NGO Another Way (Stichting Bakens Verzet), 1018

AM

SELF-FINANCING, ECOLOGICAL,

SUSTAINABLE, LOCAL INTEGRATED DEVELOPMENT PROJECTS FOR THE WORLD’S POOR.

|

FREE E-COURSE FOR DIPLOMA IN INTEGRATED DEVELOPMENT |

|||||

Edition 01 : 13 September,

2012.

Edition 05 : 30 January, 2012.

(VERSION EN FRANÇAIS PAS DISPONIBLE)

Summaries of monetary reform

papers by L.F. Manning published at http://www.integrateddevelopment.org

The

referenced papers :

NEW Comments on the IMF (Benes and Kumhof) paper “The

Chicago Plan Revisited”.

DNA of the debt-based economy.

General summary of all papers published.(Revised edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

The Manning plan for permanent debt reduction in the national economy.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

THE MANNING PLAN

FOR PERMANENT DEBT REDUCTION IN THE NATIONAL ECONOMY

By

19B

T

+64 4 2986890

24 January, 2014. Final version 10

for publication.

All Rights

Reserved.

THE MANNING PLAN

FOR PERMANENT DEBT REDUCTION IN THE NATIONAL ECONOMY

EXECUTIVE SUMMARY FOR INTERNATIONAL APPLICATION.

Introduction.

A low risk

politically acceptable and practical way to resolve the world debt crisis

without sudden or radical change to the world’s financial system is presented.

It is worked out for conditions in

Three administrative

institutions are introduced:

A national debt management

authority (NDMA),

A national public development

fund (NPDF)

A national public investment

trust account (NPITA).

The plan is based on specific

forms of UBI and DJI structured to avoid inflation. Parameters can easily be

adjusted so that incomes match the physical and human resources available to

the economy. The plan provides for control of secondary on-lending to

avoid any risk of inflation exceeding

1.3%.

Debt

jubilee.

All legal residents

receive a weekly basic income payment of about

€ 63 ( US$ 84). This goes into a special personal UBI account. For

businesses a weekly payment of € 63 (US$ 84) goes into a DJI account for each

Full Time Equivalent (FTE) employee registered under a PAYE (Pay as You Earn)

or equivalent tax system.

Parameters suitable

for each country will vary. As a very

rough guide, the total annual

amounts involved could be to the order of

€ 5 billion (US$ 6.65 billion) for each million people, of which about €

3.75 billion ( US$ 5 billion) for

Universal Basic Income (UBI) and € 1.25 billion (US$ 1.65 billion) for Business

Debt Jubilee Income (DJI). The money to make the payments will be created

debt-free and interest-free by a publicly-owned Central (or Reserve) Bank and

administered by the NDMA

The payments made to

indebted persons and businesses will be used to retire their bank debt. The

payments made to non-indebted persons and businesses will be invested in a

National Public Development Fund (NPDF) that will pay tax-free interest on the

deposits at around 2.3%/year, a figure comparable to the existing average

deposit interest rate after taking reduced inflation and taxation into account.

The NDPF money will be used to fund new productive development both public and

private. NPDF acts as a publicly owned Savings and Loan institution for the

purposes of new productive investment.

In

Public debt.

Existing government debt will be replaced as it matures by debt-free

interest-free credit created by the Central Bank for the NDMA. This does not

increase banking system deposits so the process cannot be inflationary. Money

to fund new government investment will initially be sourced from the NPDF using

deposits from non-debtor UBI and DJI accounts.

National

public investment trust account (NPITA).

Bank deposit

holders will be able to invest in a National Public Investment Trust Account

(NPITA) that will act as a publicly-owned Savings and Loan institution to

manage the on-lending of deposits to fund the exchange of existing assets and

to provide personal loans (including student loans and credit cards).

Bank

balance sheets.

Under the plan,

bank balance sheets will still grow, but over time there will be little bank

debt remaining. Instead, secondary lending will be 100% backed by monetary

deposits. Banks will be paid a spread of around 1.7%/year for their services,

comparable to what they get now after taking into account that their lending

under the new system is practically risk free as normal debt repayment is

guaranteed through the Universal Basic Income (UBI) and Debt Jubilee Income

(DJI) accounts.

Interest on NDPF and NPITA investments.

New money for

interest paid on UBI/DJI balances invested with NPDF and to depositors

on-lending their deposits through NPITA will be supplied debt-free and

interest-free by the central bank.

EXECUTIVE SUMMARY FOR

1. This plan offers

a very low risk way to resolve the world debt crisis without sudden or radical

change to the world financial system. It brings together a number of ideas such

as Universal Basic Income (UBI), Debt Jubilee Income (DJI), and Quantitative

Easing (Monetary Dialysis) that are already receiving some attention but cause

concern to some policy makers when they are considered in isolation. The plan

can be implemented quickly and unilaterally.

2. The plan is

based on specific forms of UBI and DJI structured to avoid inflation. The plan

avoids most inflation because it can easily be adjusted so that incomes match

the physical and human resources available to the economy.

3. The Manning Plan

sets out implementation details for

4. The total

Universal Basic Income payments are initially about NZ $23 billion/year and the

total Debt Jubilee Income payments are initially about NZ$7 billion/year. The

money to make the payments will be created debt-free and interest-free by the

Reserve Bank and administered by a New Zealand Debt Management Authority

(NZDMA).

5. The payments

made to indebted persons and businesses will be used to retire their bank

debt. The payments made to non-indebted

persons and businesses will be invested in a New Zealand Public Development

Fund (NZPDF) that will pay tax-free interest on the deposits at around

2.3%/year, a figure comparable to the existing

average deposit interest rate after taking into account reduced

inflation and taxation. The NZDPF money will be used to fund new productive

development both public and private. NZPDF acts as a publicly owned Savings and

Loan institution for the purposes of new productive investment.

6. About NZ$ 15

billion of bank debt will be retired during the first year, leaving new

deposits of about NZ$15 billion, roughly similar to the present financial

system.

7. Bank deposit

holders will be able to invest in a Public Investment Trust Account (PITA) that

will act as a publicly-owned Savings and Loan institution to manage the

on-lending of deposits to fund the exchange of existing assets and to provide

personal loans (including student loans and credit cards).

8. Bank balance

sheets will still grow, but there will be little bank debt. Instead, secondary

lending will be 100% backed by monetary deposits. Banks will be paid a spread

of around 1.7%/year for their services, comparable to what they get now after

taking into account that their lending becomes largely risk free. Normal debt

repayment is guaranteed through the Universal Basic Income and Debt Jubilee

Income accounts.

THE MANNING PLAN FOR DEBT REDUCTION

1. Establish a private Universal Basic

Income (UBI) Account for every legal resident. The UBI is described in

paragraph 2. The UBI provision will apply only to individual people. The

account will record the outstanding household and consumer debt of each

individual. Jointly held debt will be shared among those adults in the household

who are jointly and severally liable for that debt. Individual debt, such as student and credit

card debt will be assigned to the individual who holds it. The debt accounts

will be dynamic: new debt incurred and debt repayments made will be automatically

registered on the private Universal Basic Income account.

2. Pay every legal resident a weekly

debt-free, interest-free Universal Basic Income funded from the central bank. The

amount of the UBI will be variable so that it matches the ability of the

economy to absorb the debt-free, interest-free cash injection. The UBI will be

managed by a New Zealand Debt Management Authority (NZDMA) set up for the

purpose of administering the Manning Plan [1]. A Universal Basic Income of

NZ$100/week will amount to about NZ$23 billion/year.

3. The UBI will be funded by

means of debt-free, interest-free credit created by the central bank and

deposited in the UBI accounts managed by the NZDMA. The credit could be called

sovereign or treasury credit created by the central bank on behalf of the

government, and it mirrors the way government funding is created at present

except that it will be done internally without the need to issue interest-bearing bonds to private banks and

financial institutions.

4. The UBI will be used to automatically

and directly reduce the debt of individuals carrying debt. Existing household

bank debt will progressively be set off against the UBI cash injection

(paragraph 2) used to repay it. About 36% of the NZ$23 billion annual UBI

payments (paragraph 2) or more than NZ$ 8 billion will be used to extinguish

bank debt until nearly all bank debt has been repaid [2]. NZ$ 14.7 billion of the new debt-free,

interest-free, UBI payments will be paid out to non-debtors compared with an

average of NZ$16.4 billion of new bank debt issued annually in New Zealand

during the period from the end of March 2002 to the end of March 2012 [2].

Deposit growth under the Manning Plan will therefore be less than it has been in

the past while existing household bank debt will fall quickly as it is repaid.

5. All Universal Basic Income payments made

to those people (initially about 64% of the population in New Zealand,

including children) who are not in debt [2] will be loaned by the New Zealand

Debt Management Authority on their behalf to a New Zealand Public Development

Fund (NZPDF) to be established by the NZDMA at an interest rate to be set by

the NZDMA from time to time. The interest rate will reflect inflation of, say,

1.3 % plus a margin of, say, 1% to reflect the average interest rate on all

deposits. The interest payments payable by the NZPDF on the on-loaned UBI

deposits would be tax-free. On the above figures, the net real interest rate

payable by the NZPDF would be about 2.3% compared with the comparable average

existing net real deposit interest rate in New Zealand of about 2.4% [3].

The NZPDF does not

have to on-lend all of the deposits it receives from the UBI accounts. The

NZPDF could keep some of the residual NZ$14.7 billion (paragraph 2) to enable

the government to reduce taxation or repay government debt, or it could decide

to hold substantial balances in its accounts should that be required for system

stability. The direct cost of any of the three options is the interest that the

NZPDF pays into the citizens’ individual UBI accounts on those amounts it does

not lend for productive investment.

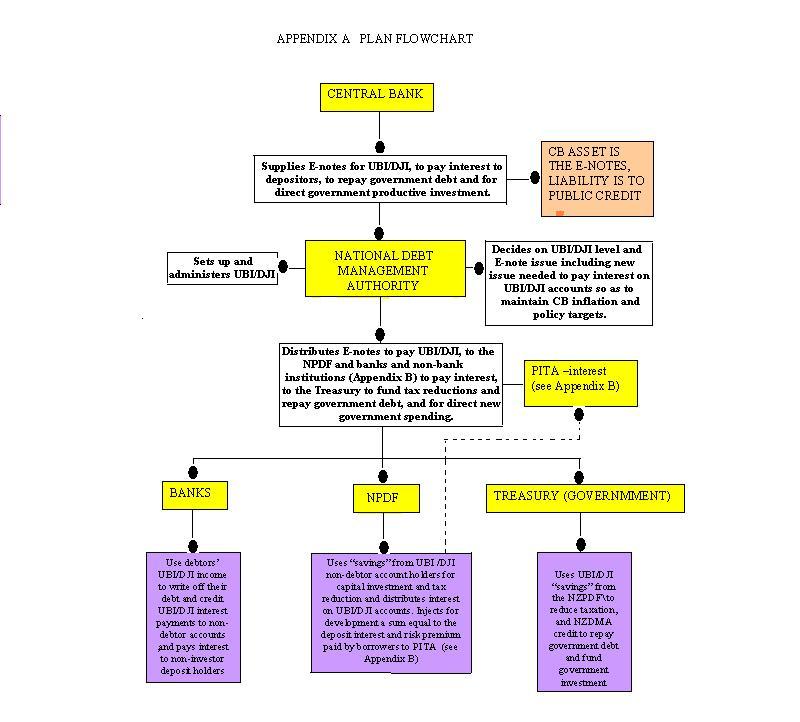

A basic flow

diagram for the Manning Plan is provided as APPENDIX A.

{kind=link}

6. Establish a Debt Jubilee Income (DJI)

account with the NZDMA for every

The DJI is described

in Paragraph 7. The account will record the outstanding debt of each individual

business. The debt accounts will be dynamic: new debt incurred and debt

repayments made will be automatically registered on the Debt Jubilee Income

account.

7. Pay every qualifying company a monthly

debt-free, interest-free Debt Jubilee

Income (DJI) funded from the central bank. The amount of the DJI will be

variable so that it matches the ability of the economy to absorb the debt-free,

interest-free cash injection. The New Zealand Debt Management Authority (NZDMA)

will manage the DJI. A Debt Jubilee Income of NZ$100/paid Full Time Equivalent

(FTE) employee/38.45 hour week will amount to about NZ$7 billion/year [5].

8. The DJI will be funded by

means of debt-free, interest-free credit created by the central bank and

deposited in the DJI accounts managed by the NZDMA. It could be called

sovereign or treasury credit created by the

central bank on behalf of the government, and it mirrors the way government

funding is created at present except that it will be done internally without the need to issue

interest-bearing bonds to private banks and financial institutions.

9. The banks will use the DJI (paragraph 8)

distributed through NZMDA to automatically and directly reduce the

(non-transaction account) bank debts of businesses carrying

non-transaction account bank debt. Existing business bank debt other than

transaction account debt will be set off against the DJI cash injection used to

repay it. Since most businesses carry some bank debt, most of the NZ$7 billion

annual DJI payments [5] will be used to extinguish bank debt. Net business

deposit growth from new investment supplied from the NZPDF will therefore

initially be similar to what it has been in the past while business bank

debt will fall quickly as it is repaid from the businesses’ DJI accounts.

10. Debt Jubilee Income payments made to DJI

account holders that are not in debt will be loaned to the NZPDF at an interest

rate to be set by the NZDMA from time to time. The interest rate will reflect

inflation of, say, 1.3 % plus a margin of, say, 1% to reflect the average

interest rate on all deposits. The interest payments on the DJI deposits loaned

to NZPDA would be tax-free and paid from new central bank money created

debt-free and interest free. The interest funding will be supplied to NZDMA by

the central bank and passed to NZPDF for distribution. On the above figures,

the net real interest rate would be about 2.3% compared with the comparable

average existing net real deposit interest rate in New Zealand of about 2.4%

[3].

The NZPDF does not

have to on-lend all of the deposits it receives from the DJI accounts. The

NZPDF could keep some of the residual it receives to enable the government to

reduce taxation or repay government debt, or it could decide to hold

substantial balances in its accounts should that be required for system

stability. The direct cost of any of the three options is the interest that the

NZPDF pays into the businesses’ individual DJI accounts on those amounts it

does not lend for productive investment.

The basic flow

diagram for DJI is shown in APPENDIX A.

11. In

12. A unit in the Audit Office will monitor the

Debt Jubilee Income working alongside the Department of Inland Revenue [6].

13. Existing government debt

will be replaced as it matures by debt-free interest-free credit created by the

Central Bank for the NZDMA. New money to fund government and local government

investment will be sourced (at least initially) from the New Zealand Public

Development Fund (NZPDF) that receives deposits from the non-debtor UBI and DJI

accounts.

Once most existing bank debt has been repaid and the need to sterilise

the Universal Basic Income and Debt Jubilee Income payments made to non-debtors

is reduced, the Central Bank may begin

issuing some debt-free-interest-free credit directly to the NZDMA for public

development instead of using investment

funding from the Universal Basic Income and Debt Jubilee Income accounts.

Replacing maturing government debt with Central Bank credit paid through NZDMA

does not increase banking system deposits so the process cannot be

inflationary. On the other hand, new public debt-free interest-free money

issued by the central bank through the NZDMA and passed directly to the

treasury for productive development

would increase deposits in the banking system as it is spent into circulation

and could therefore be slightly inflationary.

14. The

NZDMA will manage the Universal Basic Income level (paragraph 2) and the

business Debt Jubilee level (paragraph 7) to ensure the issue of new credit

matches the needs of the economy as a whole so as to keep inflation at or below

about 1.3%. The new credit injection includes a sum equal to the deposit and

risk premium interest paid by borrowers to PITA as set out in paragraph 24.

NZPDF will invest the new credit injection in new productive development as

shown in Appendices A and B.

15. The Manning Plan could be

designed for zero deposit interest and zero inflation, but many individuals and

institutions presently depend on unearned income (deposit interest). The Plan is designed to

accommodate a real interest rate at about the same level as in the present

financial system to avoid overly distorting existing net real average deposit

incomes, especially for the elderly and for pension funds. It will also prevent

existing deposits leaking into consumption where they would create demand-pull

inflation in the productive economy, a problem inherent in the large existing

deposit base that other public credit proposals have failed to take into

account.

16. The deposits on-loaned by those receiving

a Universal Basic Income (paragraph 2) or Debt Jubilee Income (paragraph 7)

represent secondary debt the treasury borrows from the public

through the NZPDF (paragraph 5) to fund the creation of new productive assets,

both public and private, (and which could also include government investments

in education and health care, especially primary health care). The UBI/DJI

accounts held by residents and businesses will separately record the interest

balance. The interest paid by the NZPDF to non-debtor adult UBI account holders

(those aged 18 years and older) and non-debtor DJI businesses will be available

to them on demand. Adult account holders and businesses will be issued a NZPDF

debit card so they can draw down their available interest balance and check

their debt or investment balances. The interest balances of those UBI account

holders under 18 years of age would accrue to provide them with a fund for

personal use (such as education or a home deposit) once they turn 18.

17. As soon as the Manning Plan becomes

operative the banks would immediately cease to create new private

interest-bearing debt and its corresponding deposits for the purpose of funding

the purchase of new or existing capital assets, though they will continue to

fund day to day productive transaction accounts. The New Zealand Debt

Management Authority will regulate the interest rates charged on transaction

account debt when required, and set supplementary capital reserve requirements

to ensure there is a full 100% reserve backing for all financial system

deposits once bank debt (excluding that supporting the productive transaction

accounts) has been repaid. The 100% reserve backing will also extend to the

productive transaction accounts that, in

18. The debt repayments made through the

UBI/DJI accounts will be in addition to the normal contractual debt repayments

made by individual and business debtors to private commercial banks under their

existing loan agreements with their customers. The enabling legislation will

ensure that normal banking practice is continued until all existing bank debt

except that supporting productive transaction accounts has been fully repaid

but with:

(a) the repayment periods adjusted to take

account of the accelerated principal repayments made from the Universal Basic

Income and Debt Jubilee Income accounts and

(b) the interest rates on the debt adjusted

downward as set out in paragraph 19.

19. The NZPDF may license private commercial

banks to act as intermediaries in the production and exchange of new capital

assets. The NZPDF will lend to the licensed banks at the same interest rate it

pays on what it borrows from the Universal Basic Income and Debt Jubilee Income

accounts held by individuals and businesses. That interest shall be included in

the bank-intermediated loan interest rates. The commercial banks’ interest rate

on intermediated lending will then be made up of:

(a) The NZDPF funding rate that the banks will

pay to NZPDF plus

(b) A bank spread up to a maximum (probably

less than 1.7%) set by NZDMA from time to time to reflect the zero risk of

lending in a system where repayment is guaranteed through the UBI and DJI

accounts. In practice this will provide

funding for the production and exchange of new capital assets at less than 4%

interest per annum.

20. The private commercial banks will be

required to follow strict investment guidelines set by the NZDMA and

administered by NZPDF. Rather than competing on the basis of cost the banks

will need to focus on better service to their customers.

21. Most existing banking system deposits have

been alienated from the original debt from which they were created. In

aggregate, borrowers hold the debt while non-borrowers hold the corresponding

deposits. The original household and business bank debt is progressively repaid

through the UBI/DJI accounts using new interest-free and debt-free money, (as

well as through orthodox debt repayment referred to in paragraph 18). The new

deposits accruing to non-debtors in the UBI/DJI accounts are invested with the

NZPDF. The existing bank generated individual and business debt remaining in

the banking system declines as it is repaid.

22. To avoid unrestrained increases in total deposit

interest (and hence inflation) that would result from increasing the speed of

circulation of the deposit base by multiple on-lending of deposits, the Manning

Plan will manage the increase in secondary debt arising from on-loaned banking

system deposits. Currently in

23. The NZ Debt Management Authority will

establish a Public Investment Trust Account (PITA) to manage the supply and

price of secondary debt and will supply debt-free and interest-free money to

fund the interest banks pay on deposits (b), (c), (d) and (e) set out in

paragraph 27 that are not on-loaned

to PITA by depositors. The deposit interest paid on bank deposits to non

investors will be set by the NZDMA at a level up to about 1.3%.and to PITA

investors will together produce systemic inflation that will be held at or

below about 1.3% as in paragraph 5.

24. The Public Investment Trust Account

(paragraph 23) will accept term investments from deposit holders and establish

several risk categories for deposit holders who seek a higher interest rate

than what is needed to cover inflation (below 1.3% per annum). Among the

highest risk categories will be special categories for unsecured personal

loans. The supplementary interest rate applying to each risk category will be

managed so as to adequately allocate secondary lending for the purposes of

exchanging existing capital assets and funding personal loans. No secondary debt funding will be made

available for commodity speculation or the purchase of derivatives. The deposit

interest including the risk premium paid by borrowers to investors through PITA

will be injected into the financial system by the NZDMA through the operations

of the NZPDF referred to in paragraph 14.

25. PITA may license private banks and

non-bank institutions to act as intermediaries in the exchange of capital

assets and to provide personal loans. It will lend the deposits invested with

it by individuals and businesses to the licensed banks and non-bank

institutions at the same interest rate paid by NZDMA on bankings system

deposits that are not invested with

PITA (paragraph 14) plus the

interest rate surcharge applicable to the PITA risk category. That interest

shall be included in the intermediated loan interest rates and paid to PITA by

the borrowers or to intermediating banks and non-bank institutions as the case

may be. The banks’ and non-bank institutions’ interest rate on intermediated

lending will then be made up of:

(a) The PITA funding rate passed to PITA

investors (those bank deposit holders who have chosen to invest with PITA) plus

(b) A bank spread up to a maximum (probably

less than 1.7%) set by NZDMA from time to time to reflect the low risk of

lending in a system where non-business repayments are guaranteed through the

Basic Income accounts.

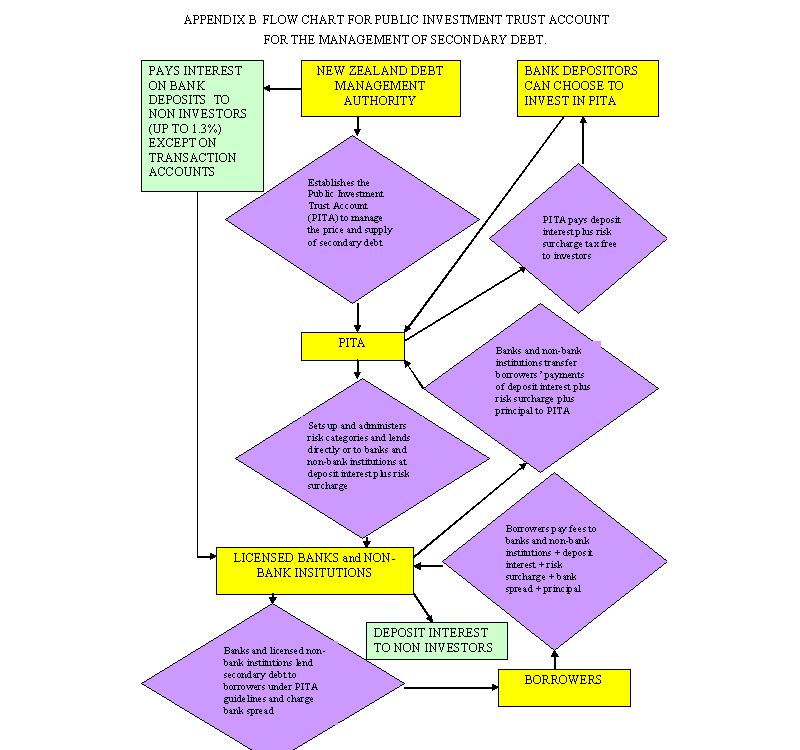

A flow chart for PITA is shown

in APPENDIX B.

{kind=link}

The licensed banks

and non-bank institutions will regularly report on their allocation of loan

funding sourced from PITA according to the different risk categories, ensuring

that both the total secondary debt and the distribution of that secondary debt

among the different risk categories are known at all times.

For purposes of

illustration only, the risk margin on secured residential assets might be 1%

bringing New Zealand home loan rates down to about 4%/year (1.3% inflation +

1.7% bank spread + 1% risk margin), while the risk margin on secured business

assets might be 2%, bringing interest for them down to about 5%/annum. The risk categories for partially secured or

unsecured loans would be considerably higher. The weighted average interest

paid on all deposits would be set to about 2.3% as in paragraph 5.

26. The licensed banks and non-bank lending

institutions on the one hand and PITA investors (those bank deposit holders who

have chosen to invest with PITA) on the other hand will equally bear the cost

of defaults on loans originating with licensed banks and non-bank lending

institutions [7]. Since any bank and non-bank institution losses are likely to

be funded from the applicable bank spread the banks and non-bank institutions

are likely to adopt a cautionary approach to risky lending. The PITA investors’

share of loan default losses will be periodically calculated for each risk

category and deducted by PITA from the funding rate PITA investors are paid

under paragraph 25(a).

27. At any time under the Manning Plan the

banking system deposits are made up of:

(a) The new debt-free money invested by

UBI/DJI non-debtor account holders in NZPDF in so far as that money has been

on-loaned by the NZPDF either directly or through licensed banks for productive

capital investment (paragraph 5), initially about NZ$14.7 billion/year (paragraph 4).

(b) New deposits arising from new direct

government spending that is not funded from the Universal Basic Income or Debt

Jubilee Income accounts. This would probably be quite small to begin with but

could eventually total several NZ$ billion/year. The new debt-free

interest-free money backing the deposits would be issued by the central bank

through the NZDMA to the treasury at the request of the government.

(c) Existing household and business

non-transaction account deposits held by debtors outside of the UBI/DJI

accounts. [8].

(d) Existing household and business

non-transaction account deposits held by non-debtors outside of the UBI/DJI

accounts. [8].

(e) Deposits arising from the payment of

interest on bank deposits by NZPDF, by NZDMA to banks on deposits not invested with PITA and the sum

equal to the deposit interest including the risk premium paid by borrowers to

investors through PITA (paragraph 24).

(f) Transaction account deposits.

The average annual increase

in deposits in

28. Government, business, individual residents

and banks would all benefit from the Manning Plan. The government would benefit

because it would have an ongoing domestic non-bank, non debt-based development

fund available at low cost for public investment, and the ability to easily

raise or retire government debt. The main benefits for business are the on-going

debt jubilee, cheaper loans and the absence of boom-bust business cycles.

Business would also benefit from the increased demand for public infrastructure

work, from new consumption generated through any tax reduction and through the

expenditure of interest received on the UBI/DJI accounts. Existing individual

debtors would benefit from rapid reduction in their debt, and those who are not

debtors would benefit from increased spending power as well as from cheaper

loans and a stable, growing economy [9]. Young people will benefit from having

a “savings” fund available to them when they turn, say, 18 years of age. Banks

will benefit from very low default rates, and a steady, almost risk-free

increase in income from their balance sheet expansion.

29. The Universal Basic Income paid to

individual debtors and the Debt Jubilee Income paid to indebted businesses will

decrease deposits (bank liabilities) and

loans (bank assets) by the same amount so that the banks’ net worth will not be

affected. The on-lending by NZDPA for new capital assets and PITA for existing

capital assets and personal loans will also create equal increases in the

banks’ assets and liabilities so they will not affect the banks’ net worth

either. The banks’ assets will also increase by the e-note cash they receive

from the new money injected through the NZDMA into the banking system for

direct investment and interest payments, and their customer deposit liabilities

will again increase by the same amount. Overall, the banks’ balance sheets will

continue to expand, even through the initial period of debt repayment, though

possibly at a slower overall rate than at present. The main change in banking

practice will be that all deposits will eventually be 100% backed by money

(including the productive transaction accounts backed by bank capital) and

there will be no interest-bearing bank debt in the financial system

except that supporting the productive transaction accounts.

30. The NZDMA accounts will be held

in trust for all legal residents. Its balance sheet would grow quickly but it

will not normally hold large monetary balances. A large portion (about 36%) of

the debt-free interest-free e-notes it issues to individuals’ UBI accounts

during the initial period and most of the debt-free interest-free e-notes it

issues to businesses’ DJI accounts during the initial period will be promptly

cancelled through compulsory residents’ and businesses’ debt repayments. All

remaining debt-free interest-free credit except interest payments deposited in

the UBI and DJI accounts or paid as deposit interest to licensed commercial

banks and non-bank institutions will be initially be represented by loans from

the UBI and DJI account holders to NZPDF. The proportion of new credit invested

with NZDPF will increase as existing bank debt is retired. A substantial

proportion of other (that is, existing) deposits will be invested with PITA.

The PITA assets will be the (secondary debt) loans it (or licensed banks and

non-bank institutions acting on PITA’s behalf) makes to those needing funding

to exchange existing assets and for personal loans. The PITA liabilities will

be the deposits it has borrowed from those deposit holders who choose to lend

to it as shown in Appendix B. The banking

system deposits available for on lending by deposit holders to PITA will

increase at about the average deposit rate (about 2.3%/year in the illustrative

example for

31. The Manning Plan remains fully flexible at all times. Its primary elements, namely the Universal

Basic Income rate, the Debt Jubilee Income rate, the interest rates paid on

NZPDF and PITA investments, the level and nature of NZPDF and PITA investments,

and any tax reductions, can all be varied easily. Since the Manning Plan is entirely domestic,

it cannot be directly affected by current account considerations, although it

would best be implemented together with the Foreign Transactions Surcharge

proposed in the working paper attached below as APPENDIX C.

CONCLUSION.

Individuals and

businesses will quickly see the benefits of the Manning Plan but there will be

few visible changes in banking services.

Individuals and businesses will still have debts and deposits. Debtors

will still pay interest on and repay their debt. Deposit holders will still receive interest

on their deposits (other than productive transaction accounts) except there

will be no tax deducted from that interest[10]. The main changes will be in the

pathways

for investing deposits and applying for loans insofar as investing and lending

will be managed on a Savings and Loan basis by two public institutions. The New Zealand Public Development Fund

(NZPDF) will manage lending for new productive investments while the Public

Investment Trust Account (PITA) will manage the on-lending of existing deposits

for the exchange of existing assets and for making personal loans. Since NZPDF

is likely to license commercial banks as intermediaries and PITA is likely to

license both commercial banks and non-bank institutions as intermediaries, the

administration of loans may not appear very different to bank customers.

END NOTES.

[1]

[2] Statistics New Zealand data suggest that

about 82% of two-adult households in New Zealand and more than 50% of one-adult

households are in debt. Single person and single parent households make up

about 50% of all households, and there are about 1.4 million households in

[3] As of July 2012 the banks’ average

“funding” rate (the average interest the banks pay on deposits) was 3.67%

(according to Reserve Bank of New Zealand data series C10 – the average

interest rate on loans was 5.79% and the bank spread or gross margin was

5.79-3.67 or 2.12%). Allowing for an

average tax rate on interest of 20%, the present tax-paid return to depositors

is about 2.9%. Systemic inflation in

[4] According to Reserve Bank of New Zealand

statistics Table C3 Monetary Aggregates (historical) the monetary base

(M3-repos) increased from NZ$127.1 billion in July 2002 to NZ$ 244.7 billion in

July 2012, giving an average increase of about NZ$11.8 billion/year over the

past decade. Since the

[5] The relevant data for

[6] The mandatory penalty for fraudulent reporting

of employees and/or worked hours might be the permanent exclusion of that

business from the business Debt Jubilee as well the permanent exclusion of any

other businesses subsequently established or purchased by any of that company’s

directors. However, the likelihood of

abuse is modest because, in the majority of cases, the income tax rates applied

to incomes in

[7] Similarly, if PITA lends directly to

individuals and businesses for non productive investment or partly secured or

unsecured personal loans, PITA will bear half of any default loss and the PITA

investor the other half. The difference between such direct PITA loans and

licensed bank and non-bank lending is that PITA may choose to include only some

or none of the lending spread in the interest rates it charges. In practice it

is likely PITA would restrict any direct lending to low risk investments.

[8] Not all of the deposits used to fund items

that make up a current account deficit are returned to the domestic economy. In

-NZ$55 billion.

That means NZ$55 billion of the deposits created by the

[9] The Manning Plan is designed to protect

pensioners and pension funds. Pensioners will receive much the same net return

on bank deposits as they do under the existing banking system. There will still

be an active investment sector that will enable pension funds to invest and grow.

[10] Informal lending among individuals,

families, and firms may also occur just as it does under the existing

debt-based financial system. Such lending represents unrecorded secondary debt,

but its volume would be minimal in the context of the total secondary debt. Any

interest paid on informal secondary debt is also unrecorded but small. Only

banks and non-bank institutions licensed by PITA will be legally permitted to

create secondary debt for the exchange of existing assets and for personal

loans. Likewise, only banks licensed by NZPDF will be legally permitted to

create secondary debt for the production and exchange of new productive assets.

Informal lending for profit would become an offence.

11/09/12

APPENDIX A : SYSTEM FLOWCHART.

APPENDIX B : FLOW CHART FOR PUBLIC

INVESTMENT TRUST ACCOUNT FOR THE MANAGEMENT OF SECONDARY DEBT.

APPENDIX C : USING

A FOREIGN TRANSACTIONS SURCHARGE (FTS) TO MANAGE THE EXCHANGE RATE.

THE REFERENCED PAPERS

The

referenced papers :

00. Summary of papers published.

01. Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

02. How to create stable financial systems in four

complementary steps.

03. How to introduce an e-money financed virtual minimum

wage system in New Zealand.

04. How to introduce a

guaranteed minimum income in New Zealand.

05. The interest-bearing debt system and its economic

impacts.

07. The DNA of the debt-based economy.

08. Manifesto of the debt-based economy.

09. Unified text of the manifesto of the debt-based

economy.

10. Using a foreign transactions surcharge (FTS) to manage

the exchange rate.

11. The Manning plan for permanent debt reduction in the national

economy.

Return to : Bakens Verzet

Homepage

"Money is not the

key that opens the gates of the market but the bolt that bars them."

Gesell, Silvio, The

Natural Economic Order, revised English edition, Peter Owen,

This work is licensed

under a Creative

Commons Attribution-Non-commercial Share-Alike 3.0 Licence.