NGO Another Way

(Stichting Bakens Verzet), 1018 AM

SELF-FINANCING,

ECOLOGICAL, SUSTAINABLE, LOCAL INTEGRATED DEVELOPMENT PROJECTS FOR THE WORLD’S

POOR

|

FREE

E-COURSE FOR DIPLOMA IN INTEGRATED DEVELOPMENT |

|||||

Edition 01: 17 November, 2010.

Edition 02 : 08 August, 2011.

Edition 03 : Revised edition 07 September,

2011.

Edition 05 : 09 February, 2013.

(VERSION EN FRANÇAIS PAS DISPONIBLE)

Summaries of monetary reform

papers by L.F. Manning published at http://www.integrateddevelopment.org

NEW Capital is debt.

NEW Comments on the IMF (Benes and Kumhof) paper “The

Chicago Plan Revisited”.

DNA of the debt-based economy.

General summary of all papers published.(Revised edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage system

in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts. (Revised

edition).

Manifesto of 95 principles of the debt-based economy.

The Manning plan for permanent debt reduction in the national economy.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

HOW TO

INTRODUCE AN E-MONEY FINANCED VIRTUAL MINIMUM WAGE SYSTEM IN

By

Sustento

Institute,

"The

government should create, issue and circulate all the currency and credit needed

to satisfy the spending power of the government and the buying power of

consumers..... The privilege of creating and issuing money is not only the

supreme prerogative of Government, but it is the Government's greatest creative

opportunity. …….The taxpayers will be saved immense sums of interest, discounts

and exchanges. The financing of all public enterprises, the maintenance of

stable government and ordered progress, and the conduct of the Treasury will

become matters of practical administration. …….. Money will cease to be the

master and become the servant of humanity."

[

“Financial

markets have worked hard to create a system that enforces their views: with

free and open capital markets, a small country can be flooded with funds one

moment, only to be charged high interest rates - or cut off completely - soon

thereafter. In such circumstances, small countries seemingly have no choice:

financial markets' diktat on austerity, lest they be punished by withdrawal of

financing”.

[Joseph E. Stiglitz “Taming Finance in an Age of Austerity” Published by Project

Syndicate, Monday July 12, 2010]

Key

Words: current account deficit, debt,

debt model, debt growth, deposit interest, domestic debt, domestic credit,

equity in society, exponential debt growth, Financial Transactions Surcharge,

Financial Transactions Tax, Fisher equation, foreign debt, FTS, FTT, inflation,

local currency systems, local economies, revised Fisher Equation, savings,

structural debt growth, systemic debt growth, systemic inflation, unearned

income.

ACKNOWLEDGEMENTS.

The

author gratefully acknowledges the support of Raf Manji and the Sustento

Institute for their encouragement and advice; and to Terry

Manning and the NGO Stichting Bakens Verzet (“Another Way”) whose editing and

constructive critique have been crucial as the paper has evolved over time.

CONTENTS:

01. EXECUTIVE

SUMMARY.

02.

THE ECONOMIC DILEMMA.

03. THE VIRTUAL MINIMUM WAGE

PLAN A.

04. PLAN A DETAILS.

05. THE FOREIGN TRANSACTIONS

SURCHARGE.

06. CONCLUSION.

07. APPENDIX 1 :THEORETICAL

BACKGROUND.

08. APPENDIX 2: THEORETICAL

SUPPORT FOR THE PROPOSAL.

09.

BIBLIOGRAPHY.

01 EXECUTIVE SUMMARY.

The main dilemma faced by today’s economic policy makers is that the

price-based financial system they have been using has run out of room to

manoeuvre. It is no longer possible either to substantially increase interest

rates to combat inflation or to reduce them to stimulate “economic growth”.

This paper offers a

practical plan to resolve the world’s problem of exponential debt growth and to

control inflation. The plan is based on a revision of the

well-known Fisher Equation of exchange enabling it to take account of

interest-bearing debt. It is designed to ensure that no substantial income

group in the community is worse off than it is now.

The plan focuses on

a substantial virtual increase in the minimum wage to stimulate demand among

low-income earners and enable them to repay credit card and other high-interest

consumer debt. The plan does not

directly increase the minimum wage.

The virtual wage

increase is merely a delivery mechanism to distribute low-income support by the

injection of E-notes or electronic currency into the banking system. The

electronic currency will be created debt-free by the Central Bank. Firms will

be granted a percentage of that low-income support for their participation in

the plan and to provide them with additional capital for future investment. In

this paper a figure of 20% has been used arbitrarily for the capital grant made

available this way to firms.

The virtual

increase in the minimum wage will continue step by step indefinitely. The

additional consumer demand created by the virtual minimum wage

increases will encourage economic growth in the usual way until full employment

has been reached. Once full employment has been reached

the economic stimulus might have to be slowed to avoid demand-pull inflation

unless it is sterilised through savings programs, such as, in

The modest

debt-free injection of purchasing power using E-notes will increase the demand

for labour, providing strong economic growth. The labour supply will be

provided from existing spare economic capacity. Prices should not change

because increases in production costs tend to be avoided. The plan is expansive

because firms can increase their production in the normal way subject to human

and physical resource limitations and consumption demand.

A

supplementary reserve ratio will need to be introduced to the banking system

over and above the existing Basel III risk-based capital adequacy requirements.

It will need to be large enough to sterilise the new e-note deposits in the

banking system, and also to support progressive lowering of the OCR (Official

Cash Rate). The banking system will

apply quantity controls on debt and money instead of using price controls through

interest rates as it does now. As the

OCR is reduced towards zero percent, the existing systemic inflation in the

economy caused by the payment of unearned income in the form of interest on bank deposits will in turn

drop towards zero.

Since

the plan is, or can be made, practically inflation free it will not measurably

increase the cost of exports. The plan

does, however, propose to introduce a variable Foreign Transfer Surcharge or

FTS starting at 10%. This would allow the

On the

basis of the preliminary debt model calculations for

Until

now, prices P in the revised Fisher equation (Manning, 2009) have been maintained

at the expense of output Q, as firms have sought to maintain or improve profits

by cost cutting and shedding labour. Some firms may soon have to begin reducing

prices P to maintain output Q at functional levels and still clear their market

02.

The

plan offers a practical and stable route toward on-going debt reduction with a

very low level of inflation in the economy.

The stabilisation and ongoing reduction in the nation’s total debt is a

fundamental objective of the plan. The improved equity and better living

standards from higher incomes are an integral part of the economic

transformation the plan will produce.

01 Foreign ownership Dca in the

model referred to and GDP have been tracking together in

02 The change in the speed of circulation Vy of the

circulating transaction deposits My in the revised Fisher equation referred to

is primarily structural. Vy tends to decline as the structures of the

payments systems changes. Except for secondary effects related to changes in

interest rates, circulating transaction deposits My must expand in the debt system if the

economy is to grow.

02. THE

ECONOMIC DILEMMA.

The body of work supporting this paper confirms

that a revised Fisher Equation of Exchange 03 and the Fisher Theory

of Interest (Fisher 1930) are sufficient

to explain why debt is expanding exponentially throughout the world and why

orthodox economics has failed to prevent unsustainable debt growth resulting in

boom and bust economic cycles interspersed with downturns and recessions. The

main difference between the revised Fisher Equation presented, which

incorporates the impact of interest-bearing bank debt, and orthodox economics

is that while the revised Fisher Equation is based on managing the quantity of

debt, orthodox economics is focused on the price of debt.

Both approaches eventually require the quantity

of debt to be regulated. The revised Fisher Equation shows that when the price

of debt, expressed as the average interest rate paid on bank deposits, is used

as a regulator, an exponentially growing pool of unearned income is created.

That pool of unearned income has to be funded by inflation in the productive

sector because unearned income, by definition, produces nothing itself. As long

as that pool of unearned income was relatively small compared with economic

output expressed as Gross Domestic Product GDP the interest cost could be

funded from increased productivity and economic growth. The result was an ongoing shift in wealth

from the productive sector to the investment sector, but as long as that shift was

corrected through socially acceptable income redistribution, the system

remained relatively stable. 04 As the world economy has become ever

more reliant on interest-bearing debt instead of cash transactions the impact

of unearned income on debt levels has increased exponentially.

Exponential “growth” curves are inexorable. What started as a relatively small effect has

rapidly become unsustainable throughout the world. In

Since the deposit interest on the pool of

unearned income Ms is funded by inflation and all price in the

productive economy is also inflation, the transaction deposits My funding the productive economy must increase at

least in proportion to the debt funding the pool of unearned income Ms. If My is increasing more slowly than Ms the productive economy must be deflating provided the speed of

circulation Vy of My is more or less constant .

03 Detailed in Appendices 1 and 2.

04 In practice, in many Western Countries like

the

In

many countries the transaction deposits funding the productive economy grow a

little faster than the debt funding the pool of unearned income Ms because the former includes

new My deposits needed to fund endogenous growth. The relationship between the

productive deposits My and the pool of

unearned income Ms is a good indicator of a nation’s economic

health. That relationship can become distorted when excess “debt bubbles” build

up in the productive economy from time to time, producing the now familiar boom

and bust cycles.

Excess

bubble debt is produced by failure by the banking sector to properly align

demand for credit with the productive capacity of the economy. It arises in

In the

present debt-based financial system, the productive economy has to replace the

deposits it loses to the unearned income investment sector My. While the unearned income deposits migrate to

the investment sector, the corresponding debt backing Ms remains in the productive sector.

To replace the deposits lost as unearned income the productive economy must

borrow a new amount at least equal to what has been alienated from it as well

as enough to fund the next tranche of deposit interest 05.

During

booms there is excess debt in the productive system that affects both the rate

of increase of the pool of unearned income Ms and the bubble dent Db shown in the debt model. By and large, Ms has followed My so closely in the debt model arising from the

revised Fisher Equation because virtually all the nominal GDP growth in New

Zealand over the past 30 years has been funded by offshore borrowing as

demonstrated in “The Interest-Bearing Debt System and its Economic

Impacts” (Manning, 2010).

In

March 2011 the total domestic debt in

05 This simple concept lies at the core of the

world economic debate. Try it with counters. Start with 10 counters

representing unearned income deposits and 10 representing deposits in the

productive economy. The total debt is 20 counters. Suppose the unearned income

for the period starts at 1 counter. Shifting 1 from the productive economy to

unearned income leaves

06 The preliminary debt model calibration

shows the change in Ms exceeding the change in (My * 18) in each of the March years 2009, 2010, and 2011, indicating

a serious credit crunch, that can only be undone by increasing My by direct injection

(E-notes or electronic cash) into the productive sector. It is otherwise

numerically difficult to “grow” out of such a productive sector deficit because

of the high demand placed on the economy by debt servicing.

07 As in footnote 5 the amount added to My has to replace

the systemic inflation passed to the investment sector Ms plus add a

roughly equal amount to pay for the systemic inflation on the GDP.

08 It is difficult to achieve large

productivity increases in service based economies like those of

09 Further details are provided in Appendix 2 to this

paper.

From the March 2009 year through the March 2011

year there is little evidence of real expansion of

The dilemma faced by economic policy makers is

that the price-based financial system has run out of manoeuvring room. It is no

longer possible either to substantially increase interest rates to combat

inflation or for that matter to reduce them to stimulate “growth”. In

10 The OCR in New Zealand was 2.5% in August 2011. Its reduction to 1.5%, if fully reflected in

interest rates charged by banks to their clients, would increase growth by 1%.

03. THE VIRTUAL MINIMUM WAGE PLAN.

This

is an almost non-inflationary proposal to stimulate economic growth without the

need for radical change to the existing financial architecture. The key to the proposal is to increase

consumer purchasing power by increasing the circulating deposits (arising as an

increase in electronic cash ME in the debt model shown in the

Appendices) without significantly increasing prices and without causing any

growth in the pool of unearned income Ms.

a).

Increase the minimum wage to a VIRTUAL LEVEL of $20/hour, but leave

youth rates for those below 18 years of age at a lower level but above

$12.5/hour. The wage increase is virtual because the increase is paid through

employers but funded by a central bank cash injection into the economy.

Employers must pass the cash injection on to their employees. The higher

virtual wage is an instrument to deliver the cash injection of purchasing power

to those parts of the economy where it is most needed. The proposed increase

would potentially add about NZ$ 5 billion annually to disposable purchasing

power and 2.7% to GDP. The increase in GDP would be “real” growth stimulated by

greater purchasing power at more or less constant prices.

b). Supply new electronic cash (not debt) to businesses to fund the

virtual increase in the minimum wage, so there is no significant increase in price.

The new electronic cash deposits would circulate at the same speed as deposits

arising from debt. The first cash injection needed would be about NZ$ 5

billion/Vy =

5/18 or NZ$ 0,28 billion where Vy is the speed of circulation of the productive transaction

deposits My in the debt model. Since this amount helps cover

the deposit interest transferred to Ms , it must be repeated for very production cycle

leaving residual incomes available for

consumption and investment. It cannot be inflationary unless the total

aggregate amount exceeds the aggregate increase in Ms.

c).

Supply a corresponding injection to businesses to facilitate business growth,

to be paid to businesses weekly together with the planned virtual wage

increase. This supplementary support for businesses has been arbitrarily set at

20% of the virtual wage injection, that is 20% of NZ$ 5 billion, or NZ $ 1

billion/year.

d).

The planned increase in the virtual minimum wage income is largely expansive.

It does not increase systemic inflation because the E-note injection is not

interest-bearing debt. While it stimulates new productive activity by improving

business confidence the net injection will not be large enough to produce

significant demand-pull inflation. The circulating transaction deposits My in the debt model shown in the appendices does

not change because the new funds are injected in the form of electronic cash.

The proposed E-note injection will notionally support additional “real” GDP

growth of up to 2.6%. However, some of the deposits arising from the cash

injection will be used to reduce mortgage, credit card and other consumer

debt. As set out the plan details, E-note injection at about

the proposed level can be continued indefinitely.

e).

Use taxation revenue (about NZ$ 2 billion) from the up to 2.6% increase in

GDP to index social welfare and

superannuation payments to the higher VIRTUAL average wage. The virtual average wage will rise by $2/hour

to $25/ hour. This is based on June 09 NZIS income survey figures, which have

not changed significantly over the past year and represents a virtual wage

increase of about 8%. In

f). In

g).

Seek trade union agreement to keep real wage increases close to the inflation

rate 12. Such inflation-led

wage increases will apply to all workers in the usual manner, including those

receiving the virtual wage increase. Under the agreement the E-note injections

would be continued indefinitely as long as the rate of injection remains close

to or within the permanent growth capacity of the economy.

h).

Progressively extend the virtual wage increases. Many people will use some or

all of their extra income to reduce debt. The program could therefore be

continued until much, if not most, existing household debt is retired.

Increasing the virtual minimum wage from $20/hour to $23/hour will add another

$5 billion a year to lower incomes to enable the process to continue. Such

extensions should be possible because normal wage increases will progressively

reduce the size of the original injection as normal wages rise towards the

virtual minimum wage of NZ$ 20/hour. A third similar tranche, raising the

virtual minimum wage from $23/hour to $25/hour would follow the second, and so

on.

i).

The new cash deposits in the banking system could provide the base for

increases in bank lending. Supplementary reserve ratios will need to be

introduced into the banking system, over and above existing Basel III-based

capital adequacy criteria, so that bank lending can be managed by quantitative

means rather than by price. This will need to be done during the first year of

execution of the plan. The banking

system will progressively change the nature of its activities from credit

creation toward savings and loan intermediation.

j). To

reduce systemic inflation, progressively reduce the overnight cash rate (OCR)

based on measured macroeconomic outcomes towards zero %. This may require the introduction of a

Foreign Transactions Surcharge (FTS) to manage capital flows, as set out in the

plan details below.

11 In New Zealand the main contributors to

this are the Family Tax Credit scheme, which provides NZ$2.2 billion (2010)

annually, and the In-Work tax credit scheme, which provides NZ$0.6 billion

(2010) a year.

12 People with real wage rates above $20/hour

less inflation would initially get a pro-rata increase in their virtual minimum

wage to a level above the $20/hour virtual rate. If inflation were 3% and

someone was on a wage of NZ$19.70/hour, their wage would increase by 3% to

NZ$20.30/hour.

04. PLAN

DETAILS.

a).

Increasing the VIRTUAL minimum wage.

One

primary reason the New Zealand economy has not been growing very quickly is

that wages have not kept up with inflation in real terms and the benefits of

modest productivity increases have accumulated to the business gross operating

surplus instead of being passed on to employees.

The

increased virtual wage will stimulate increased production and reduce

unemployment. In the absence of full employment there will be little or no

inflationary pressure. The plan can be continued over time by increasing

workforce participation through greater innovation and productivity. It is also

an axiom of capitalism that people tend to work harder if they know they are

being rewarded for doing so.

Some

workers will use their extra income to reduce debt, especially high-interest

consumer and credit card debt, smoothing the initial positive impact of the

programme. This is a composite part of

the plan designed to reduce the country’s total debt over time.

Some

regulatory provision may be needed to prevent employers seeking to reduce wages, through the loss of jobs by workplace

attrition and subsequent replacement of workers at lower wages, or by failure

to negotiate or pass on the normal real wage increases agreed by wage

bargaining from time to time. Actions of

this type by employers would tend to keep their prices stable, but would lead

to higher injections of credit into the economy as discussed in point b) below,

eventually putting the plan at risk. As

discussed in point c) below, businesses will be well rewarded under the plan

and would be expected to support normal wage levels and normal wage increases

as well.

b).

Injection of electronic cash.

The

Central Bank does not need new legislative authority to make an injection of

electronic cash into the economy. The money in the proposed plan will be used

to

increase virtual wages. It is not a subsidy to business, though business

will be rewarded for its participation in the scheme and to stimulate business

development. The plan is a

non-inflationary way to increase wage-earners’ purchasing power. It is made

possible through the greater

understanding of the operating mechanisms of the existing interest-based debt

system provided by the debt model discussed in detail in the appendices to this

paper.

Each

business will have to demonstrate the number of qualifying employees it has who

earn below the proposed initial virtual wage threshold of $20/hour. That should be apparent from existing PAYE

(Pay As You Earn) tax data. The amount needed to bring wage earners’ pay up to

$20/hour will be deposited weekly into the firm’s business operating accounts

in a manner similar to ordinary government transfer payments together with the

corresponding incentive payment to be made available to businesses. Firms will

have to provide records (as part of their normal PAYE returns) to show that all

the money they receive has been used for its intended purpose. They will

continue to pay workers at their usual (pre-existing) rates of pay together

with any pay increases from time to time negotiated with the unions in the

normal way as wage inflation increments arising from increases in the cost of

living and increases in productivity.

Since

it is likely that a substantial part of the E-Notes injection will be used to

reduce existing consumer and credit card debt it is probable that the initial

programme can be continued over time and expanded beyond the virtual wage of

$20/hour.

Normal

wage increases will progressively erode the amount of the initial E-Note

injection providing an automatic “sunset” clause to the plan should a political

decision be made to discontinue it. To

maintain the effects of the initial E-Note injection, the virtual minimum wage

will need to be increased in tranches as set out below under point h) of the

plan or simply increased incrementally each year.

c).

Business participation.

In

many countries, the business gross operating surplus is 50% or more of the

purchase price of goods and services. It is therefore usually beneficial for

firms to expand production capacity as demand rises. There will be a reward for business

participation in the plan. The reward will take the form of a capital grant.

Businesses will be required to show how they use the capital grant provided to

them to increase productive capacity. All businesses employing wage and salary

workers will be eligible, not just those employing workers below the proposed virtual

minimum wage. The proposed level of 20%

of the planned initial E-Note injection of NZ$ 5 billion/year would provide an

annual capital injection to business of about NZ$ 700 for each FTE (Full Time

Equivalent) worker, or in round terms, about NZ$ 14 per worker per week. This would, in principle, continue as long as

the plan is operative and for as long as individual firms continue to invest in

increased production capacity.

d).

Inflation.

Since

the E-Note injection is not part of production costs firms can continue to

produce the same output as they do now for the same price. The E-Note injection will increase

wage-earners’ consumption capacity, stimulating further new production at

nominally constant prices. It does this by reducing the drain of incomes to the unproductive

investment sector leaving more of the earned incomes (both compensation of

employees and gross operating surplus) for consumption and investment. The need to increase consumption capacity in the short term arises from the

exponentially growing transfer of deposits from the productive sector My to the investment sector Ms. Increase in unearned income Ms will continue as long as interest continues to

be paid on deposits. Increasing debt

levels require an ever-higher proportion of incomes to cover interest payments

for debt servicing. The debt model presented in Appendix 2 shows there will be

a deficit in effective consumer demand in the economy whenever wage-earners’

net incomes fail to fully compensate for increased debt servicing costs and

inflation. This is especially the case

when the OCR is used to increase interest rates in an effort to manage

inflation, producing unemployment and a contraction in consumption and, over

time, a contraction of economic output.

When purchasing

power is increased modestly, the miracle happens as employees spend at least

some of their new income on consumption. Since prices remain very nearly the

same, the increased purchasing power induces added production using existing

unused resources available within the economy. The initial stimulus provided

does not need to be large. In practice it is a lot less than what has been used

in countries such as the

Normal

wage increases and new growth would initially continue producing systemic

inflation in

e).

Indexation of transfer payments including Superannuation.

Indexation

of transfer payments on a tax-neutral basis does not change the figures

referred to under points a) to c) above.

The higher virtual minimum wage level results in higher employee

incomes. A substantial portion of that wage increase is transferred back to the

government through taxation. The

government then redistributes that tax, leaving the global increase in

purchasing power intact, but further improving its spread amongst the

population. Some existing transfer payments should fall as the rate of

employment increases with economic expansion. People on other benefits should

become more motivated to seek work because the higher minimum virtual wage

allows them to escape the poverty trap 13. This plan assumes such

budget “savings” would be used to increase the transfer payments to the people

still needing them. Whether the government of the day chooses to increase the

present level of social welfare transfers and, if not, what it does with the

resulting ‘savings” becomes a matter for public policy debate.

f). Other

forms of income support.

As

lower income levels rise, the need for supplementary income support through

programs such as the

13 The term “poverty trap” refers here to

situations arising under the existing

14 In

g). Wage restraint.

The trade union movement is expected to be

strongly attracted to the plan because it will improve the purchasing power of

many of its members. A unique feature of

the plan is that it provides a systemic bottom up approach to reducing income

disparity rather than a top down approach.

The plan is neutral on taxation rates, which are considered to be a

political matter.

The plan does not remove systemic inflation from

the economy though it will reduce it over time through the reduction in the

OCR. As in the past, wages may increase to reflect price changes induced by

inflation as well as to allow employees to enjoy a share of increased

productivity. Such wage increases will

also apply to those benefiting from increases in the virtual minimum wage. They

are included in systemic inflation. The

whole economy will continue to inflate by an amount equal to the systemic

inflation, which is expected to be about 1.8% in

It would be advisable to keep annual wage

increases to less than 2.5%, that is, up to 1.8% for inflation (reducing as

inflation falls) and 0.7% for productivity gains.

An agreement with the unions would be helpful

because there will be some pressure to increase incomes above the median wage to

restore skill differentials in the labour market. Skilled employees should not

be worse off under this plan than they would have been without it. Upward

pressure among middle incomes could be dealt with by making the tax system more

progressive by adjust adjusting tax thresholds to maintain income

differentiation. 15

15 One way to do this would be to replace

existing taxation with a single

automatically collected Financial Transactions Tax (FTT) . The FTT would be deducted whenever

transfers are made out of any deposit account except a savings account in the

name of the same depositor. That would

raise “consumption” taxes by about 80% and allow all other taxes except

excise/social taxes to be abolished. FTTs are strongly progressive because they

would apply to all transactions, not just those in the productive economy.

Assuming total transactions of 1.8 x GDP, to raise, say, $65 billion would

require an FTT of around 19%, not much higher than the new GST of 15%.

h). Plan extension.

There

is enough spare capacity in

Most

New Zealanders on low incomes struggle to make ends meet now. The bulk of the

first cash injections will probably go into new consumption as they are

intended to do rather than into debt reduction. This will change as further

cash injections make debt reduction more feasible.

Economists

and political leaders throughout the world are calling for an end to

exponential debt growth. This plan does

that by progressive credit monetisation of the existing debt as well as by

permanently reducing the OCR (Official Cash Rate) towards zero, at which point

systemic inflation would be removed from the financial system.

i).

The banking system.

This

plan will progressively and significantly increase cash deposits in the banking

system. The difference between cash

deposits and deposits arising from debt is that cash deposits reduce the banks’

risk-based capital requirements thereby increasing their lending capacity. Nobody can default on a cash deposit because

it can’t be liquidated. Cash deposits remain somewhere in the banking system

unless they are used to repay debt. That

makes a credit (electronic cash) based financial system inherently more stable

than the existing debt-based system.

Bank

deposits will continue to increase, but at a slower rate than during recent decades.

The increased deposits will result from population expansion and from residual

systemic inflation. They will tend to be offset by increased productivity

derived from increases in employees’ purchasing power. The growth of debt in

the economy will reduce towards zero as the OCR is progressively reduced

towards zero, eventually eliminating most, if not all, exponential debt growth.

One

main element of past exponential debt growth has been the use of the price

mechanism to “manage” it. This has turned out to be a perverse system. The debt

model set out in the appendices shows how raising interest rates increases

systemic inflation instead of reducing it.

During downturns and recessions the systemic inflation is still there.

Higher systemic inflation is, however, masked by falling purchasing power

caused by higher debt financing costs, and falling production with aggregate

discounting of goods and services by producers leading to a reduction of their

gross operating surpluses. The systemic inflation is not visible in consumer

prices and therefore tends to go unnoticed and unmeasured.

Since

cash deposits increase banks’ nominal lending capacity this paper proposes

using variable supplementary bank reserve ratios to limit bank lending. This is

to avoid risk of added inflation caused by increases in circulating productive

transactions deposits My over and above what is needed to maintain real GDP growth within the

resource constraints of the economy.

There

is nothing new about reserve ratios for bank lending. Most countries still have

them in some form even though they have usually played a minor role in economic

management in recent years. How the supplementary deposit ratio to be

incorporated in the plan is framed is outside the scope of this paper. Its

purpose is to slow down the exponential growth of bank lending as new debt is

replaced by electronic cash injections so that systemic inflation can be

reduced and eliminated altogether over time.

Over

the longer term, household debt can be first stabilized and then gradually

reduced. The banks will be gradually transformed into savings and loan

institutions. This process will reduce systemic banking risk while at the same

time maintaining banks’ profit margins.

The

main change under the plan will be the elimination of unsustainable exponential

debt growth. This is what the world wants to happen. Unlike this plan, orthodox

economics offers no mechanism to achieve it.

j).

Reducing the OCR.

The

introduction into the financial system of electronic cash credit injections and

supplementary reserve ratios allows the OCR (Official Cash rate) to be

gradually reduced, and systemic inflation to be removed from the financial

system. The financial system becomes

based on the quantity of debt (and E-notes) rather than its price. The persistent problem of exponential debt

growth will be solved. Over time, interest-bearing debt can be removed entirely

from the financial system.

From a

systemic point of view, the decline in the OCR can be carefully managed to allow

the

The

plan does not, of itself, resolve either the current account deficits of debtor

nations or the current account surpluses of creditor nations. It does, however, provide a platform from

which the exchange rate and current account can be effectively dealt with using other options such as the

Foreign Transactions Surcharge (FTS) discussed briefly in Section 5 below.

The

plan has been conceived to avoid significant additional costs for exporters.

Except for tourism, most producers of

From

the structural macroeconomic point of view debtor countries clearly need to get

their current account deficits under control.

One mechanism to do this is by applying a variable Foreign Transactions

Surcharge (FTS) whereby a currency exchange surcharge is automatically

collected whenever domestic currency is converted into foreign currency. It would have no effect on export prices, but

it would increase effective import prices. The proposal would be made tax neutral

by reducing domestic taxation by the amount of the surcharge collected.

05. THE FOREIGN TRANSACTIONS

SURCHARGE (FTS).

It is advisable to introduce a Foreign

Transaction Surcharge (FTS) as soon as possible to protect against the export of

assets (financial leakage) offshore and progressively repay the nation’s

foreign debt.

An FTS would be

simple to administer 16. It has very rarely been used in the past 17.

Introducing a financial instrument such as the FTS is essential in the medium term

if offshore borrowing and related interest costs, which are among the main

causes of exponential inflation in

A broader issue is whether a

foreign transactions surcharge would contravene international financial

agreements. There are provisions in the relevant international World Trade

Organisation (WTO) protocols for countries to protect their balance of

payments. The GATT legal text, Article XI clause 1 appears to specifically

permit non-discriminatory taxes to be applied. Provision of funding is a

service that falls under the GATS protocols.

The so-called policy “trilemma” referred to in

paper 1(cited in Appendix 2) is important to any debate on the FTS. Obstfeld

(1998) put it this way: “In most of the world's economies, the

exchange rate is a key instrument, target, or indicator for monetary policy. An

open capital market, however, deprives a country's government of the ability

simultaneously to target its exchange rate and to use monetary policy in

pursuit of other economic objectives” 20.

16 The “beauty” of FTS is that it applies to

outward capital flows, not inward capital flows. Moreover, FTS is not a

“restriction” on capital flows , it is a universal tax on all outward

transactions.

17 It was used successfully in

18 As discussed briefly at page 12 of the

paper “The Interest-Bearing Debt System and its Economic

Impacts”.

19 Setting the parameters for that regulatory

framework falls beyond the scope of this paper.

20 See also Rosenberg, Bill “Financial Crises,

Trilemmas, and a Time to Rethink”, Foreign Control Watchdog, 120, (2009).

If the current account is to

be managed, some form of exchange management will be required. To restructure

the financial architecture as proposed in this paper, a tool such as the FTS

will have to be inserted at the currency exchange interface. Failure to do so could condemn the world to

economic ruin. It is now widely, if not yet universally, acknowledged the

current economic system is deeply flawed as suggested or implied in recent

articles from the Bank for International Settlements, the World Bank, and

leading economists like Joesph Stiglitz 21 and Paul Krugman.

The exchange management

instrument(s) would apply to all outward exchange transactions, not just

outward capital flows.

The proposed FTS is

not a tariff or trade barrier of any kind. Nor is it a restriction on capital

flows as such. It can be adjusted

Financial receipts

from the surcharge would be used to offset a corresponding amount of domestic

taxation (for example by reducing GST), to make the surcharge tax-neutral apart

from any receipts put towards foreign debt reduction. Its intent is to correct

the current account, which is part of the balance of payments as defined in the

legal WTO, GATT, GATS texts, by removing the existing subsidy enjoyed by those

engaging in foreign currency transactions at the expense of those who do not.

Those using foreign currency in

The proposal for an

FTS also deserves mention in the context of ongoing negotiations for a TPPA

(Trans-Pacific Partnership (Free Trade) Agreement) presently being negotiated

among eight

21 For example the Report of the United Nations (UN) Commission of Experts

on Reforms of the International Monetary and Financial System, 2009, chaired by

Joseph Stiglitz: (the “Stiglitz report”)

22 Under the gold standard, capital flows

appear to have been unrestricted, but they were not the dominant feature in

financial flows they have become in recent decades and current account imbalances were reflected in changes in gold

reserves.

23 The famous Bretton Woods meeting was where

the basis for the post World War II financial architecture was agreed among the

allied powers. The British position was effectively vetoed by the

24

25 For example,

26 The author of this paper is not aware of

any remission policy in cases where the PPMs (Process and Production Methods)

is MORE carbon efficient than the

corresponding

The overall saving

to the wider New Zealand economy from the introduction of an FTS is likely to

be more than the annual current account deficit itself

A foreign

transactions surcharge would cause the exchange rate to fall towards a stable

base level, allowing exports to increase and imports to decrease, providing a

more even playing field for local manufacturers and producers 28. At the moment they face a severe economic

disadvantage through the hidden costs represented in the status quo.

Introduction of the

FTS could allow the removal of all remaining tariffs and subsidies in the

The FTS can also be seen as a

correction designed to offset the unmanaged volatility in

27 Each 1% in interest rate alone

represents nearly NZ$ 3.1 billion per year on domestic credit of around NZ$ 310

billion, as at March 2011. Estimating the actual economic effect of FTS is outside

the scope of this paper, but, according to the System of National Accounts,

every dollar off the current account deficit is a national “saving” before

taking into account other benefits.

28 Rose (2009) notes that

exchange rates have relatively little influence on imports, but it is likely

that the FTS would act more directly on the import sector because it is visible

as it is drawn directly from bank accounts.

29 Source: Reserve Bank of

30 New Zealand National Accounts

for the year ended March 2009.

31 The outward payments could

fall from their present level and inward receipts would probably increase.

That would be enough to reduce

GST to 10% from 15% and begin foreign debt repayment

There would be a substantial

reduction in interest payments as the current account is brought under control,

the reduction of foreign ownership begun and inflation reduced to very low levels.

Rose (2009) notes: “Effectively the

market is pricing country and/or currency risk into national interest rates”.

On the other hand, the

That would produce a sharp fall in the exchange rate.

The FTS is a very powerful economic tool because of its indirect redistributive

impact within the domestic economy 34. Its introduction would also prevent a

reversal of the so-called “carry trade” 35 once domestic interest

rates have been reduced to low levels.

32 This could be done through

some form of tender process. The worked indicative

example for Option (B) at Table

33 The Keynesian transfer problem

implies the current account should go far enough into surplus to meet all transitional foreign investment

claims, though that might be optimistic in the short term.

34 On the other hand, debtor

countries may be better off “biting the bullet” and dealing with their foreign

debt sooner rather than later. Since the volume of exports cannot be rapidly

increased, the FTS must rely on changing the relationship between the NZ$ value

of exports and imports.

35 The carry trade is the

practice of transferring deposits from countries where deposit interest is low

to countries where deposit interest is high(er).

The share of the

“

That those annual servicing

requirements should be more or less equal to

Banks would quickly unwind

their dependency on foreign debt when the funding rate falls below what they

are paying offshore. Transitional

arrangements may be needed to favour the replacement of foreign funding with

domestic funding.

Some academic

literature supports the need for some form of foreign exchange management to

correct the balance of payments and the current account. “Pegged” exchange rates

have been widely used by major countries, including

Preston (2009)

argues that the levels of the

The FTS outlined

above is much broader in scope than

06. CONCLUSION.

The

paper sets out the underlying economic problems relating to the exponential

growth of debt and offers a detailed plan to deal with them. The private

interest-bearing debt-based financial system generates systemic exponentially

increasing transfers of wealth from the productive sector of the economy to the

investment sector. The transfers take

the form of net interest paid on bank deposits. The deposit interest has to be

funded from the productive economy. This causes an inflationary expansion in the

debt levels the productive economy has to service. Over the past few decades, the orthodox

economic approach to that inflationary expansion has been to increase the price

of debt by raising interest rates. Not only is that approach shown to be

counterproductive but debt levels in developed economies are now so high that

small increases in interest rates are enough to force them into recession. The

consequence it that interest rates now have to be reduced close to zero to

stimulate the economy.

The

proposed plan resolves the exponential debt problem. It is limited in its scope

to reducing debt in the economy and stimulating sustainable growth.

The

plan introduces the concept of a virtual minimum wage. In

Debt reduction

occurs as people receiving the stimulatory payments use some of them to repay

existing consumer debt and mortgages 36. Debt is progressively

replaced by electronic cash circulating in the economy at the same speed as

existing bank debt. The paper shows the

debt reduction process can probably continue indefinitely. The proposed cash

injections become self-limiting as normal wage increases reduce the difference

between ordinary wages and the virtual minimum wage. The plan can then be

extended by increasing the virtual minimum wage first from NZ$ 20/hour to NZ$

23/hour and then to NZ$ 25/hour. Each of

those extra increases has approximately the same effect as the original

increase to NZ$ 20/hour; being about 2.6% of GDP. The program can be continued in stages,

and progressively broadened until most

debt in the economy has been retired and

the economy is permanently

working at full capacity.

36 Injections by the Japanese Government failed

to adequately stimulate the Japanese economy in part because of the debt

substitution that took place. Instead of stimulating consumption some private

debt was replaced with public debt.

The plan is accompanied by at least two monetary

instruments. The first is the introduction of a supplementary deposit ratio

into the banking system and the second is the introduction of a foreign

transactions surcharge to manage the current account and retire foreign debt.

The supplementary deposit ratio is applied in

addition to the Basel III risk based capital requirements under which the

banking system operates at present. The

supplementary deposit ratio enables the effect of the E-note injection to be

sterilised (offset) so that new bank lending is correspondingly reduced. This eliminates the possibility of inflation

being caused by an oversupply of new interest-bearing bank debt as the Official

Cash Rate (OCR) is reduced towards zero.

Lowering the OCR will progressively remove systemic inflation from the

economy.

The Foreign Transactions Surcharge (FTS) serves

two main purposes. The first is to limit any capital flight as the OCR is

reduced. The second is to provide a powerful ongoing instrument to regulate the

exchange rate and progressively repay the nation’s foreign debt. The FTS is a variable tax on all outward transfers

of NZ currency. It would start at about 10% and be automatically collected

through the banking system. The income received would be used to reduce

domestic taxes, such as GST, and to begin reducing foreign ownership. The proposed 10% initial level for the FTS is

much lower than the recent percentage variations in the NZ$ exchange rate. The

proposed FTS rate would apply to ALL exchange transactions including

speculative financial transactions. It

appears to come within the context of existing international protocols such as

GATT and the WTO that allow for protecting a nation’s balance of payments. It

is important that this position be reserved in any TPPA (Trans-Pacific Partnership Agreement) the

country decides to enter into.

07. APPENDIX

1 : THEORETICAL BACKGROUND.

The

first paper of this series “The Interest-Bearing Debt

System and its Economic Impacts” 37 looked at the fundamental

cause of exponential debt growth and proposed several key concepts:

(a) The fundamental debt problem is that the

economy has institutionalised the payment to deposit holders of unearned

income.

(b) That unearned income takes the form of interest

paid on bank deposits.

(c) Interest paid on bank deposits creates

systemic inflation and exponential increase of the debt burden.

(d) Culture

and institutional “capture” of the debt debate has made rational discussion of

the debt problem difficult.

(e) Sustainable debt levels cannot be achieved without removing most

if not all new deposit interest.

(f) Quantitative analysis can be provided using a new debt model of

the economy based on a revised form of the Fisher Equation of Exchange.

The paper “The Interest-Bearing Debt System and its Economic

Impacts” showed that the debt system in

The productive

economy is progressively becoming paralysed. The exponentially growing pool of

unearned deposit income is funded by inflation of the productive economy. The

unearned income investment sector is becoming so large that servicing the

nation’s total debt requires inflation close to the deposit interest rate 38.

The present situation has probably never arisen before, not even during the

depression of the 1930’s.

Orthodox economic

instruments such as the use of interest rates to manage inflation mask systemic

inflation at the cost of economic growth as shown in Figures 2 and 4 of

Appendix 2. The inflation cost is still

there and it is still being paid, but it is being paid in the form of lost

production and unemployment instead of showing up in prices.

Appendix 2 provides

detailed evidence of the current position for

The world’s

financial system is approaching a state of collapse and cannot be repaired

using orthodox economic theory. Orthodox

economics has failed to reveal the fundamental mechanisms at the root of the

debt problem or to offer any practical long-term solution to address it.

37 L.F.Manning, for Sustento Institute,

38 Some

of the inflation is masked by the current account deficit and offshore

borrowing.

08.

APPENDIX 2 : THE THEORETICAL SUPPORT FOR

THE PROPOSAL.

The theoretical basis for this

paper is the debt model shown below which is the same as the one described in “The Ripple Starts here….”39 and the first paper of this

series “The Interest-Bearing Debt

System and its Economic Impacts” cited above. The debt model is

based on the Fisher Equation of Exchange amended as follows:

While the debt

model is based on the volume of debt, it is unrelated to earlier volume-based

reform proposals like those of Social Credit that failed to offer a viable

theoretical basis to support them.

The premise in the

debt model is that the circulating deposits and cash My = Prices P * output q where q

is the quantum of domestic output produced by My over a single cycle. Taken

over a whole year, the SNA definition of Gross Domestic Product GDP is given in

the debt model by mathematically integrating the expression Pq* Vy, where Vy is the number of times the

circulating deposits and cash My are used during the year 40.

The SNA should

reflect an expression of the original Fisher Equation of Exchange as shown in

Figure 2 41. The only difference is that the money supply

M in the Fisher equation of exchange included hoarded cash, whereas in the debt

system shown in Figure 2 for practical purposes there is now very little cash

contributing to measured GDP.

In circulating cash

and deposits My cannot include

hoarding of debt beyond the term of the production cycle because all the

productive bank debt giving rise to My is conceptually repaid at the end of the cycle 42.

39. “The Ripple Starts

here….”

40. The contribution of cash transactions in industrialised countries is

now (very) small.

41. The Fisher equation has been very widely discussed in relation to the

economic difficulties arising from the sub-prime mortgage defaults in the

42. As previously noted, in practice there is a continuous flow of production

and consumption so the deposits and cash My are always

present, but they are being used in the production cycle, not hoarded.

At any point in

time there are five broad blocks of deposits in the domestic financial system.

They are:

Mt The transaction

deposits representing the productive debt My - M0y so:

My =

Mt + M0y (1)

Mca The accumulated

domestic deposits representing the sale of assets to pay for the accumulated

current account deficit.

M0y The cash in circulation

included in Mv and used to contribute to

productive output.

Ms The net after tax accumulated deposits arising from

unearned deposit income on the total domestic banking system deposits M3 (excluding

repos) 43.

(M0-M0y) Cash hoarded by the public and not used

to generate measured GDP.

In this paper the

total of these deposits, that is, Mt + Mca + M0y + Ms , is provisionally assumed to

be the M3 (excluding repos) monetary aggregate published by most central banks

monthly less the amount of cash in circulation M0 except for the part M0y that is included in My. In this paper M0y is assumed to have the same

speed of circulation as My. In industrialised countries,

the contribution of cash transactions to the measured output of goods and

services (GDP) has been declining in recent decades and their contribution to

the GDP has been provisionally calibrated for the purposes of this paper 44.

In this paper, the

total debt in the domestic financial system is assumed to be the Domestic Credit,

DC debt aggregate published by most central banks monthly.

At any point in

time there are four broad blocks of domestic debt in the domestic financial

system. Three of them together add up to DC such that:

DC = Dt + Dca 45 + Ds

(2)

Where

Dt The productive debt supporting the transaction

deposits Mt.

Dca The whole of the debt created in the

domestic banking system to satisfy the accumulated current account deficit 46.

Ds The residual debt to balance equation (2)

43. Repos refer to inter-institutional lending

44. More accurate assessment of the cash contribution to GDP over time

requires further detailed study.

45. Arguably the accumulated sum of capital transfers could be included

here, in which case the net international investment position (NIIP) would be

used instead of the accumulated current account. The decision affects the size

of the “residual” Db.

46. This is greater than the monetary deposits Mca because the banking system may have sold commercial paper to borrow

foreign currency to satisfy the foreign exchange settlement.

The fourth block of debt is :

Db, the virtual “bubble” debt, the

excess credit expansion or contraction in the banking system such that Ds - Db = the debt supporting the accumulated deposit interest Ms defined

above. Db can be positive or negative as discussed further below

in relation to Figure 5.

There is also a

fifth block of debt Is that is, conceptually, not bank debt .

Is, the total debt accumulated by

investors arising from Saving Sy = S/Vy.

The investor pays

the investment Iy =I/Vy = Sy = S/Vy to the producer and the money is used to

retire the outstanding part of My relating to the investment in

question. Conceptually the investor borrows the purchase price from employee

incomes and the business operating surplus. Except for households buying new

homes, the investor then becomes a producer, and the interest on investment Iy is included as a production

cost in the subsequent production cycle loans My.

The predicament of

new homeowners is quite different. They cannot service their debt because they

cannot, conceptually earn more than they were before they bought their new

home, because the home itself is nearly always unproductive. There is no new

income stream from their housing investment. If economic demand is to be

maintained, homeowners must, in aggregate, rely upon increasing house prices

and refinancing of their properties, creating an aggregate “pass the baton”

systemic increase in debt.

When non-productive investment assets

are traded there is typically a capital gain because of asset inflation on

investment (Dca + Ms + the property component of Is). The new purchaser pays more for the asset

because of asset inflation, allowing the seller to retire the outstanding

mortgage debt on the property.

By definition in this paper :

My * Vy = GDP

Ms = Ds

The cash contribution to GDP =

M0y * Vy. Therefore :

DC = (GDP)/Vy - M0y + Ms + Dca

+ Db (3)

Ms =Ds =

(DC – Dca ) – GDP/Vy + M0y - Db (4)

GDP = Vy *(DC - (Ms +Dca

+Db ) + M0y ) (5)

My = GDP/Vy

= DC - (Ms +Dca + Db) + M0y (6)

Where the terms are as defined

above.

Equations (3 ) to

(6) are all forms of the debt model developed in previous papers 47.

47. Links

are provided in the conclusion to this paper.

Ms is the same format as Ms in

the earlier forms of the model. It has been freshly calibrated. Unlike the

previous forms of the model equations (3) to (6) are general and include the

contribution made to the economy by cash transactions.

In equation (4),

all the terms except GDP/Vy = My and Db are known or can be estimated

with reasonable accuracy. For the purposes of equations (1) and (6) My can be approximated using trend-lines because it is small

compared with Ms. Db is unknown but can be

approximated through the calibration as in Figure 5. The calculations in

equations (5) and (6) involve the subtraction of large numbers to get

relatively small numbers, which leaves them sensitive to modelling and data

error.

If Ms , calculated as “the

accumulated deposits arising from unearned deposit income on the total domestic

banking system deposits M3(excluding repos) ”agrees more or less

with that calculated in equation (4), bearing in mind the value of Mb , the proposition that debt

growth is determined by deposit interest will be proven. The model will require

further calibration as further data becomes available. Despite that, it is self-evident Db will be positive during periods of rapid expansion,

particularly as bubbles form, and will become negative during periods of rapid

contraction, particularly as bubbles collapse. The classic case of this in

The dependence of

the gross domestic product (GDP) on the Domestic Credit DC and the interest

rate on bank deposits in the modern cash-free economy from which Ms is calculated has profound

implications for economics.

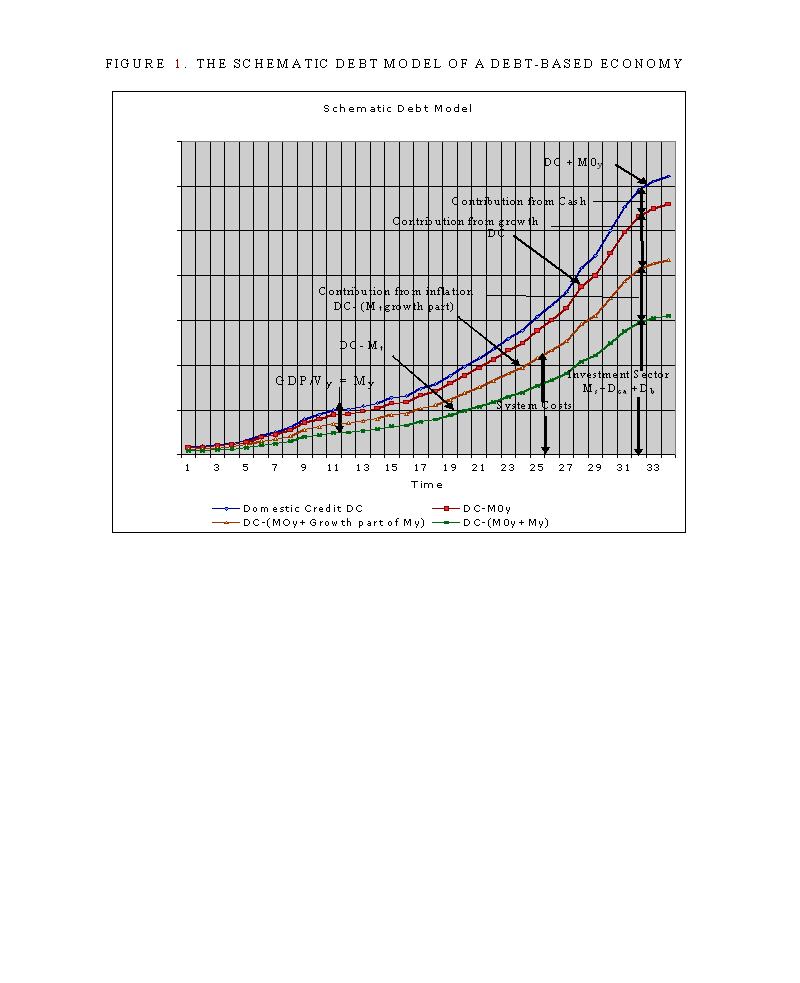

In the light of the

worldwide financial chaos of 2007-2009 the indicative debt model shown in

Figure 1 provides a powerful argument in support of public control of a

nation’s financial system.

Click here to view FIGURE

1 : THE SCHEMATIC DEBT MODEL OF A DEBT-BASED ECONOMY.

{kind=link}

The vertical axis

in Figure 1 applies to the Domestic Credit for

It isn’t possible

to have a simpler model of the economy than equation (5):

My

=Nominal GDP/Vy equals domestic credit DC less (unearned net deposit

income Ms + the accumulated current account Dca + the

cash contribution to GDP M0y plus a correction for bubble activity Db

(+/-))

Domestic

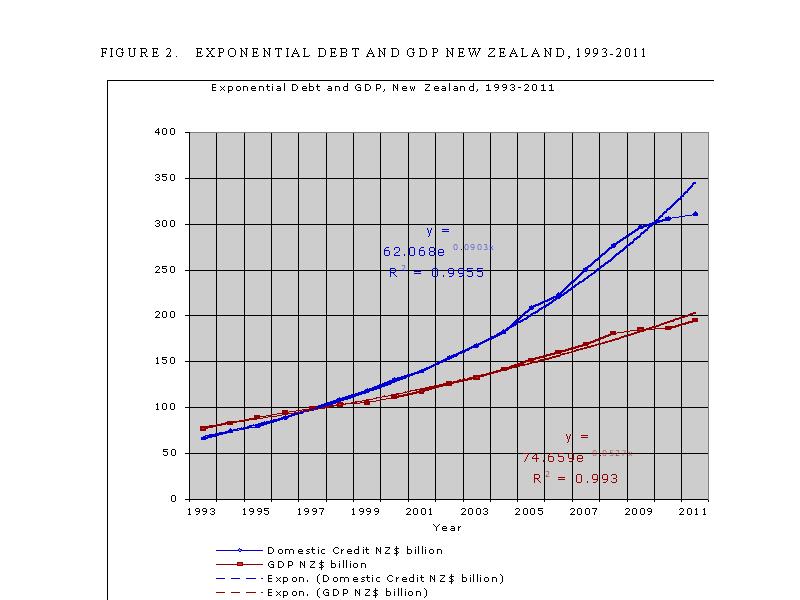

Click here to view FIGURE

2 : EXPONENTIAL DEBT AND GDP NEW

ZEALAND, 1993-2011.

{kind=link}

It is theoretically impossible

to maintain exponential debt expansion faster than GDP expansion over an

extended period because the added debt servicing costs will always leave the

productive sector insolvent.

To avoid national

bankruptcy, each nation must maintain, in aggregate, a zero accumulated current

account deficit.

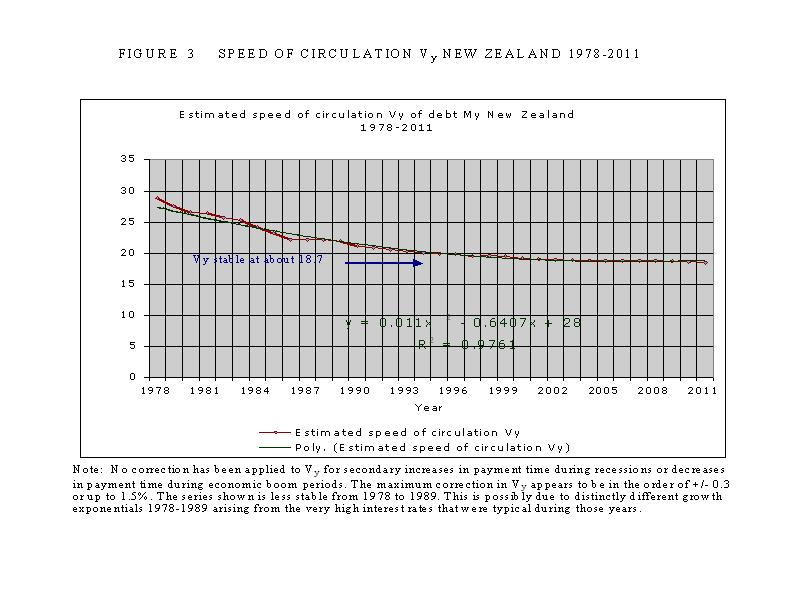

A first

approximation for the speed of circulation Vy of productive debt plus cash

transactions My is given in Figure

3. Vy varies with the

change in the payments systems. Minor secondary shorter-term cyclical variability

also occurs through changes in the average time taken to pay bills. When times

are tough people take longer to pay their bills, and each change of a day in

the time taken to pay them can alter Vy by perhaps 0.25%.

The process is usually reversed in better times. Otherwise Vy reached a constant value of

about

48. Vy is estimated at the moment

so the present figures are indicative. Once further research accurately refines

the present estimates, Vy will be

sufficiently accurate for predictive purposes.

Click here to view FIGURE

3 : SPEED OF CIRCULATION Vy NEW ZEALAND 1978-2011.

{kind=link}

Note that in Figure

3, no correction has been applied to Vy for secondary increases in

payment time during recessions or decreases in payment time during economic

boom periods. The maximum correction in Vy appears to be in the

order of +/- 0.3 or up to 1.5%. The series shown is less stable from 1978 to

1989. This is possibly due to distinctly different growth exponentials

1978-1989 arising from the very high interest rates that were typical during

those years.

As shown in Figure 4, My in

Click here to view FIGURE

4 : ESTIMATED TRANSACTION FUNDING My NEW ZEALAND 1990-2011.

{kind=link}

The methodology

used to calculate Vy in Figure 4 is as

follows. The GDP in

Businesses pay

suppliers monthly, and indirect payments are usually made on a monthly basis

too, so their speed of circulation is about 12 on average. Most workers get

paid fortnightly (though some get paid weekly and some monthly) so an average

speed of circulation of 26 has been assumed for that.

When the above figures are

weighted the weighted average speed of circulation is (12 * (42.7+12.3)+45 x

26)/100 = 18.3.

A similar estimate

of payment trends and a separate Vy calculation was made for each of the other years, and

a polynomial best fit curve was drawn as in Figure 4.

My was then obtained by dividing the official GDP figure by

the speed of circulation taken off the best fit trend curve. This gives the data series shown in Figure 5

and used when applying the debt model.

The methodology is

easily replicable using better information about payment trends and is

applicable to any country.

Figure 4 shows the

preliminary estimate for estimated production debt and cash My in

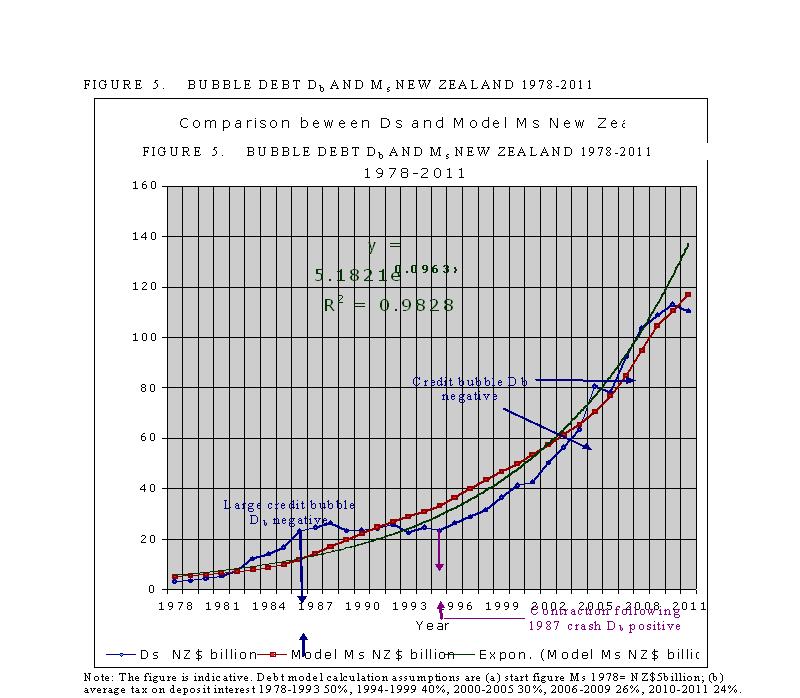

Figure 5 shows an

indicative comparison between the residual debt Ds for New Zealand calculated

from equation (2) and plotted against the model Ms calculated as the accumulated

after tax deposit interest on M3 (excluding repos). The curve for Ms is a first approximation

because assumptions have been made on the average tax deducted from the gross

payments of unearned income (M3 (excluding repos x the average interest paid on

deposits). The tax is the average tax

paid by each income-earner on his or her total income. It is not the marginal

tax rate 49. The losses from the 1987 share market crash

in

Once the tax rates

on Ms have been

accurately calibrated, the size of any debt bubble Db can be immediately calculated. Measures can

then be taken to eliminate the bubble without risking any economic downturn.

Click here to view FIGURE

5 : BUBBLE DEBT Db AND Ms NEW ZEALAND 1978-2011.

{kind=link}

09. BIBLIOGRAPHY.

Allsopp C & Vines D, (2008) “Fiscal policy, intercountry adjustment

and the real exchange rate in

Baker D (2008), “The Benefits of a Financial

Transactions Tax” Center for Economic and Policy Research, December 2008.

Bertram G (2009), “The Banks, the Current Account, the Financial Crisis

and the Outlook”, Policy Quarterly, Vol. 5 Issue 1, February 2009.

Brand C (2010), “Commission Calls for Tax on

Financial Transactions”, 6/April/2010.

Brash D (1996), . New Zealand and international

financial markets: have we lost control of our own destiny?” Address by Donald T Brash, Governor of the

Reserve Bank of New Zealand to the 31st Foreign Policy School,

University of Otago, Dunedin, 29th

June 1996.

Fisher I (1930) “The Theory of

Interest”

George H (1879) “An inquiry into the cause of

industrial depressions and of increase of want with increase of wealth... The

Remedy” Self published in

Kelsey J (Ed) “No Ordinary Deal: Unmasking the Trans-Pacific

Partnership Free Trade Agreement” Bridget William Books, 2010. ISBN

978-1-877242-45-0

Manning L (2009), “The Ripple Starts Here: Finishing the Past 1694-2009”, New

Zealand Association of Economists 50th Anniversary Conference July

1-3 2009, as published under a creative commons licence at www.integrateddevelopment.org.

Manning L, (2010) “The Interest-Bearing Debt System and its Economic

Impacts” Version 3, 18 August, 2010,

Sustento Institute, Christchurch NZ

with the assistance of MEA

(Manufacturers and Exporters Association of New Zealand) as published under a

creative commons licence at www.integrateddevelopment.org.

Obstfeld M (1998), “The Global Capital market: Benefactor or Menace?”

Draft April 27 1998.

Preston D (2009), “Putting Credit back into Monetary Policy:

Reconstructing the New Zealand Monetary Policy Framework”, Paper for NZ

Association of Economists 50th Anniversary Conference, July 1-3

2009.

Rose D (2009), “Overseas Indebtedness, Country Risk and Interest Rates”,

Policy Quarterly, Vol. 5 Issue 1, February 2009.

Unknown authors, (ca. 2000) “Alternative monetary policy

instruments”.

More information on monetary reform :

NEW Capital is debt.

NEW Comments on the IMF (Benes and

Kumhof) paper “The Chicago Plan Revisited”.

DNA of the debt-based economy.

General summary of all papers

published.(Revised

edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

The Manning plan for permanent debt reduction in the national economy.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

Return to : Homepage

"Money is not the key that opens the gates of the market but the

bolt that bars them."

Gesell, Silvio, The Natural Economic Order, revised English edition,

Peter Owen,

![]()

This

work is licensed under a Creative Commons

Attribution-Non-commercial Share-Alike 3.0 Licence.