NGO Another Way (Stichting Bakens

Verzet), 1018 AM

SELF-FINANCING,

ECOLOGICAL, SUSTAINABLE, LOCAL INTEGRATED DEVELOPMENT PROJECTS FOR THE WORLD’S

POOR.

|

FREE E-COURSE FOR DIPLOMA IN INTEGRATED DEVELOPMENT |

|||||

Edition 01 : 06 August 2011.

Edition 02 : 21 September,

2011.

Edition 04 : 09 February,

2013.

(VERSION EN FRANÇAIS PAS DISPONIBLE)

Summaries of monetary reform

papers by L.F. Manning published at http://www.integrateddevelopment.org

NEW Capital is debt.

NEW Comments on the IMF (Benes and Kumhof) paper “The

Chicago Plan Revisited”.

DNA of the debt-based economy.

General summary of all papers published.(Revised edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

The Manning plan for permanent debt reduction in the national economy.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

THE DNA OF THE DEBT BASED

ECONOMY

THE Disputation on the Power

and Efficacy of the Indulgences of the Debt-BASED FINANCIAL SYSTEM.

By

Out of love and concern for the truth, and with the object of eliciting

it, the following heads are offered for public discussion under the presidency of

the Authors. They request that whoever cannot be present personally to debate

the matters orally will do so in absence in writing.

EMAIL: manning@kapiti.co.nz

JULY

31, 2011: 19B

THE

DNA OF THE DEBT-BASED ECONOMY.

The following

three-dimensional diagram represents the DNA of the debt-based economy. It is tilted

forward from the top to make its features easily understandable.

The diagram is made

up of two mirrored helical strands of financial DNA. The blue strand represents

the total accumulated GDP output for a given period while the red strand

represents the total outstanding productive investment principal. The vertical

axis of the helices represents time. The diagram shows a random period of four

years.

On the blue helix,

Vy bases of production output My are added over the time

span needed to make one full turn of the blue helix (usually a year). On the

red helix, Vy bases of national saving Sy (net new

productive investment) are added over the time span needed to make one full

turn of the red helix (usually a year). For ease of consultation, the bases of

production output My and the bases of national saving Sy are

shown only for year three. The drawing shows nineteen of them, as this is the

approximate speed of circulation Vy of productive deposits My

in

The helices

replicate by extension. The blue helix showing GDP “dies off” at the end of

each period. The helices grow exponentially by the transfer of National Saving

Sy from the blue helix to the red one over each notional production

cycle.

For each of the

bases the national saving Sy is returned to the next production

cycle on the blue helix in the form of net new capital investment Sy

(Saving = Investment) as shown. Individual bases can vary in size (up or down)

reflecting the state of the economy.

The annual length

or growth ring Lz of the blue helix shows the GDP as it

accumulates during that year. The

nominal, usually annual, GDP growth in the blue DNA is the change in length Lz

of the DNA spiral over the period z compared with the corresponding length L z-1

over the previous period. In the diagram, the length (and therefore the

diameter) of the GDP spiral is shown to be increasing exponentially from year

to year.

The annual increase

in the length of the growth ring Lz of the red helix shows the

annual increase in outstanding investment

principal S which also equals the nominal GDP growth for that year. The total

length of the red helix at any time is the sum of all outstanding investment

principal. It equals the current

(annual) GDP at any time.

At the end of each

(annual) period z (and only then) the value of output represented by length Lz

of the blue helix (the GDP for that year) equals the value represented by the

whole of the red helix (its total length representing the sum of all

outstanding investment principal).

The plan diameter

of the helices typically expands exponentially. The helices vary together with

the state of the economy. In the case of recessions they show up as changes in

the annual rate of increase of the

helix diameters, and therefore the length of the spiral loops. In the case of

depressions they would show up as an actual

annual decrease in the helix diameters.

Click here to view

a drawing showing

the DNA of the debt-based economy.

{kind=link}

Click

here to see a visual form of the debt model.

{kind=link}

A UNIFIED TEXT OF THE

MANIFESTO OF THE DEBT-BASED ECONOMY.

This document presents unified texts of the 95 principles included in the

Manifesto of the Debt-Based Economy. They are organised in a logical order of

sequence under the various subject headings. The revised Fisher equation

showing the debt Model is described in the Appendix.

Debt.

For practical

purposes, debt-based financial systems in modern industrialised countries are

cashless. In industrialised (and most other) countries, privately owned banks

create new debt and charge their clients for doing so. In the

debt-based system the debt is created before its corresponding money deposit.

Except for residual

cash transactions, in a debt-based financial system there is a unit (dollar) of

debt for every unit (dollar) of “money”. For every unit (dollar) “saved” by one

person there is a unit (dollar) of debt owed by another.

Debt can only be

used once. Once debt is used it must eventually be repaid with interest. Unless

it is written off by bank failure, existing debt can be repaid only by reducing

the banking system deposits or net worth.

Debt growth.

The debt based

financial system is dynamic and independent of orthodox economic equilibrium

theory. Orthodox economics offers no mechanism to achieve

elimination of unsustainable debt growth. As the ratio of unearned income to

GDP increases, the ability of the productive economy to fund the pool of

unearned income decreases.

Net after-tax

interest paid by banks on their clients’ deposits forms an exponentially

increasing pool of non-productive unearned interest income that is never repaid

and is a structural part of the debt-based financial system. The interest rate

on deposits must be eliminated if the exponential growth of the pool of

non-productive unearned income is to be stopped. Unless the deposit interest

rate is zero, Domestic Credit, unearned deposit income and nominal GDP must all

grow exponentially because, in the debt based financial system, they are all a

function of the deposit interest rate.

In the absence of

realised capital gains it is impossible to maintain exponential debt expansion

greater than GDP expansion over an extended period because the added debt

servicing costs will always leave the productive sector insolvent. The debt

supporting the exponentially increasing pool of non-productive unearned income

leads to an ongoing transfer of real wealth from the productive sector to the

non-productive investment sector.

Credit bubbles, recessions and depressions result from the failure of

the banking sector to properly align demand for credit with the productive

capacity of the economy. Credit expansion in the banking system above what the

debt system requires means there is a bubble in the economy while credit

expansion below what the debt system requires means there is a recession or

depression in the economy. A credit bubble or economic contraction is

neutralised when credit expansion has been adjusted so that it just satisfies

what the debt system requires taking into account the full productive capacity

of the economy.

There is no “money”

multiplier in the debt based financial system other than the (slightly) variable speed of circulation of

the transaction deposits actually used to generate productive economic output.

Exponential debt growth can be eliminated by progressive credit

monetisation of the existing debt and by permanently reducing the OCR (Official

Cash Rate) towards zero, at which point systemic inflation caused by interest

paid on deposits would be removed from the financial system.

Inflation.

Systemic inflation

and exponential debt growth are caused by interest paid on bank deposits.

Interest paid by banks on their clients’ deposits forms an exponentially

increasing pool of non-productive unearned income that is a structural part of

the debt- based financial system and cannot be repaid.

In a debt-based

economy where interest is paid on deposits, systemic inflation is half the

interest rate paid on deposits provided adjusted wage rates rise in line with

that systemic inflation plus productivity growth and there are no changes to

indirect taxes. Systemic inflation arising from deposit interest automatically

reduces towards zero as deposit interest rates reduce towards zero. However, in

the absence of quantity controls on the issue of new debt, low interest rates

can lead to unproductive “bubble” lending, thereby increasing price inflation.

In an economy based

on interest bearing debt, almost all price is inflation. Aggregate consumer

prices inflate with the deposit interest rate so that deposit interest on

existing productive investment can be paid into the unearned income pool

without disrupting the productive economy. Increasing interest rates to manage

inflation increases the flow of deposits from the productive sector to the

investment sector by increasing the unearned income pool. It is no longer possible to combat inflation

by substantially increasing interest rates (or to stimulate growth by reducing

them) because modest increases in interest rates are now enough to drive the

economy into recession.

Foreign ownership

of a part of a debtor economy causes asset inflation there because there are

more domestic deposits available to fund the exchange of assets remaining in

domestic ownership.

The supply of new electronic cash (not debt) to businesses to fund

virtual increases in minimum wages does not necessarily cause immediate increases

in prices because the E-Note injections are not part of production costs and

some of the extra wages will be used for private debt retirement.

Banks.

In a debt-based

system, the interest banks charge their clients to provide goods and services

(the bank spread) is part of productive economic activity and does not cause

inflation. When the bank spread and costs are constant, the larger the total

debt of a nation the larger the turnover of the banks and the more profit they

make.

Deposit interest paid by banks to their

clients is not specifically beneficial to the banks but is the fundamental

source of systemic inflation in the debt-based financial system. Public credit

and money issue enables domestic banking systems to operate in high growth, low

risk, low interest, low inflation economies while retaining their existing

profit margins.

Gross domestic product (GDP).

The nominal

increase in GDP over any period equals the increase in National Saving, which is

the gross capital formation less principal repayments over the same period.

Productivity growth

is inherently deflationary. It usually affects prices rather than GDP and

declines as an economy becomes more service-based. Except by utilising existing

idle productive capacity, the only way to increase GDP is through new

productive investment through the supply of new transaction deposits to make

use of spare labour and resources in the economy or to increase the skills of

and re-employ existing resources, and by the relationship between the

production of capital goods and goods and services for consumption

Interest rate

reductions stimulate an economic recovery only when the capital gains from the

exchange of existing capital assets produce enough new debt to satisfy the

systemic debt requirements of the financial system.

In a cash-free debt

based economy with zero interest rates on deposits the increase in GDP equals

the speed of circulation of debt in the productive sector times

(a) the change in

domestic credit, less

(b) the current

account deficit, plus

(c) a correction

for any imbalance between the change in domestic credit and what the debt

system requires taking into account the full productive capacity of the economy

Business cycles.

A recession

provides for inflation but not economic growth, while a depression provides for

neither economic growth nor inflation. A recession occurs when the change

(increase) in the total debt (both public and private) over time is less than

what is needed to service the financial system costs made up of the net

unearned interest that has to be paid on all bank deposits plus any new current

account deficit plus any increase in the productive debt used to generate new

economic output. A depression is a deep recession that also fails to provide

for inflation.

Income distribution.

Apart from

utilisation of existing unused productive capacity, the additional production

from new capital assets is the ONLY way to increase earned purchasing power in a

debt-based economy.

The SHAPE of an economy, which is the basket

of goods and services produced in relation to incomes and consumption patterns,

is largely determined by its income distribution. Poor income distribution suppresses

demand for domestically produced goods and services. Since the employed workforce is already producing goods and services, the

SHAPE of the economy must change to improve economic efficiency and promote domestic production.

Socially mandated income

redistribution is necessary to distribute productivity increases throughout the

economy and improve real wages and purchasing power. The application of a

single flat financial transactions tax to all withdrawals from bank accounts

changes the shape of the economy by redistributing income.

Taxation.

Skewed tax systems

benefit a relatively small section of society at the expense of everyone else

because they impair economic performance and economic growth potential by

systemically transferring purchasing power from the productive sector to the

unproductive sector through increased debt and debt servicing.

A uniform wealth tax on all net wealth from all sources is

redistributive because it (gradually) reverses the accumulation of net wealth

inherent in the presently dominant debt-based financial system. A single Financial

Transactions Tax (FTT) automatically

collected on withdrawals from bank deposits can help correct the tax skew

inherent in existing taxation systems that substantially exempt the investment

sector from paying its “fair share” of tax.

Consumption (with housing).

Most residential

housing is economically unproductive once it has been built, thought its

construction is part of the productive economy. Residential housing that does

not generate income is incompatible with a financial system based on

interest-bearing debt.

Assuming incomes are constant and there are no productivity gains or

realisation of capital gains through asset inflation, homeowners must reduce

their domestic consumption by an amount equal to the principal and interest

payments they make on their non-productive capital assets. The reduction can be

(partly) offset through capital gains. Realised values from the

exchange of existing assets must in that case increase by an amount sufficient

to cover both the interest and principal repayments. The reduction in domestic

consumption must otherwise be matched by the export of the

resulting surplus consumption goods and services if structural unemployment and

recession are to be avoided

The process of production and consumption in

the productive economy is self-cancelling wherever it takes place and however

its phases of production and consumption are shared amongst nations. Export of surplus consumption goods and services to avoid structural

unemployment and recession decreases foreign ownership of the domestic economy.

It does not directly improve domestic wellbeing in the exporting country.

Inclusion of a

housing provision in a tax-free guaranteed minimum income (GMI) system allows close matching of the GMI

to existing government income transfer structures in many industrialised

countries

Capital formation.

Capital formation

in a debt-based economy takes place in accordance with the basic tenet of

orthodox economics that National Saving equals Productive Investment. It arises

from the redistribution of employee income and gross operating surpluses of

businesses to purchase the capital goods created by the productive economy.

Production must always, but only just, lead consumption to provide the incomes

that enable consumption to take place.

Saving.

In the modern

world, faster depreciation has swapped longer-term productive investment to

boost existing stock and existing property prices. Saving for productive investment and real GDP

growth as measured using the international System of National Accounts cannot

be restored to modern developed economies unless the protocols around

depreciation are altered, bank lending polices and regulations reviewed and the

serious distortions in the System of National Accounts (SNA) records themselves

are corrected.

In a debt-based

financial system and in the absence of a debt bubble it is impossible to

increase National Saving (and therefore GDP) without increasing production

loans and new productive investment. In the absence of asset inflation, any

attempt to withdraw any part of deposits for non-productive investment purposes

(“savings”) reduces purchasing power in the productive economy or leaves capital

goods unsold, leading to increases in inventory, and subsequent unemployment

and recession. Unproductive savings and pension schemes such as Kiwisaver in

Investment.

The investment

sector represented by the accumulated net after tax interest paid on bank

deposits produces nothing itself and is paid for through inflation in the

productive sector. Increased depreciation allowances speed up principal

repayments and reduce national saving and productive investment. Increased

repayment of debt, including household debt, reduces national saving and

reduces net new productive Investment.

The accumulated net outstanding principal invested in productive capital

goods is equal to the net accumulated national saving because in a competitive

market economy the long-run economic profit of business tends toward zero as

profit falls toward the opportunity cost of capital. Productive investment

represents the redistribution of production incomes to clear the capital goods

market in the productive sector.

Economies in

recession must be stimulated by direct investment in new production because the

lead-time before the benefits of increased productivity from infrastructure

investment exceed the infrastructure costs is usually too long to be effective.

System of national accounts.

The

use of depreciation for measuring economic success has been catastrophic for

the world economy.

When the current account

balance is included as income in the national income and outlay account of the

SNA an entry of equal value entitled “purchase of capital assets on the current

account” should be included on the other, “use of income”, side of the national

income and outlay account.

The National income

and outlay account of the SNA needs to be restructured and the National capital

account consequentially adjusted to reflect orthodox economic theory as

follows:

Use of income side:

= Final consumption C

+ Purchase abroad of non-productive

capital investment goods (=CA)

+ Saving for productive investment S

Income side:

= GDP

+ Current account balance (CA)

less the balance on external

goods and services

less repayments of principal

on outstanding productive investment.

Current account.

Current account transactions are exchange

transactions, not production transactions. To avoid bankruptcy of the

world economy in the long run, each nation must maintain, in aggregate, a zero

accumulated current account.

There is no such

thing as foreign debt; there is only foreign ownership by foreign creditors of

part of a debtor’s nation’s economy either as physical ownership or ownership

of commercial paper. An accumulated national current account deficit reduces

national savings and increases the domestic debt of the debtor country, its

domestic inflation and foreign ownership of its economy. Foreign ownership of a

debtor nation’s economy drains its domestic economic growth through outgoing

current account payments of interest on commercial paper and dividends and

profits arising from the physical foreign ownership of its assets.

The debtor status

of debtor countries can only be managed without affecting their domestic

economies if their exchange rates are reduced so their current accounts become

positive enough to reverse the foreign ownership of their assets. In the

absence of effective management of capital flows and the exchange rate, the

logical outcome of the existing debt system in heavily indebted debtor

countries is national bankruptcy because debtor countries are condemned to

paying high interest rates to avoid capital flight.

Exporting domestic

production (“export-led recovery”) is an unsatisfactory method for reducing an

accumulated current account deficit unless the accumulated deficit is small and

the exchange rate is free to fluctuate independently of domestic interest

rates.

At any point of

time, the current account deficit in heavily indebted debtor countries is

typically just a little more than:

a) the accumulated

current account deficit of the debtor country, multiplied by the average bond

rate in the debtor country, minus

b) the trade

balance of the debtor country for the period, plus

c) the net

repatriated profits of foreign-owned banks operating in the debtor country over the same period.

A positive balance

on external trade swaps domestic growth in the exporting country for foreign

assets in the debtor country and is a positive growth factor for the exporting country’s business

interests. The logical outcome of the existing debt system in creditor

countries is zero deposit interest and stable or falling asset prices (as in

A tax-neutral variable

Foreign Transaction Surcharge (FTS) applied to all outward exchange transactions allows the progressive reduction in foreign ownership of the domestic

economy (the so-called foreign debt) by enabling the exchange rate to fall towards a

stable base level, increasing the value

of exports and decreasing the quantity of imports, and providing a more even

playing field for local manufacturers and producers.

E-notes.

Existing privately

issued interest-bearing government debt can be progressively retired as it

matures and replaced with publicly issued interest-free debt or E-notes spent

into circulation by the Government. E-notes (electronic cash) perform exactly

the same role as existing bank debt.

Zero or low interest credit and money issue

enables economic growth to be tied to the productive economy instead of being

inflated by deposit interest.

Local money systems.

Local money systems

are co-operatively owned interest-free, self-cancelling monetary systems in

which there is no systemic debt because the debt incurred during the production

phase is cancelled when the product or service is sold. They can be organised

nationwide and taxed in formal currency, promote domestic production, increase

economic efficiency and reduce financial leakage from local economies.

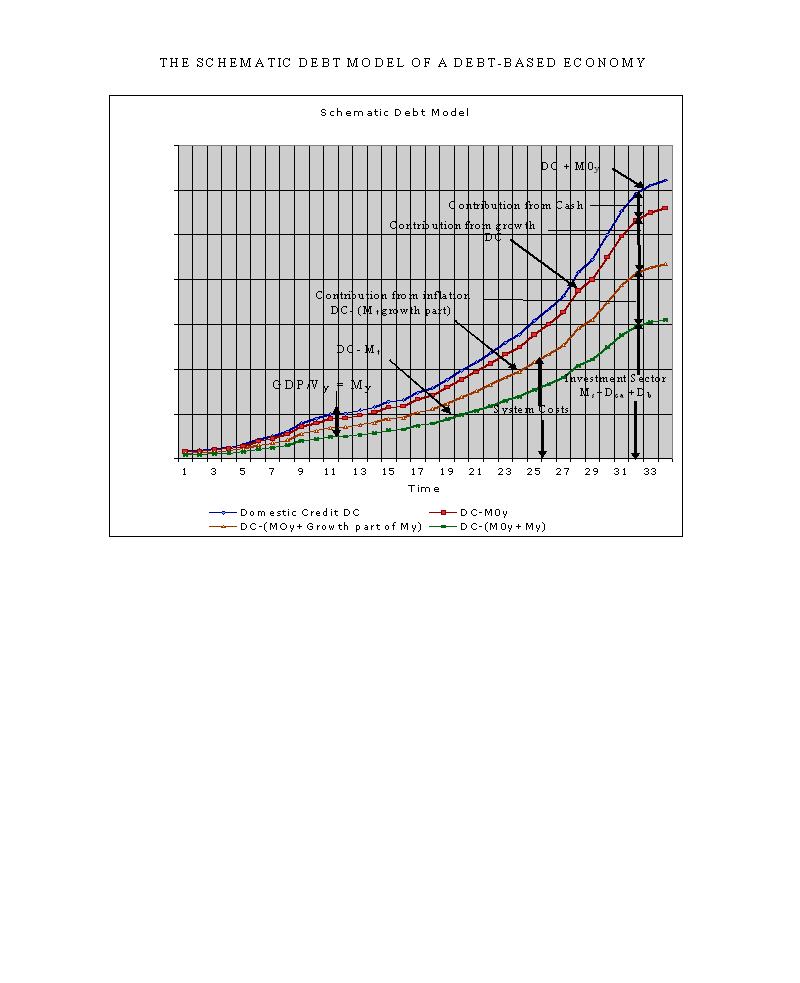

Appendix : The Debt Model based on a revision of the Fisher Equation.

Click here to see a visual form of the debt model.

The debt-based economy can be

expressed as a simple variation of the original Fisher Equation of Exchange:

GDP (Total economic output measured

as gross domestic product PQ, being the quantity Q of goods and services

produced times their price level P) = Vy ( the speed of circulation

of My) times My (the transaction deposits actually used

to generate PQ)

in the

form:

GDP = Vy *(DC

- (Ms +Dca +Db ) + M0y )

Where My

= GDP/Vy = DC - (Ms +Dca + Db) + M0y and:

My = The

deposits actually used to generate productive output and My = Mt + M0y where Mt

is the transaction deposits representing

productive debt Dt,

and M0y = The residual cash

in circulation included in My that is used to contribute to

productive output,

Dca = The whole of the debt created in the

domestic banking system to satisfy the accumulated current account deficit 1.

Ms =

The net after tax accumulated deposits arising from unearned deposit income on

the total domestic banking system deposits M3 (excluding repos) 2.

DC = Domestic Credit,

Ds = the residual needed to satisfy the

equation DC = Dt + Dca3 + Ds and the debt Dt is numerically equal to the

Db =

The “bubble” debt, the excess credit

expansion or contraction in the banking system such that Ds - Db = the debt supporting the accumulated deposit interest Ms

defined above. Db can be

positive or negative”.

The debt model can be expressed and

used in its differential form to quantify macroeconomic outcomes over any

chosen time period.

1. This is greater than the monetary deposits Mca

because the banking system may have sold commercial paper to borrow foreign

currency to satisfy the foreign exchange settlement requirements.

2. Repos refer to inter-institutional lending

3. Arguably the accumulated sum of capital transfers

could be included here, in which case the net international investment position

(NIIP) would be used instead of the accumulated current account. The decision

affects the size of the “residual” Db.

"Money is not the key that opens the gates of the market but the

bolt that bars them."

Gesell, Silvio, The Natural Economic Order, revised English edition, Peter

Owen,

![]()

This work is

licensed under a Creative Commons

Attribution-Non-commercial Share-Alike 3.0 Licence.