NGO Another Way (Stichting Bakens Verzet), 1018

AM

SELF-FINANCING, ECOLOGICAL,

SUSTAINABLE, LOCAL INTEGRATED DEVELOPMENT PROJECTS FOR THE WORLD’S POOR.

|

FREE E-COURSE FOR DIPLOMA IN INTEGRATED DEVELOPMENT |

|||||

Edition 01: 09 May, 2013.

(VERSION EN FRANÇAIS PAS DISPONIBLE)

Summaries of monetary reform

papers by L.F. Manning published at http://www.integrateddevelopment.org

The

referenced papers :

00. Summary of papers published.

01. Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

02. How to create stable financial systems in four

complementary steps.

03. How to introduce an e-money financed virtual minimum

wage system in New Zealand.

04. How to introduce a

guaranteed minimum income in New Zealand.

05. The interest-bearing debt system and its economic

impacts.

07. The DNA of the debt-based economy.

08. Manifesto of the debt-based economy.

09. Unified text of the manifesto of the debt-based

economy.

10. Using a foreign transactions surcharge (FTS) to manage

the exchange rate.

11. The Manning plan for permanent debt reduction in the national

economy.

12. Comments on the (Jaromir Benes and Michael Kumhof) Chicago Plan Revisited Paper.

13. Missing links between

growth, saving, deposits and GDP.

COMMENTS ON

COMMENTS BY :

Sustento Institute,

EXECUTIVE

SUMMARY.

On balance it is

probably preferable to work directly with official statistics such as those

provided by the Reserve Bank of

Selecting data

tends to create a reporting bias.

The NZI paper

extends to 70 pages without providing an adequate visual overview of

The NZI report is

disjointed and hard to follow. It poorly illustrates the methodological

differences in the various data series.

NZI Figure 1 purportedly “shows

the best available estimates of the total international liabilities.....”

when the official national accounts data produced by Statistics New Zealand

(SNZ) plotted as Figure 2 below are readily available on line. The SNZ balance

sheet (BS) data apparently gives debt figures 9.2% higher than SNZ Balance of

Payments (BoP) data [NZI p. 4 RHS top]. The NZI use of the BoP data instead of

the BS data needs to be fully justified, while stock based figures that

include revaluations (as in NZI Table 1) may be useful but are not immediately

relevant to the nation’s current external debt position.

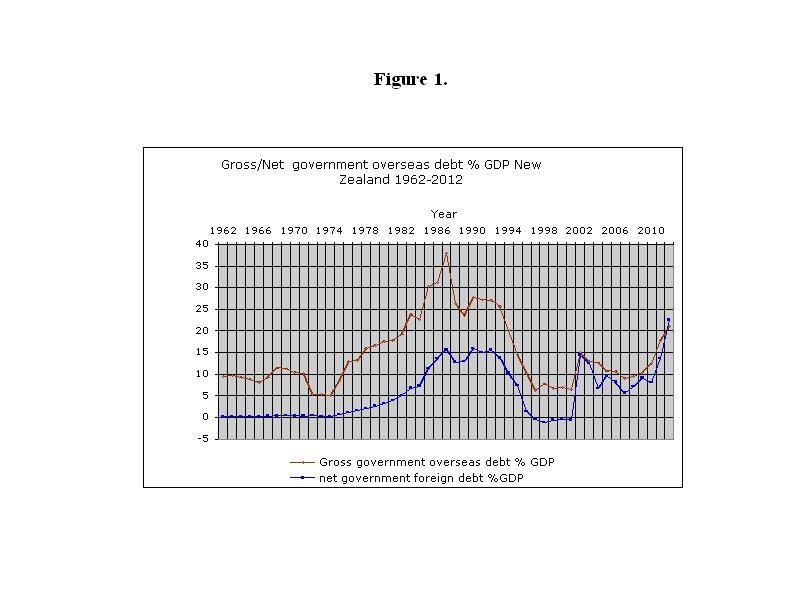

Figure 1 Gross/Net New Zealand Government Debt as % of GDP.

{kind=link}

NB

The apparent discontinuity in 2001/2002 in Figure 1 could be related to the

fallout from the 9th September 2001 attacks in the

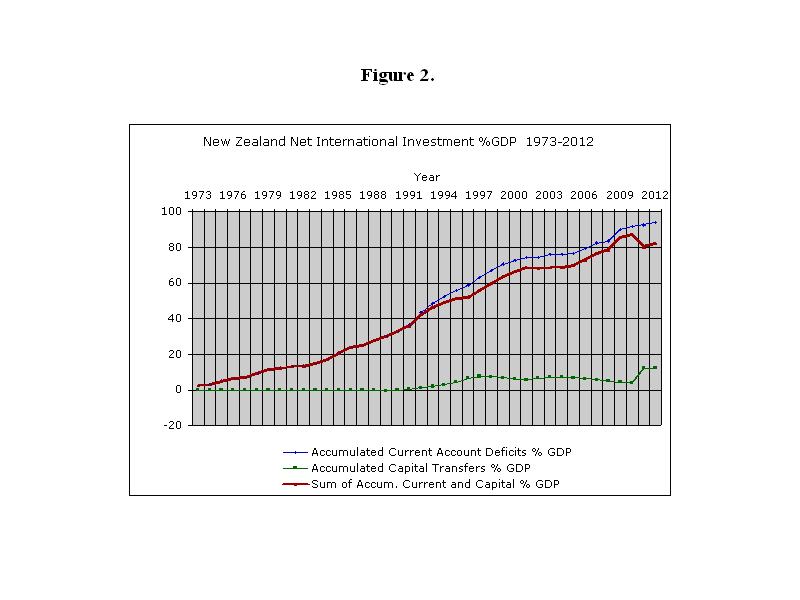

Figure 2 New Zealand Accumulated Net International Investment as % of

GDP.

{kind=link}

Source:

COMMENTS

ON PRELIMINARY PAGES OF NZI PAPER.

P. v : Foreword.

Free trade has to

be bounded so as to avoid large scale current account imbalances, but it is

not. One can have free capital flow but not asymmetrical capital flows. When

the outcomes are asymmetrical, trade and capital mobility do not constitute “a mechanism that creates prosperity for all”

as NZI claim, because the additional wealth the economy creates is being

drained offshore through foreign ownership of the economy.

P. vi : Import of

capital.

The NZI paper shows

“

The single key

event was when US President Nixon abandoned the US$ gold peg on August 15th

1971. The asymmetry in the world financial system could not have arisen were

the peg still in place because asymmetrical events would have forced

stabilising currency de(re)valuations. The more recent “floating” exchange

rates do not work in the face of unbridled speculative capital flows.

P. xiii : Key messages.

Key message 1.

In the early days

of

Key message 2.

The oil shocks did

result in current account deficits and consequential investment inflows. They were

not sterilised and resulted in increasing net overseas debt. The oil shocks

could not have happened prior to the abandonment of the

Key message 3.

The current account

problems have little to do with the 1970’s per se and everything to do with

over consumption (including that resulting form the oil shocks) and the “free

trade” policies the NZI paper appears to be promoting. Keynes argued in favour

of “balanced trade” at Bretton Woods in 1944 and was vetoed by the

Key message 4.

The NZI text is

wrong. The way to fix the investment and debt problems is to manage the

exchange rate and rebalance the broad balance of payments so New Zealanders can

buy back their country and enable other countries can do the same. That will

not be possible unless effective policy tools are implemented (like the

author’s proposed foreign transactions surcharge

(FTS)- the details of which can be found at www.integrateddevelopment.org ).

P. xiv : Myths about

International Debt and FDI.

Myth 1 : NIIP is negative

because domestic investment since 1973 has exceeded national savings.

Contrary to what

the NZI paper says, the causality is the current account deficit itself. The

“borrow and hope” program was indeed funded by foreign borrowing, and the

“think big” projects did involve foreign components and foreign companies.

Despite that, as shown in Figure 1 above, the external government debt to GDP

ratio rose faster before and after “think big” due to the 1970’s oil

shocks and the Labour government’s free for all in the mid 1980’s. Moreover,

external government debt was reduced (at huge public cost) to very low levels

through the 1990’s until the recent debt crisis began. The negative NIIP was

exacerbated by the deficits on international investment income caused by

increasing foreign ownership of the NZ economy, including the banks. The NZI

text (top left p. xv) is true in part, but it is not the government that is

borrowing abroad to fund fiscal deficits. The government has recently borrowed

abroad because it is cheaper to do that than borrow from the domestic banks.

The relatively high domestic interest rates are due to foreign ownership

draining the NZ economy. To be certain of this, the data in Figure 1 replicates

the gross and net government debt data for the 50 years ending 2012. The NZI

paper fails to show the (more appropriate) net government external debt

position. Net government debt as a % of GDP has never been excessive and

funding it, while substantial, makes up less than 15% of the present current

account deficit.

Myth 2 : NZ ‘s large negative NIIP arises because

since the mid 1970’s ‘we’ have been spending more than we earn.

The NZI argument is

misleading. It says that because the Balance of Trade has been in surplus

neither business nor the public is responsible for the deficits. Somehow that

means according to NZI that “ [b]y

definition, gross domestic spending on goods and services was less than gross

domestic production....”. This neglects all other spending on foreign goods

and repatriation of profits and interest and so on that are part of the current

account. The myth is absolutely true.

Myth 3 : NZ has a large

negative NIIP because New Zealanders are poor savers.

The NZI argument about myth 3

is also misleading. NZI says “national

saving has been positive for 38 out of the 41 years between 1972 and

“Saving rates in

In orthodox terms, New

Zealanders are relatively poor “savers”.

The issue is whether that poor saving affects NIIP.

There are always

“savings” because total productive incomes include those arising from new

capital development. Conceptually those incomes are “saved” and used to

purchase the capital items the economy produces. In practice, in the debt based

financial system, most capital items are funded by new bank debt. Most

“savings” from gross household and business incomes migrate instead to the

non-productive investment sector (equities, property, bonds and the like and

household debt servicing, especially to pay the unearned income on banks

deposits), or to pay for excess expenditure on the current account. The

accumulated current account deficit, which in

Myth 4 : NZ’s large negative

NIIP is due to the private sector.

This is not a myth

either. NIIP, primarily reflecting the accumulated current account deficit,

results from foreign ownership of the economy and the failure to bring the

current account and exchange rate under control. This is due to free market,

free capital flows, and so on. Foreign ownership has grown because NZ has lived

beyond its means while not fixing its current account problem.

“The sharp rises in the NIIP from 1974 to the

mid 1980’s was associated with heavy government net overseas borrowing”.

That is partly true as long as the word “associated” is not treated as being

the cause of the debt. The data appendix (AS 25) supplied by NZI starts from

2001. Myth 1 above and Figure 1 clearly show that net government external

borrowing was reduced to zero by March 1996.

On the other hand

there is a convincing argument that government debt is caused largely by the

periodic reductions in private sector tax rates. For the time being it have been

cheaper for the government to borrow abroad than to sell bonds to the domestic

banks or other institutions. This is why the banks themselves are borrowing

abroad now! The main point is that now, under a National led austerity

government, the private sector (households and businesses) is by far the main

driver of the NIIP, with the possible exception of the 2011 and 2012 years.

The NZI statement

(top p. xvi) “that the high NIIP today is a legacy of the policies and events of the

1974-1984 period” is untrue as a glance at Figures 1 and 2 above demonstrates. The net government

overseas debt was zero from mid 1990’s to 2001 through both national and labour

governments. In 1991 the

Myth 5 :

The text may be

referring to private NIIP debt. If so, NZI is implying that it doesn’t matter

if NZ is foreign owned, though it may be true that NZ “borrowers [have been] borrowing

unwisely – for the last 25 years” as NZI say. The NZI text then supports

the banks’ offshore borrowing!

Apparently they cannot be borrowing unwisely “given the intensity of the scrutiny they face”. The truth is

apparent. The banks borrow abroad for one reason: they profit from it because their offshore

borrowing costs are less than onshore deposit interest. There is no net

liability to the banks because they hold the equivalent NZ domestic exchange in

reserve. So contrary to the NZI text there is no moral hazard in the banks’

arbitraging as long as they have reasonable currency hedging in place.

Myth 6: NZ’s large negative

NIIP is due to banks borrowing to fund new housing.

That is a myth as

NZI claims. The accumulated current account deficit is due to NZ spending too

much and giving away ownership of its resources. The current account is funded

in the first instance by domestic debt. Once foreigners are paid, the

corresponding deposits return to NZ to buy whatever the foreigners want. The

sale of those assets leaves deposits in the hands of the domestic sellers. Most

of that money goes into inflating the non-productive investment sector,

including housing.

The NIIP is due

mainly to the current account deficit, not funding new housing. The investment

sector inflation is a consequence of the current account deficit, not its

cause.

Myth 7 : Attaining a fiscal

surplus 2014-15 will start reducing the current account deficit.

This is not a myth. A fiscal

surplus (that is : a theoretical ability to repay government overseas debt)

could enable the government to pay down its net foreign debt (Figure 1 above).

That would improve the net NIIP position. The repayment will not affect the

current account much because the government borrowing is a capital transaction.

These days, government debt is not typically used to pay for foreign goods and

services. It is, instead, used to pay for domestic goods and services and

transfer payments. Only the interest on the government foreign debt appears in

the current account. A reduction in the interest payments will reduce the current account deficit a little, though only a

pittance – a reduction of NZ$ 2b. in the capital account at 3% would improve

the current account by, say, NZ$ 60m. out of a current account deficit of some

NZ$ 10b.

Myth 8: Asians are

increasingly taking over NZ.

This is not a myth

either. While it’s true the vast bulk of Foreign Direct Investment (FDI) is not Asian,

NZI itself says Asian FDI is increasing. The free trade deal with

Myth 9 : NZ companies are not

investing offshore; NZ is open to takeover but it isn’t two-way.

There is an element

of truth in what the NZI text says but it is still misleading. Their Figure 3

shows inwards FDI “stock” at almost

50% of GDP and outwards “stock” at just over 10% of GDP (NZI Figure 3 p. xxiv).

The stock measures include revaluations that are internal balance sheet items

rather than cash-flow items. The NZI text therefore needs to be treated with

caution.

Myth 10:

This is definitely

a myth. The important point is that FDI should be limited to what serves the NZ

economy. Until now NZ has just been selling its economy.

Myth 11: Passive investment is

less useful than direct investment.

This is not a myth,

but neither is it especially relevant. NZI says “Foreign portfolio investment helps reduce the cost of capital in

Myth 12 : New Zealanders are

becoming tenants in their own country because of growing foreign ownership.

The NZI text is

utterly and deliberately misleading on this point because it refers only to

land. The economy is not land. It reflects the ownership

of the means of production. New Zealand’s productive capacity is already more

than 60% foreign owned where foreign ownership is measured as the accumulated

current account deficit/value of capital investment at cost. NIIP could also be

used. If the outstanding capital investment principal is used instead of

capital investment at cost, the extent of foreign ownership is even higher.

Since GDP= the outstanding capital investment principal as set out in the “DNA of the debt-based economy” by the author at website www.integrateddevelopment.org, monetised

production is dependent on the outstanding investment capital, not on the

unrealised value of land and property assets.

NZI discusses other

methodologies for assessing % foreign ownership in Section 2 of the main

document. Land (agriculture) contributes a relatively small portion to NZ GDP

despite its critical importance. The numbers for it are in the NZ national

accounts. In the

PP xix-xx : Key points : NIIP and indebtedness.

The NIIP numbers

NZI uses are misleading in part because they are distorted by more than NZ$ 16

billion capital inflows relating to the

The difficulty here

is that re-creating the status quo ante is called “investment” when it is

really more like maintenance and repair because the net value of NZ assets does

not increase as a result. At best they return to what was before the earthquakes. Moreover the BoP Manual 5 rules specify

that the whole insurance inflow from the

Perhaps that is why

NZI doesn’t mention the figures for the intermediate years in their text,

though they can be traced in table AS 25. Without that specific one-off NZ

$16b. “capital inflow”, the NIIP numbers would be at least 10% higher than

those shown in the NZI text.

When that 10%

correction is made together with the 9.2% from using the BoP method instead of

the BS method, the real NZ international debt equals the accumulated current

account deficit (94% of GDP in 2012) less a small deduction of about 4% for the

residual accumulated capital inflows, or about 90% of GDP.

The future path for

NIIP is not primarily “a function of the

earnings rate paid on the NIIP relative to the GDP growth rate” as NZI

claims. It is mainly a function of persistent current account (CA) deficits. By

inference, NZI seems to think it is fine if all the GDP growth leaves the

country in the form of those CA deficits. The nation as a whole is then left

the impossible task of sustaining the increasing drain of wealth into foreign

hands.

As described for

the “myths” above, the statement that “these

[NIIP] statistics indicate today’s highly negative NIIP is largely a legacy of

the prolonged deficit spending between 1976 and

P. xxi-xxii. Key Points :

Foreign Direct Investment.

The numbers offered

by NZI are largely meaningless when the official accumulated current account

deficit can be used as shown in Figure 2 above which is arguably more accurate,

especially over the earlier period.

The BoP manual and

commentary on it show that is has always been difficult to split current flows

from capital flows. In most countries the separation was not made at all for

most of the period 1962-2012.

No evidence is

provided for the statement that “the OECD

now considers

MAIN

DOCUMENT.

1. Introduction.

If NZ’s high “net external indebtedness has long troubled

policy makers and rating agencies alike” (p.1 RHS bottom) one would have

thought they would have something done about it, such as the author’s proposed foreign transactions surcharge

(FTS) information on which is available at www.integrateddevelopment.org.

2. Notes on key concepts and

relationships.

2.1 Terminological

distinctions and issues.

The NZI text [p. 4

RHS top] refers to SNZ Table AS 36 but

it doesn’t appear to be in the appendix. The table says the “estimated asset and liability positions are

higher for the BS [Balance Sheet] presentation by 9.2% of GDP on average [than

they are for the Balance of payments figures]”.

2.1.3 Derivatives.

SNZ measures of international

borrowing and lending include derivatives while the IMF measures of external

debt do not.

2.1.4 Overseas debt.

SNZ figures for

banks’ overseas debt are larger than Reserve Bank of New Zealand (RBNZ) figures

because SNZ follows IMF BPM5 that includes banks and other financial

institutions.

2.1.6 IIP measures.

SNZ/IIP stock based measures

rely on surveys. They can’t just be worked out from flow measures.

2.2 Key identities.

2.2.1 IIP Stock flow dynamics :

Closing

stock of investment = opening stock of

investment + Foreign investment over the intervening period + Valuation changes

during that period.

The stock number is

about “value” not debt. That means it is difficult to get a foreign debt figure

from a stock figure because valuation changes such as exchange rate changes,

financial derivatives valuation changes, market price changes, and “other

valuation” changes are unrealised. Nor is it clear whether those changes are

net of depreciation/ debt repayment.

NZI itself writes “If

the second and third items [of those mentioned above] have only a small effect,

the net investment flow will closely approximate the current account deficit

(or surplus) in the BoP.”

That is one reason why

the author of this paper uses the accumulated current account data as a first

approximation in his work. This is confirmed at NZI Table 4 p. 12 where the

current account deficit is funded by the net capital account inflow plus net

foreign investment inflow as used in Figure 2 above.

“Change in stock of investment as % of GDP=

(residual net investment flows plus valuation changes) as a % of GDP during the

intervening period plus (opening stock as a % of GDP for the same period times

the difference between the earnings rate and the rate of growth of GDP divided

by the proportionate growth rate of GDP)”. [sic?]

The calculations and text

giving rise to NZI Table 2 (p. 11) look dubious and there is a big typo error

bottom right of the table where the NZI text p.12 LHS top gives 72.1% not 62.9%.

2.2.3 Two identities linking the BoP to the

national income accounts.

That is dealt with

at great length in my paper on the “Savings

Myth” available at www.integrateddevelopment.org

which among other things shows that the use of capital consumption

(depreciation) as in NZI Table 5 is incorrect. Depreciation is a tax variable

not a value variable so it cannot satisfy the

BS stock-flow dynamics. [2.2.1 above].

3, Overview of the latest

statistics.

3.5 Degree to which NZ assets

are now overseas funded.

This is misleading.

The test is not the “capital stock including land and residential buildings”

but the country’s productive economy. A completely different result is obtained

if the ratio of the accumulated CA deficit to capital investment at cost shown

in the National Accounts is used. That ratio shows more than 60% foreign ownership

compared with 12% claimed by NZI (p. 26 LHS bottom). NZI then gives various

other flow “comparisons” such as (p. 26 RHS bottom) comparing “total income

paid overseas” NZ$ 14.9 billion to “operating surplus net of capital

consumption” NZ$ 57.2 billion giving 26% foreign ownership. It is not valid to

compare a net tax paid payment with a gross operating surplus because that

defies all basic accounting principles. Therefore, NZI Table 8 needs to be

taken with a grain of salt because none of the numbers appears to

reflect the true status of foreign ownership.

4. Comment on the historical

record pp. 30-45.

4.1 Nineteenth century.

Interesting but not relevant

to today.

4.2 Early twentieth century.

Ditto. Blanket foreign exchange

and import controls imposed in 1938 (Reserve Bank formation, Labour government)

changed the debt profile.

4.3 1950-mid 1980’s The

protectionist years.

The following quote

gives the flavour of the text: (p40) “It

was not important if the costs to NZ consumers were very high because

successive governments made sure consumers had little or no choice”.

The foreign

ownership of NZ business and assets resulting from free trade hardly offers a

better choice. Moreover, any claimed positive effects of the “choice” are short

lived as is now apparent from the progressive loss of real purchasing power

arising from foreign indebtedness. Nash (as expressed in the text at the bottom

of NZI p. 40) was probably closer to the truth.

Current account

deficits used to be limited through the application of the

Section 4.3.3 1970’mid 1980’s-

Big Deficits - is about escalating debt.

This is the “spend,

borrow and hope” period discussed in the preceding pages of these notes. NZI

forgets to mention that almost the whole world went through the oil shocks and

the huge deficits and inflation they created. That’s where the sea of

petrodollars came from! What does NZI think that little NZ should have done?

Of course imports

exceeded exports for most of this period

“

The NZI figures

bear no relationship to the figures in Figure 2 of this paper. Figure 2 is based on the official national accounts

and shows that the increase slowed after the oil shocks. It rose again later

under both Labour and National governments. As previously stated, the primary

reason for that was the deregulation and globalisation that followed after the

4.4 1985-95 Fiscal

Consolidation and Liberalisation.

The COST of the

liberalisation has been the sale of

Much of the text p.

43 RHS relating to the benefits of selling off State assets is false. Yes, the government foreign debt was reduced.

That was not achieved from the asset sales but from the vicious austerity

imposed on most of the public. Moreover, as the text itself acknowledges NZI

RHS p. 44: “Selling assets such as ... to overseas investors and using the proceeds

to reduce foreign currency denominated government debt does not alter the net

external liability but it does change its composition”.

The ideological

bias of the NZI document is there in Orwellian terms for all to see. That

ideology is why we have such an escalating current account problem today due to

the vast asymmetry between inwards and outwards flows.

4.5 Post 1995-2012 : The Mixed

Member Proportional Representation (MMP) era.

According to NZI NZ

has somehow “lost competitiveness” because of MMP! NZI blames MMP for the post 2009 fiscal

deficits – as if NZ created the world debt crisis. In fact, the recession in NZ

was 100% self-inflicted. Banks directly caused the recession by failing to pass

on Reserve Bank interest rate cuts in favour of boosting their loss reserves,

thereby squeezing credit. NZI does, however, highlight the risk of increases in

external liability (bottom RHS p. 44).

END

OF FILE

THE REFERENCED PAPERS

The

referenced papers :

00. Summary of papers published.

01. Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

02. How to create stable financial systems in four

complementary steps.

03. How to introduce an e-money financed virtual minimum

wage system in New Zealand.

04. How to introduce a

guaranteed minimum income in New Zealand.

05. The interest-bearing debt system and its economic

impacts.

07. The DNA of the debt-based economy.

08. Manifesto of the debt-based economy.

09. Unified text of the manifesto of the debt-based

economy.

10. Using a foreign transactions surcharge (FTS) to manage

the exchange rate.

11. The Manning plan for permanent debt reduction in the national

economy.

12. Comments on the (Jaromir Benes and Michael Kumhof) Chicago Plan Revisited

Paper.

13. Missing links between

growth, saving, deposits and GDP.

Return to : Bakens Verzet

Homepage

"Money is not the

key that opens the gates of the market but the bolt that bars them."

Gesell, Silvio, The

Natural Economic Order, revised English edition, Peter Owen,

This work is licensed

under a Creative

Commons Attribution-Non-commercial Share-Alike 3.0 Licence.