a production chain, or when they take place 27. Each transaction follows the

cycle shown in Figure 1.

The

production cycle shown in Figure 1 uses the transaction deposits My to produce capital goods as

well as goods and services for consumption. The capital goods make up the

“Gross Fixed Capital Formation” shown in SNA Table 1.1 on the lower right in

Figure 1. Figure 1 assumes the producer of a capital good sells it to other

existing deposit holders for the time being, so its purchase price comes out of

employee incomes and the gross operating surplus. The banking system

intermediates among deposit holders to enable such exchanges of capital goods

to take place. The borrower repays loan

principal by transferring future income to the lender. The lender can then

consume the repayment or re-lend its purchasing capacity to others who wish,

for the time being to consume more than they earn. Such arrangements are a matter of agreement

between the parties and will usually include the payment of interest. Such

payments are like borrowing from a non-bank finance company. They involve a

transfer of wealth (future income) from the borrower to the lender but they do

not affect the total amount of bank deposits.

There is no inconsistency between the interest-free system of Figure 1

and the idea that willingness to delay consumption is “worth” an interest

premium.

In the

absence of interest on deposits, the system is in balance and there is no inflation.

A

capital good would typically be put to good productive use to generate

additional income in subsequent production cycles. The transaction deposits My, incomes, the gross operating

surplus and q would all rise to accommodate the real growth from new capital

goods so repayments could be made from the economic expansion. That’s why, as

shown in Figure 3, there was no inflation in

27 Danks (1955) pp. 12-15

28 In some

countries, investment banking became widespread, pooling cash and deposits to

fund capital investments such as rail, shipping and other industrial expansion.

Sales

and transfers of capital goods mean the banking system is left with debtors and

creditors in like amount at the end of the production cycle when My is conceptually

cancelled. That distributive effect

leaves some players in the economy with net deposits and some with net debts,

and that, as will be shown below, is where the problems with systemic debt

expansion begin as soon as interest is paid on system deposits.

In an

interest-free environment, the chains of transactions needed to make productive

investments in infrastructure, whether public or private, are the same as those

shown in Figure 1. Investment in infrastructure made by a government or other

public body is traditionally funded from taxation. If there are sufficient

labour and material resources available, it could also be funded using new

producer transaction deposits My within the context of Figure 1.

In that case repayments are typically met in the form of (sometimes

extra) taxes and levies. Since in Figure 1 the cost of such goods and services

are stable, they are known. Private contractors bid against each other for

public work. They do this on the basis of technique, method, and organisation.

Contrary to what some authors might seek to suggest (Danks, 1955), there is no

conflict in such cases between private enterprise and an interest-free economy.

29

The

story is a little different for unproductive capital goods such as

residential housing where the capital expenditure does not increase production beyond

the construction phase. Aside from increasing their work efficiency or working

longer hours, most homebuyers have to pay for their home from their future

earnings or by realising capital gains because they lack a new independent

income stream to pay for the capital good. This greatly accentuates the

distributive effect already referred to because residential homebuyers become

heavily indebted to other players in the economy 30. Until about 200 years ago

housing formed only a small part of economic activity. Since then, and

particularly during the twentieth century, housing expectations in modern

economies have risen sharply to the point where, in

Despite

the various issues around capital goods, the simple economy works very well,

especially where appropriate income redistribution is used to ensure a socially

acceptable level of housing is affordable to all.

People

all over the world owned property, borrowed and loaned money and successfully

conducted all manner of economic transactions long before interest was

routinely paid on bank deposits (Danks, 1955) 32. Payment of interest on bank deposits relates

to the structure of the debt system itself, not to interest-bearing contractual

obligations between consenting parties where one party chooses to defer

consumption and another chooses to buy the use of that party’s consumption

capacity 33 . Reducing or removing interest on deposits

would reduce or eliminate inflation, leading to stable rents and prices 34.

29 Danks, (1955) pp 48-51.

30 The

quantum of residual debt is readily quantifiable but outside the scope of this

paper.

31 Source: Statistics New Zealand Household

Economic Survey (income) June 2009.

32 Danks, (1955) pp 57-58.

33 As discussed later in the paper, the system presently

requires banks to compete for deposits but that competition would still be

possible in the absence of deposit interest.

34 Investment resource allocation would still

be based on cost-benefit analyses exactly as happens now, but with the benefit

that finance charges would play a smaller part in “efficient” allocation. In

addition, other instruments such as variable reserve ratios are available to

central banks to restrain demand for bank lending.

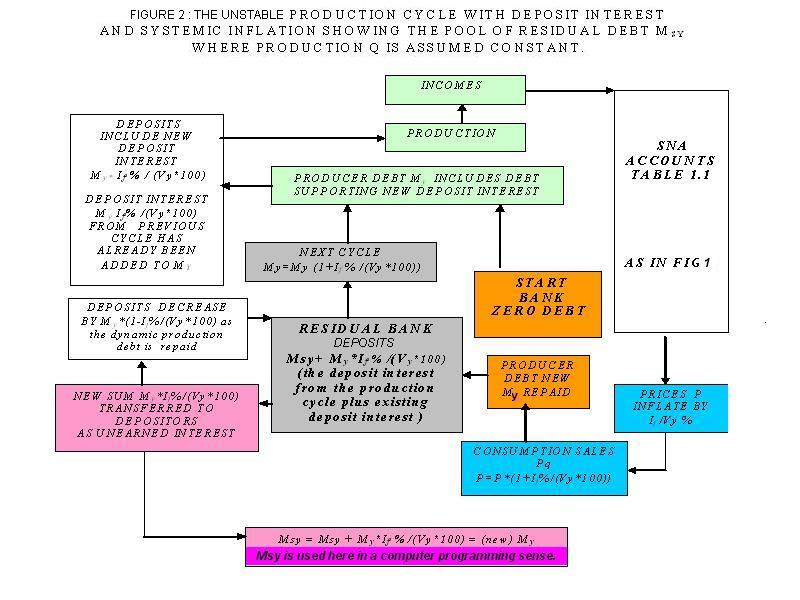

04. THE UNSTABLE ECONOMY.

Having

isolated the broad fundamental problem of debt and shown how a very low- debt

simple economy can function (without inflation), the next step is to explore

how the present system using deposit interest is structured and what causes

exponential debt growth.

The only

difference between the stable simple economy shown in Figure 1 and the unstable

economy shown in Figure 2 is the introduction of deposit interest on all bank

deposits arising from debt 35 . If Figure 2 demonstrates conclusively how debt

expands exponentially when interest is paid on deposits, then it necessarily

follows that the cause of unsustainable debt growth lies in the payment of

deposit interest.

![]() The introduction of

deposit interest If% 36 produces systemic

changes throughout the economy. In Figure 2, to enable all production to be

consumed, producers must first borrow

(and then pay out in the form of incomes) the deposit interest through

the production phase of the production cycle and then recover it by way of

increases in their prices during the consumption phase. Incomes are assumed to

keep pace with inflation. Otherwise the production cycle cannot clear itself.

The introduction of

deposit interest If% 36 produces systemic

changes throughout the economy. In Figure 2, to enable all production to be

consumed, producers must first borrow

(and then pay out in the form of incomes) the deposit interest through

the production phase of the production cycle and then recover it by way of

increases in their prices during the consumption phase. Incomes are assumed to

keep pace with inflation. Otherwise the production cycle cannot clear itself.

When

each production cycle is cleared there is residual debt and corresponding

residual deposits as shown toward the bottom left of Figure 2. Those deposits take on a life of their own

because they are reinforced by every subsequent production cycle but exist

outside it. The pool of deposit interest plays no further part in production.

Instead, it makes up what is usually called the investment sector or paper

economy that includes the non-trade sector and derivatives market. Deposit

interest acts as a debt pump, pumping more and more deposits into the

investment sector Ms while leaving the corresponding debt in the productive

sector. The investment sector is what creates the inflationary “market” in

existing assets. The deposit Ms supporting the investment sector Ds is un-repayable because it

represents unproductive unearned deposit interest that resides outside the productive

sector.

It does

not matter how many transactions there are in a production chain, or when they

take place 37. Each transaction

follows the cycle shown in Figure 2. There is no inconsistency between the

deposit interest based system of Figure 2 and the idea that willingness to

delay consumption is “worth” an interest premium.

Figure

2 does not directly specify who in the economy has the deposits and who has the

corresponding debt at the end of the production cycle (lower centre of Figure 2). However, net deposit holders emerge from the

redistribution of debt arising from the purchase of capital goods as already

discussed in relation to the simple economy in Figure 1. The production cycle

itself remains a zero-sum game but in Figure 2 the cycle is constantly being

loaded with the extra debt needed to pay the deposit interest (unearned income)

on the investment sector Ms. In addition, when interest-bearing debt is used as in Figure 2 the

consequential transfer of wealth that takes place is accelerated in comparison

with the stable economy of Figure 1

(Danks, 1955) 38.

35 The analysis in this paper uses the average

funding (deposit interest) rate counted over all of the domestic credit. The

average funding rate for

36 Net deposit interest after tax is I*K where K is (I –

tax rate on gross deposit interest).

37 Danks, (1955) op cit pp. 12-15.

38 Danks, (1955) op cit p. 12.

It

should be stressed that ownership of productive infrastructure is irrelevant

from a national macro-economic point of view. Who owns what depends on

political choice. In the case of publicly owned productive infrastructure, the

benefits of the investment are distributed directly amongst the population.

They may for example take the form of shorter travelling times for all

(tunnel), improved education facilities (school), or improved public health (a

sports centre). Where infrastructure is privately owned, the temptation to

charge users for services may be greater and the resulting profits may

accumulate in the hands of a few.

The

investment sector funded by the accumulated interest paid on bank deposits

produces nothing itself. It is paid for

through inflation of the productive sector and from realised capital gains.

Neither

the SNA (System of National Accounts) nor Figure 2 provides any direct

mechanism to enable increases in interest rates to reduce inflation. Interest

rate policy works through borrowers (such as home mortgage holders), the

holders of the Ds debt that supports

the accumulated deposit interest on bank deposits. Raising interest rates

typically increases their interest payments on mortgage and other debt, and

thereby reduces their purchasing power. Raising interest rates to “manage”

inflation, as is commonly done under orthodox economic policy, transfers even

more consumption capacity from the productive economy to unearned income for

deposit holders in the investment sector 39.

39 The quantum can be estimated from equations

1-3. On an annual basis it is roughly the change in the deposit interest

rate*K* (the domestic credit (Ddc). At the moment, based on the Model

calibration for

Figures

1 and 2 provide an alternative insight into the real productive economy. The

orthodox view is that people and firms borrow to invest on the basis their

financial return will exceed their costs including interest. Their net profit

after tax is often put in the bank and the holders of those banked profits then

expect to be paid interest on it. Figure 2 shows such deposits (or other earned

“savings”) by their nature force others in the economy into new debt to replace

those savings in the economy if production and consumption levels in the

economy are to be maintained. Figure 2 also shows that any deposit interest

paid on those “savings” deposits increases My and inflationary pressure in

the productive economy. This is discussed further in section 7 of this paper

where it is proposed that traditional “savings” as set out in the System of

national Accounts (SNA) represent the difference between increases in consumer

debt plus new bank debt for the purchase of capital goods on the one hand and

principal repayments relating to previously purchased capital goods on the

other. As shown in section 6 of this paper, those “savings” are typically

offset by the bubble debt Db in the revised Fisher Equation of Exchange. When interest rates are

increased to manage inflation the higher deposit interest is not (immediately, anyway) compensated in wages

and other incomes. In effect, producers and income earners are forced to gift

to investors “savings” they do not have.

Click here to view FIGURE 2 :THE UNSTABLE PRODUCTION CYCLE.

{kind=link}

In

Figure 2 the reduction of consumers’ purchasing power forces prices P down. The

large-scale collateral damage from the loss of consumers’ purchasing power is

that production q in Figure 2 falls in turn, leading to unemployment and

recession.

Deposit

interest prevents the efficient functioning of the economy unless the

interest is fully compensated in

employee incomes and the gross operating surplus. Orthodox economic policy

typically fails to match incomes to inflation because of arbitrary limits

placed upon measured CPI (Consumer Price Index) inflation. Such mismatches

create the boom and bust features so typical of modern business cycles as

interest rates change. They also accentuate the drift of wealth away from wage

and salary earners towards the holders of deposit interest.

The key

to understanding Figure 2 is that only that part of the domestic debt that is

not already committed as Ds to fund the unearned income pool

or to Db as “savings” is available for

use in the productive economy.

Debt

can only be used once. If the debt Ds is used to support

the pool of unearned deposit income it cannot also be used to fund the

production cycle unless the corresponding Ms deposits are directly

re-invested in new production or productive capital goods.

In

aggregate, re-investment of deposits arising from the debt Ds into the production cycle is

not common, in part because there is a financial incentive (discussed later)

for them to remain in the investment sector, and in part because saving is

instinctive. People have always saved. Instead, holders of unearned income

deposits tend to find the investment “game” more profitable, trying to increase

their share of those deposits by trading among each other in existing capital

goods such as equities, property and financial derivatives. Figure 2 shows that

the investment sector debt creates an exponential expansion of unearned income

Ms given by the

expressions (based on annual figures) 40

Ms1

= Ms0*(I+I1*K1)+11*(My1*Vy1)*K1

where Ms0 = 0 (1)

Ms2

= Ms1*(1+I2*K2)

+ I2*(My2*Vy2)*

Msn

= Ms(n-1)*(1+InKn)+In*Myn*Vyn)*Kn

(3)

Where Msn is the pool of deposits representing the debt

Dsn that has been created to fund deposit interest.

I1 ….. In is the average deposit interest through each

of the years 1 …. n

My1 … Myn is the average transaction deposits through

each of the years 1 ….. n

Vy1 … Vyn

is the number of production cycles during each of the years 1 …….n

K1……..Kn

is the proportion of deposit interest remaining after deduction of tax T1….Tn

during each of the years 1 ……..n

Equations

(1) to (3) are derived directly from Figure 2. They create an exponential

series, and the only difference between Figure 1 and Figure 2 is the

introduction of deposit interest. The thesis that deposit interest is the cause

of unsustainable debt growth is proven. Since the investment sector deposits Ms are largely funded

directly by the productive sector by price inflation and by realised capital

gains, if Ms is exponential, both the accumulated price inflation

and the transaction deposits My in the productive sector must

also be exponential.

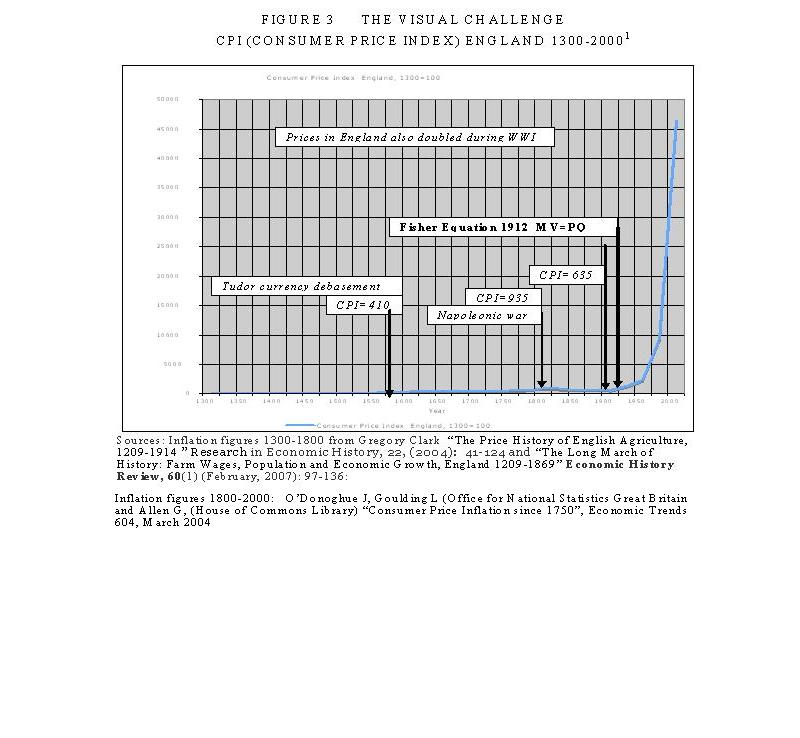

Figure

3 shows the dramatic impact of inflation in

Click

here to view FIGURE 3 :THE VISUAL

CHALLENGE CPI (CONSUMER PRICE INDEX)

ENGLAND 1300-2000. 42

{kind=link}

40 Equations (1)-(3) include the

effect of net debt Ds

directly

borrowed for investment, which is introduced in section 6 of this paper, but do

not include any accumulated current account deficit or bubble debt that also

introduce further system deposits and net deposit interest.

41 Such as the removal of the US$

gold peg in 1971, “globalisation” and its accompanying freeing up of capital

flows, the introduction of Basel I risk-based capital requirements and the

repeal of the Glass-Steagall Act in the United States.

42 Sources:

Inflation figures 1300-1800 from Gregory Clark

“The Price

History of English Agriculture, 1209-1914 ” Research in Economic

History, 22, (2004): 41-124 and “The Long March of History: Farm

Wages, Population and Economic Growth, England 1209-1869” Economic

History Review, 60(1) (February, 2007): 97-136.

Inflation figures 1800-2000:

O’Donoghue J, Goulding L (Office for National Statistics Great Britain

and Allen G, (House of Commons Library) “Consumer Price Inflation since

43 By comparison, in

New Zealand in 1893 (a crisis year – RBNZ (2009b)) production was estimated to

be about

In

Figure 2 shows how exponential growth in prices is a

structural part of the debt-based financial system. Figure 3 suggests this has been a twentieth

century phenomenon.

The price index increased from

Figures 1, 2 and 3 suggest inflation is predominantly

caused by the interest rate on deposits. In that case, an obvious way to

achieve a stable economy is to remove interest on deposits to return the

financial system closer to what is shown in Figure 1 45. Low inflation cannot be maintained in an

economy when it must increase as a function of the deposit interest I and often

faster 46.

44 In New Zealand the Consumer Price Index

(CPI) increased by 583% between March 1978 and March 2010, while during the

same period domestic credit increased by roughly 3000%. [source RBNZ table

hc3].

45 Together with stabilising the current account and

progressively retiring foreign debt.

46 Annual inflation in Figure 2 is a function of My*I*Vy, but My can be

increased by any injection of debt, such as mortgage or consumer debt, from

outside the production system which increases My instead of

I.

Reducing or removing interest on deposits would have no

impact on bank lending decisions, nor, with appropriate policy instruments in

place would it lead to excessive demand for new debt. Lending decisions relate

primarily to the creditworthiness of borrowers.

Bad lending decisions, like those in the

On-going

efforts by central banks to control Consumer Price Index (CPI) inflation have

done little to halt inevitable rises in prices within the existing

interest-bearing debt-based financial system. They have superficially succeeded

up to a point only at incalculable cost to human lives, wellbeing and

development over the past century or more while at the same time transferring

nearly all the increased wealth to the minority of people and institutions

holding large deposits in the banking system. While the quality of life of some

of the world’s people has improved during that time the improvements are patchy

and fewer than they might otherwise have been. Exponential debt growth appears

to have reached the point where the productive economy can no longer satisfy

the profit expectations of the investment sector despite excessive and

unsustainable exploitation of the world’s labour force and natural resources.

The

unearned investment sector deposits Ms shown in Figure 2 give rise

to the cumulative unearned interest income on the deposits in the banking

system. Consumer prices are also locked into exponential expansion though

normally at a lower rate than Ms itself.

Consumer

prices inflate with the deposit interest rate I*K to pay the deposit interest

on the existing My into the unearned income pool Ms. Ms also increases by the amount

of new deposits that have to be added at

each production cycle to pay the deposit interest on Ms itself as well

deposits arising from bubble debt Db and the accumulated current

account deficit. 47

Figure

2 provides for numeric inflation equal to I*K*My*Vy to fund the interest on the

productive sector. If Ms is not less than or equal to My*Vy the interest difference would have to be drawn

from My itself which means producers are paying some

of the costs directly from their real incomes. Those holding debt backing

deposits arising for example, through the use of credit cards and new mortgages

that are used to buy non-productive capital and consumption goods that have

already been produced also have to find some way to fund the interest on them.

That debt can only come from realised capital gains on the sale of existing

assets or from “bubble” debt Db. Bubble debt injections allow wage and income earners to consume beyond

their financial means 48 but they are offset by “savings” in non-productive speculative

investment. Some leakage of Ms deposits back into My or leakage of My deposits out of My (as earned savings, for example) is also

possible. Any such net flows will destabilise the production cycle as

previously discussed.

Since

nearly all price is inflation the value of assets and goods and services would

become far more stable and predictable if interest on deposits, and hence

inflation were to be reduced or phased out.

Interest destroys value. The present system not only guarantees

unsustainable exponential debt growth, it also guarantees an exponentially

increasing transfer of wealth from borrowers to bank deposit holders. This

worsens the already critical problem of inequitable income distribution typical

of much of the developed world, especially

47 Db is described at section 6 of this paper.

48 The “keeping up with the Jones’s” syndrome

is encouraged through advertising and social pressure. The concepts of systemic

inflation developed here are very close to the “one-for-one” link between

interest and inflation predicted by Irving Fisher in his famous “ The Theory of

Interest”, New York, Macmillan, 1930 that has never before been proven.

05. The unsustainable economy with

foreign debt.

Recent

decades have seen vast changes in trade and capital flows giving rise to “free

trade”, globalisation and financial deregulation. The collapse of the sub-prime

mortgage market in the

Large-scale

foreign debt is a relatively new phenomenon in modern economies 49.

Until 1971 most of the developed world’s economies operated most of the time on

a gold standard using fixed exchange rates (albeit for a time indirectly

through what was known as the US$ gold peg)

US

President Nixon was forced to abandon the

49 Though national bankruptcies were far from

unknown in earlier times. For example the French Court of King Phillip IV was

bankrupted in the early 14h century having borrowed heavily for a

failed crusade to the holy land. Other

instances were King Phillip II of

50 In times of crisis some countries were

forced off the gold standard. This occurred during WWI when

51 The

Bretton Woods conference was where the WWII allies agreed on the

framework for the post WWII financial architecture, including he World Bank and

the International Monetary Fund.

Progressive

deregulation of capital flows, the growth of unearned income from interest on

deposits (Ms) and the

introduction of ever more complicated derivative trading instruments have long

since destroyed the principle of automatic exchange rate adjustments based on

real cash flows. Many debtor countries

including

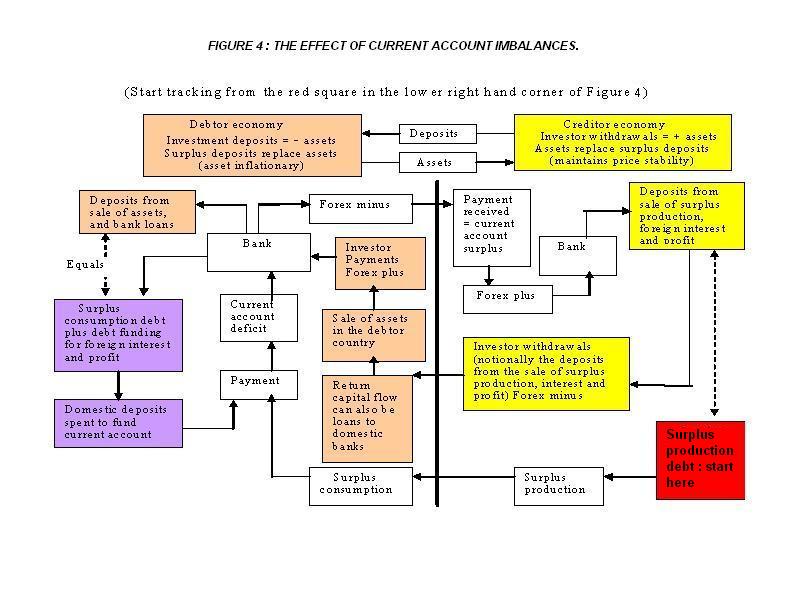

Figure

4 is the same as Figure 2 except that it makes provision for current account

deficits. It clearly demonstrates how

“carrying” the current account deficit through the productive economy as set

out in the System of National Accounts increases inflation throughout the productive

economy as well as increasing the pool of unearned deposit income that makes up

the investment sector.

Click here to view FIGURE 4: THE EFFECT OF CURRENT ACCOUNT IMBALANCES.

{kind=link}

The

balance on external goods and services is shown in Table 1.1 of the SNA as a

(foreign) debt arising outside the production cycle shown in Figure 2 52. The trade deficit for any period forms part of

the nation’s accumulated current account. Theoretically, with a floating

exchange rate and open capital markets there should not be any surpluses or

deficits in the current account. Persistent current account deficits should

produce a lower exchange rate, automatically correcting the inwards and

outwards flows of goods and services. In practice a single monetary policy

instrument such as the Official Cash Rate (OCR), as it is used in countries

like

Current

account deficits result from aggregate withdrawals from the accounts of importers

and parties repatriating profits or otherwise transferring funds offshore.

Transfer of funds abroad should result in a corresponding sum of bank deposits

in offshore beneficiary accounts 54. Those offshore deposits are used to buy investments that are recorded

in the debtor country’s financial (capital) account

52 The trade deficit is subtracted from the consumption

side in SNA Table 1 so the trade account results in “saving” when it is in

surplus and “dis-saving” when it is in deficit. The deficit is, for those

countries whose currency is not a reserve currency, necessarily met by

borrowing on the current account accompanied by compensating inward capital

flows.

53 There is now a considerable body of research on this

but the statement is obvious from high school mathematics. You can solve for y

with one variable x in y=(f)x , but not in y= (f)x+(f)z .

54 Any good primary economics textbook should set out the

process.

55 For the

56 NIIP NZ$ 176.6b–derivatives NZ$ 2.0b–managed funds NZ$

3.7b–overseas shares held by NZ residents NZ$ 10.6b.

Within

the SNA international accounting system, a current account surplus is

shown as “Saving”

In the

SNA National income and outlay account the current account balance is shown as

part of the nation’s cash flow but it is, apparently, except for goods and

services, kept outside of the

production system. In practice, current account shortfalls seem to result from

deficit balances relating to productive activities and the foreign borrowing is

needed to meet profit and interest payments on the offshore debt and deficits

from current transactions 61. To allow for this, transaction deposits My shown for

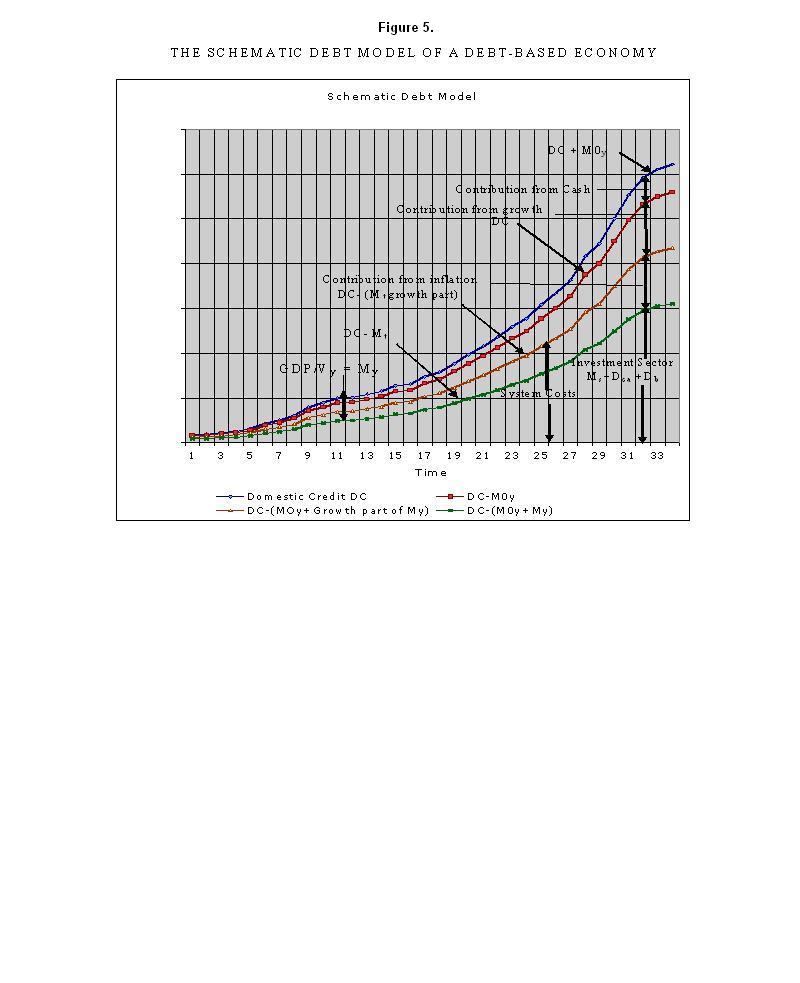

Click here to view FIGURE 5: THE SCHEMATIC DEBT-MODEL OF A DEBT-BASED

ECONOMY.

{kind=link}

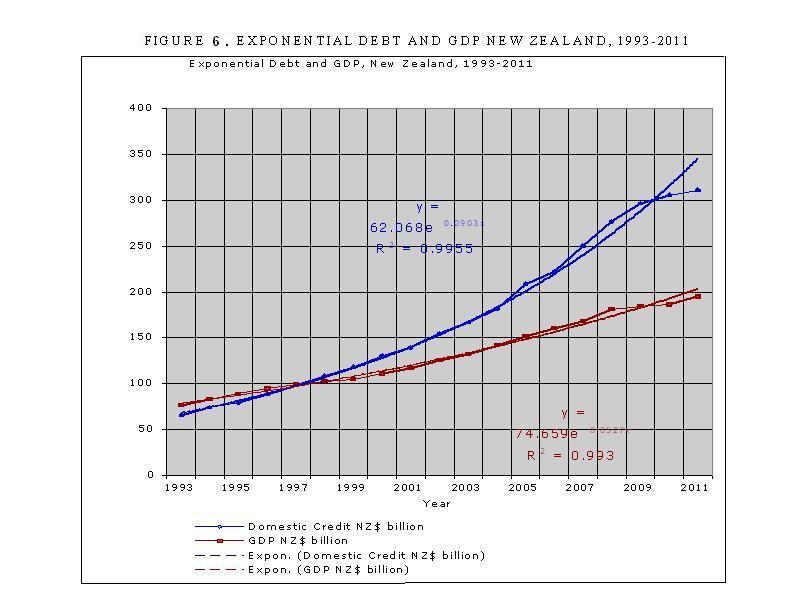

Click here to view FIGURE 6: EXPONENTIAL DEBT AND GDP IN NEW ZEALAND

1993-2011.

{kind=link}

57 The SNA National income and

outlay account shows a current account surplus, “investment income from the

rest of the world, net” on the income side and the residual “Saving” on the

“use of income” side.

58 As shown in the National Accounts; National income and

outlay account, Table 1.2 .

59 Shown on the right hand side of Figure 1 as “exports

less imports”.

60 The SNA National income and outlay account is suspect

not just over the issue of saving but also because it incorporates an imaginary

number “consumption of fixed capital” to allow for depreciation that has

nothing to do directly with cash flows in the productive economy. “Consumption

of fixed capital” belongs only to assessments of net capital stock. The

appropriate figure to use for income/outlay purposes is “principal repayments

on capital goods”.

61 Statistics NZ Balance of Payments and International Investment

Position, March 2009, Table 10.

62 In line with the common saying that countries with

current account surpluses export inflation while those with current account

deficits import inflation.

63 Though in practice there is an on-going transfer through

the cycle rather than a lump sum at the end.

06. THE DEBT

MODEL.

The first version

of the debt model was published in the paper:

Manning, L “The Ripple Starts Here: 1694-2009 : Finishing the

Past”, presented at the 50th

Conference of the New Zealand Association of Economists (NZAE),

While the debt

model is based on the volume of debt, it is unrelated to earlier volume-based

reform proposals like those of Social Credit that failed to offer a viable

theoretical basis to support them.

The premise in both

the debt model and Figure 2 is that the circulating deposits and cash My = Prices P x output q where q

is the quantum of domestic output produced by My over a single cycle. Taken over a whole year, the SNA definition of

Gross Domestic Product GDP is given in the debt model by mathematically

integrating the expression Pq* Vy, where Vy is the number of times the

circulating deposits and cash My are used during the year 65.

The SNA should reflect

an expression of the original Fisher Equation of Exchange as shown in Figure 1 66. The only difference is that the money supply

M in the Fisher equation of exchange included hoarded cash, whereas in the debt

system shown in Figure 2 for practical purposes there is now very little cash

contributing to measured GDP.

In Figure 2 My cannot include hoarding of

debt beyond the term of the production cycle because all the productive bank

debt giving rise to My is conceptually repaid at the end of the cycle 67.

64. http://www.nzae.org.nz/conferences/2009/pdfs/The_Ripple_starts_here_1694-2009__Finishing_the_Past.pdf

. Non-members can access the paper by Google search: NZAE The Ripple Starts

Here (use “quick view”).

65. The contribution of cash transactions in industrialised countries is

now (very) small.

66. The Fisher equation has been very widely discussed in relation to the

economic difficulties arising from the sub-prime mortgage defaults in the

67. As previously noted, in practice there is a continuous flow of

production and consumption so the deposits and cash My are always present, but they are being used in the production cycle,

not hoarded.

At any point in

time there are five broad blocks of deposits in the domestic financial

system.

They are:

Mt The transaction

deposits representing the productive debt My - M0y so:

My

= Mt + M0y (4)

Mca The accumulated

domestic deposits representing the sale of assets to pay for the accumulated

current account deficit (see section 5 of this paper for details).

M0y The cash in circulation

included in My and used to contribute

to productive output.

Ms The net after tax accumulated deposits arising from

unearned deposit income on the total domestic banking system deposits M3 (excluding

repos) 68.

(M0-M0y) Cash hoarded by the public and not used

to generate measured GDP.

In this paper the

total of these deposits, that is, Mt + Mca + M0y + Ms , is provisionally assumed to

be the M3 (excluding repos) monetary aggregate published by most central banks monthly

less the amount of cash in circulation M0 except for the part M0y that is included in My. In this paper M0y is assumed to have the same

speed of circulation as My. In industrialised countries, the contribution of cash transactions to

the measured output of goods and services (GDP) has been declining in recent

decades and their contribution to the GDP has been provisionally calibrated for

the purposes of this paper 69.

In this paper, the

total debt in the domestic financial system is assumed to be the Domestic

Credit, DC debt aggregate published by most central banks monthly.

At any point in

time there are four broad blocks of domestic debt in the domestic

financial system. Three of them together add up to DC such that:

DC = Dt + Dca 70 + Ds (5)

Where :

Dt is the productive debt supporting the

transaction

Dca is the whole

of the debt created in the domestic banking system to satisfy the accumulated

current account deficit 71.

Ds is the residual debt to balance equation (5)

68. Repos refer to inter-institutional lending

69. More accurate assessment of

the cash contribution to GDP over time requires further detailed study.

70. Arguably the accumulated sum of capital transfers could be included here,

in which case the net international investment position (NIIP) would be used

instead of the accumulated current account. The decision affects the size of

the “residual” Db.

71. This is greater than the

monetary deposits Mca because the

banking system may have sold commercial paper to borrow foreign currency to

satisfy the foreign exchange settlement as shown in Figure 4.

The fourth block of debt is :

Db, the virtual “bubble” debt, the

excess credit expansion or contraction in the banking system such that Ds - Db = the debt supporting the accumulated deposit interest Ms defined above. Db can be positive or negative

as discussed further below in relation to Figure 9.

There is also a

fifth block of debt Is that is, conceptually, not bank debt .

Is is

the total debt accumulated by investors to buy capital goods arising from

Saving Sy = S/Vy.

where S is national saving measured as gross capital formation less repayments

of principal made on all existing capital goods.

Conceptually

the investor borrows the purchase price of the capital goods from employee

incomes and the business operating surplus. The investor pays the investment Iy

=I/Vy = Sy = S/Vy to the producer and the money is used

to retire the outstanding part of My relating

to the investment in question. The principal repayments on productive capital

investment, being part of Iy (=Sy)

is included together with the interest on the investment principal as a

production cost in the subsequent production cycle loans My,

allowing the investor’s debt to producers to be repaid over time.

The predicament of

new homeowners is quite different. They cannot service their debt because they

cannot, conceptually earn more than they were before they bought their new

home, because the home itself is nearly always unproductive. There is no new

income stream from their housing investment. If economic demand is to be

maintained, homeowners must, in aggregate, rely upon increasing house prices and

refinancing of their properties, creating an aggregate “pass the baton”

systemic increase in debt.

When non-productive investment assets

are traded there is typically a capital gain because of asset inflation on

investment (Dca + Ms + the property component of Is). The new purchaser pays more for the asset

because of asset inflation, allowing the seller to retire the outstanding

mortgage debt on the property.

By definition in this paper :

My *Vy =

GDP

Ms = Ds

The cash contribution to GDP =

M0y * Vy. Therefore :

DC = (GDP)/Vy - M0y + Ms + Dca

+ Db (6)

Ms =Ds =

(DC – Dca ) – GDP/Vy + M0y - Db (7)

GDP = Vy *(DC - (Ms +Dca

+Db ) + M0y ) (8)

My = GDP/Vy

= DC - (Ms +Dca + Db) + M0y (9)

Where the terms are as already

defined above.

Equations (6 ) to

(9) are all forms of the debt model developed in an earlier paper 72.

72.

Links are provided in the conclusion to this paper.

Ms is the same format as Ms in the earlier forms of the

model. It has been freshly calibrated. Unlike the previous forms of the model

equations (6) to (9) are general and include the contribution made to the

economy by cash transactions.

In equation (7),

all the terms except GDP/Vy = My and Db are known or can be estimated

with reasonable accuracy. For the purposes of equations (8) and (9) My can be approximated using

trend-lines because it is small compared with Ms. Db is unknown but can be

approximated through the calibration as in Figure 9. The calculations in

equations (8) and (9) involve the subtraction of large numbers to get

relatively small numbers, which leaves them sensitive to modelling and data

error.

If Ms , calculated as “the

accumulated deposits arising from unearned deposit income on the total domestic

banking system deposits M3(excluding repos) ” as defined above,

agrees more or less with that calculated in equation (7), bearing in mind the

value of Mb , the proposition

that debt growth is determined by deposit interest will be proven. The model will require further calibration as

further data becomes available. Despite

that, it is self-evident Db will be positive during periods of rapid expansion, particularly as

bubbles form, and will become negative during periods of rapid contraction,

particularly as bubbles collapse. The classic case of this in

The dependence of the

gross domestic product (GDP) on the Domestic Credit DC and the interest rate on

bank deposits in the modern cash-free economy from which Ms is calculated has profound

implications for economics.

In the light of the

worldwide financial chaos of 2007-2009 the indicative debt model shown in

Figure 5 provides a powerful argument in support of public control of a

nation’s financial system.

Click here to view FIGURE 5 : THE SCHEMATIC DEBT MODEL OF A DEBT-BASED ECONOMY.

The vertical axis

in Figure 5 applies to the Domestic Credit for

It isn’t possible

to have a simpler model of the economy than equation (8):

My =Nominal GDP/Vy = domestic credit DC less (unearned net deposit

income Ms + the accumulated current account Dca + the cash

contribution to GDP M0y plus a

correction for bubble activity Db (+/-)).

Domestic

Click here to view FIGURE 6 : EXPONENTIAL DEBT AND

GDP NEW ZEALAND, 1993-2011.

It is theoretically impossible

to maintain exponential debt expansion faster than GDP expansion over an

extended period because the added debt servicing costs will always leave the

productive sector insolvent.

To avoid national

bankruptcy, each nation must maintain, in aggregate, a zero accumulated current

account deficit.

A first

approximation for the speed of circulation Vy of productive debt plus cash transactions My is given in Figure 7. Vy varies with the change in the

payments systems. Minor secondary shorter-term cyclical variability also occurs

through changes in the average time taken to pay bills. When times are tough people take longer to

pay their bills, and each change of a day in the time taken to pay them can

alter Vy by perhaps 0.25%.

The process is usually reversed in better times. Otherwise Vy reached a constant value of

about

73. Vy is estimated at the moment

so the present figures are indicative. Once further research accurately refines

the present estimates, Vy will be

sufficiently accurate for predictive purposes.

Click here to view FIGURE 7 : SPEED OF CIRCULATION Vy NEW ZEALAND 1978-2011.

{kind=link}

Note that in Figure

7, no correction has been applied to Vy for secondary increases in

payment time during recessions or decreases in payment time during economic

boom periods. The maximum correction in Vy appears to be in the

order of +/- 0.3 or up to 1.5%. The series shown is less stable from 1978 to

1989. This is possibly due to distinctly different growth exponentials

1978-1989 arising from the very high interest rates that were typical during

those years.

As shown in Figure 8, My in

Click here to view FIGURE 8 : ESTIMATED TRANSACTION FUNDING My NEW ZEALAND

1990-2011.

{kind=link}

The methodology

used to calculate Vy in Figure 8 is as follows. The GDP in

Businesses pay

suppliers monthly, and indirect payments are usually made on a monthly basis

too, so their speed of circulation is about 12 on average. Most workers get

paid fortnightly (though some get paid weekly and some monthly) so an average

speed of circulation of 26 has been assumed for that.

When the above figures are

weighted the weighted average speed of circulation is (12 * (42.7+12.3)+45 *

26)/100 = 18.3.

A similar estimate

of payment trends and a separate Vy calculation was made for each

of the other years, and a polynomial best fit curve was drawn as in Figure

8.

My was then obtained by dividing

the official GDP figure by the speed of circulation taken off the best fit

trend curve. This gives the data series

shown in Figure 9 and used when applying

the debt model.

The methodology is

easily replicable using better information about payment trends and is

applicable to any country.

Figure 8 shows the

preliminary estimate for estimated production debt and cash My in

Figure 9 shows an

indicative comparison between the residual debt Ds for New Zealand calculated

from equation (5) and plotted against the model Ms calculated as the accumulated

after tax deposit interest on M3 (excluding repos). The curve for Ms is a first approximation

because assumptions have been made on the average tax deducted from the gross

payments of unearned income (M3 (excluding repos x the average interest paid on

deposits). The tax is the average tax paid by each income-earner on his or her

total income. It is not the marginal tax rate 74. The losses from the 1987 share market crash

in

Once the tax rates

on Ms have been

accurately calibrated, the size of any debt bubble Db can be immediately

calculated. Measures can then be taken to eliminate the bubble without risking

any economic downturn.

Click here to view FIGURE 9 : BUBBLE DEBT Db AND Ms NEW ZEALAND

1978-2011.

{kind=link}

One of these, of

interest to New Zealand’s recent economic performance, relates to the impact of

banks increasing their reserves by increasing the bank spread, which is the

difference between the lending (or claims) rate they charge their clients and

the interest they pay on their customers’ deposits (their funding rate).

Were the banks to set aside some of their income for reserves instead of

feeding it into the income stream in wages and profits the effect would be

similar to the case for aggregate earned savings 75. In both cases, deposits arising from debt My supporting

the transaction deposits in the productive economy are withdrawn

from the production cycle. While earned savings, could they in the aggregate

occur, would be transferred from the productive sector to the investment

sector, bank reserves are withdrawn from circulation altogether and do not form

part of the productive money supply. Less income would then remain available to

consume the productive output. In the short term, in Figures (1,2,4), the

market would not be able to clear and either prices P would tend to fall or

output q would tend to fall as inventories rise, creating deflation and

unemployment. More typically P and q would both fall. The only other possibility is that consumers seek to replace the

shortfall by borrowing more from the bank to maintain their levels of

consumption.

Widespread borrowing for consumption purposes does not alter the

principle that in the basic economic cycle described in Figures (1,2,4) “Earned

Saving” is used to fund and repay principal on existing capital goods . Any

other “savings” must be borrowed. 76 77

Banks seek to increase their reserves when they foresee future losses

from bad debt arising during economic downturns. They then need higher reserves

because losses are drawn from the banks’ net worth that includes their reserves

78. The increases in reserves can be funded from

retained profit or by increasing the bank spread. The banks could also generate

new capital through the issue of shares, bonds, or debentures. Recent figures

for

75. Earned savings, could they

occur in aggregate, would be the portion of total productive (earned) income hoarded by consumers for later

use, for example as a deposit on a future home purchase, superannuation funds

(including funded government superannuation schemes), and worker/employer

savings schemes like Kiwisaver in New Zealand.

76. The mechanics

of unearned “saving” are outside the scope of this paper.

77. For example, “Economics

Principles and Policy” William J Baumol and Alan S Blinder, 4th

Edition Harcourt Brace Jovanovich, 1988.

78 . .Paying

losses from deposits is illegal and traditionally happens only when banks fail.

That is why some western countries, including

TABLE 1: RECENT CHANGES IN BANK SPREAD IN

|

YEAR |

2005 |

2006 |

2007 |

2008 |

2009 |

2009 |

2009 |

2009 |

2010 |

|

|

MAR |

MAR |

MAR |

MAR |

MAR |

JUN |

SEP |

DEC |

MAR |

|

% spread |

2.37 |

2.10 |

2.04 |

1.67 |

2.85 |

2.99 |

2.85 |

2.76 |

2.55 |

|

claims |

7.51 |

8.14 |

8.36 |

9.01 |

6.96 |

6.52 |

6.39 |

6.22 |

6.16 |

|

deposit |

5.14 |

6.04 |

6.24 |

7.34 |

4.11 |

3.53 |

3.54 |

3.54 |

3.60 |

(Source RBNZ Table hc10)

Mainly to increase their reserves, the banks operating in

79. Bank reserves do not form part of

the “money” supply. Arguably March 2008 represented a low point in the banks’

historical spread, but the economic impact of the withdrawal of bank reserves

from earned incomes was nevertheless very real.

07. SYSTEMIC

INFLATION AND INFLATION POLICY.

Click here to view FIGURE 2 :THE UNSTABLE PRODUCTION CYCLE.

Figure 2 shows what

happens when funding interest If % is paid on bank deposits. The dynamic production debt My is all repaid in full to the

bank at the end of each cycle. The funding interest If % paid by a bank is a bank liability, not an asset.

The deposits belong to deposit holders. The bank must transfer to them the

deposit interest it receives when the production debt My is repaid. At first sight the bank would be losing

money because it would be left in debt by the same amount as the deposit

interest.

In practice, the production

system does not “pulse” as shown for simplicity in Figure 2. Instead, there is an ongoing dynamic flow of

production and consumption funded by the dynamic production debt My. The pool of residual debt (My in this paper) shown at the

lower centre of Figure 2 is the accumulated interest component My*If % /(Vy*100) created through

each nominal business cycle. 80 Since the price P itself is the

sum of the price increases shown at the bottom right of Figure 2, price P must

represent the total price inflation.

Assuming production

Q is constant, the deposit interest If % (less tax) can be paid to depositors only if prices

P increase as shown. Otherwise the

production debt My cannot be cleared

when the economic production Pq 81 is sold. In this paper, the inflation caused by the deposit interest on

the dynamic production debt My is called systemic inflation.

In an economy based on

interest bearing debt, almost all price is inflation.

80. My is a dynamic variable similar

to those used in almost iterative computer programme. The new total becomes the

old total for that variable plus the increment added to it each cycle.

81. The quantity of production q is what is produced in the single

nominal production cycle shown in Figure 4. The amount q must be multiplied by

the speed of circulation Vy to get total

output Q.

Click

here to view FIGURE 3 :THE VISUAL

CHALLENGE CPI (CONSUMER PRICE INDEX)

ENGLAND 1300-2000.

Figure 3 gives a historical

overview of inflation in

By the beginning of

the 20th century prices had increased by just 6 times in 600 years,

with nearly all the increases due to the “great debasement” of the mid-Tudor

period and the Napoleonic wars around the turn of the 19th century.

Prices fell by about one third between 1800 and 1900 during the industrial

revolution due to vast improvements in productivity. Higher productivity means more goods and

services are produced for the same input costs leading to lower prices P if

money M and speed of circulation V remain constant.

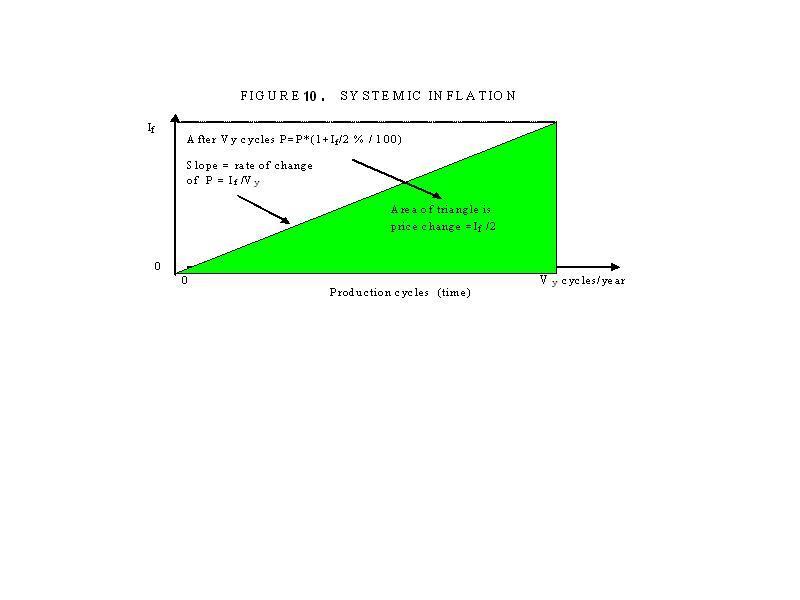

![]()

![]() The price change

formula P=P*(1+ If % /(Vy *100)) shown at the bottom right of Figure 2 refers to a single production

cycle producing the (constant) economic output q. Figure 10 shows that,

assuming the deposit interest rate If and output Q are

more or less constant, physical inflation is half of If %. The figure P* If % /(Vy *100) is the rate of change of P. It must be

mathematically integrated to give the total numerical change in P. This

increase in price in called systemic inflation.

The price change

formula P=P*(1+ If % /(Vy *100)) shown at the bottom right of Figure 2 refers to a single production

cycle producing the (constant) economic output q. Figure 10 shows that,

assuming the deposit interest rate If and output Q are

more or less constant, physical inflation is half of If %. The figure P* If % /(Vy *100) is the rate of change of P. It must be

mathematically integrated to give the total numerical change in P. This

increase in price in called systemic inflation.

Click here to view FIGURE 10 : SYSTEMIC INFLATION.

{kind=link}

Systemic inflation is

a structural part of the debt-based financial system whenever interest is paid

on deposits.

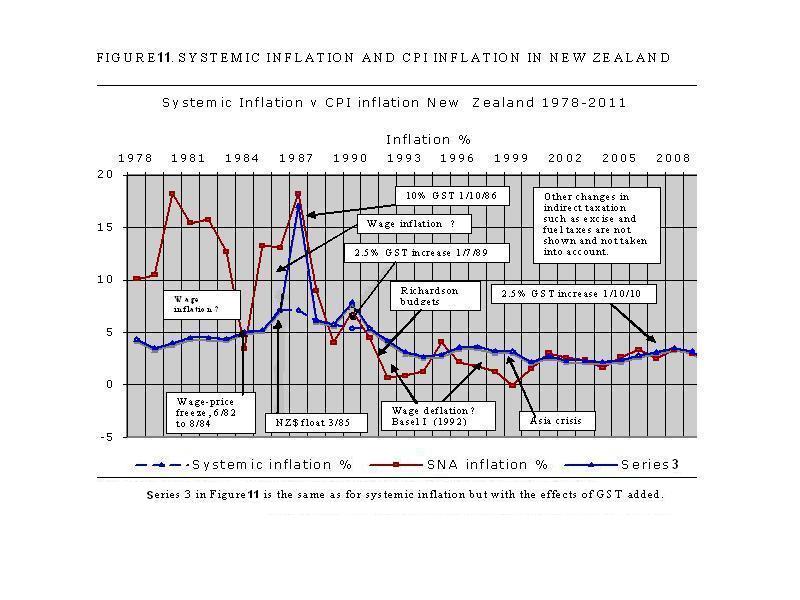

Figure 11 compares

systemic inflation with consumer price inflation (CPI) in

Click here to view FIGURE 11. SYSTEMIC INFLATION

AND CPI INFLATION IN NEW ZEALAND.

{kind=link}

Rapid wage

increases increase the debt for production My faster than would normally be