NGO Another Way (Stichting

Bakens Verzet), 1018 AM

SELF-FINANCING, ECOLOGICAL,

SUSTAINABLE, LOCAL INTEGRATED DEVELOPMENT PROJECTS FOR THE WORLD’S POOR.

|

FREE E-COURSE FOR DIPLOMA IN INTEGRATED DEVELOPMENT |

|||||

Edition 01: 09 May, 2013.

(VERSION EN FRANÇAIS PAS DISPONIBLE)

Summaries of monetary reform

papers by L.F. Manning published at http://www.integrateddevelopment.org

The

referenced papers :

00. Summary of papers published.

01. Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

02. How to create stable financial systems in four

complementary steps.

03. How to introduce an e-money financed virtual minimum

wage system in New Zealand.

04. How to introduce a

guaranteed minimum income in New Zealand.

05. The interest-bearing debt system and its economic

impacts.

07. The DNA of the debt-based economy.

08. Manifesto of the debt-based economy.

09. Unified text of the manifesto of the debt-based

economy.

10. Using a foreign transactions surcharge (FTS) to manage the exchange rate.

11. The Manning plan for permanent debt reduction in the national

economy.

12. Comments on the (Jaromir

Benes and Michael Kumhof) Chicago Plan Revisited

Paper.

13. Missing links between

growth, saving, deposits and GDP.

15. Measuring Nothing on the Road to Nowhere.

16. Debt bubbles cannot be popped : Business cycles

are policy inventions.

THE

By

Sustento Institute,

29th April, 2013.

CONTENTS.

EXECUTIVE SUMMARY.

BACKGROUND OF CPRII.

CPRII DOES NOT RESOLVE

DEBT AND INFLATION ISSUES.

THE SIX CLAIMED ADVANTAGES OF

THE PROPOSAL :

(a) REDUCTION OF GOVERNMENT

DEBT & INTEREST BURDEN.

(b) MUCH BETTER CONTROL OF

CREDIT CYCLES.

(c) REDUCTION IN PRIVATE DEBT.

(d) ELIMINATION OF BANK RUNS.

(e) A LONG TERM INCREASE IN

OUTPUT OF 10%.

(f) THERE IS NO LIQUIDITY TRAP

......

CONCLUSION.

EXECUTIVE SUMMARY.

This paper is a

response to the IMF Working Paper WP/12/202 “The Chicago Plan Revisited” by Jaromir Benes and Michael Kumhof

(BK), and more particularly to the revised draft of that paper released on 12th February 2013 (CPRII).

The CPRII paper models the Chicago Plan (CP) proposals. The CP

proposals date from the 1930’s and grew out of concern that the current

debt-based financial system is inherently unstable. That view has been

reinforced by the instability leading up to the recent debt crisis and, more

recently, large scale Quantitative Easing and Eurozone

debt problems. The CP has always been supported by many of the world’s leading

economists. Many of its main provisions have formed the basis of monetary

reform movements for almost a century.

CPRII uses Dynamic

Stochastic General Equilibrium (DSGE) modelling to

study six main claims made for the Chicago Plan:

(a) Reduction of government debt and the interest

burden it creates.

(b) Much better control of credit cycles

(c) Reduction in private debt

(d) Elimination of bank runs

(e) A long term [relative] increase in [GDP]

output of 10%

(f) There is no liquidity trap, so that “steady

state inflation” can drop to zero.

BK find strong

support for all six of the claims they make for CPRII.

This paper shows that many of

the claims are unfounded because the CP itself is insufficiently robust to work

properly as it is presented and modelled. It would work if it were slightly

revised along the lines of the Manning plan for permanent debt

reduction in the national economy available at website www.integrateddevelopment.org.

It is likely that a more robust form of the CP would demonstrate outcomes

vastly superior to those obtained by BK in their

modelling.

The present

structure of the CP retains the functional elements of the existing financial

system except that Savings and Loan debt replaces Bank debt. Apart from

government spending, it leaves the private financial institutions in full

control of money allocation and credit. The large financial institutions and

business are the primary beneficiaries from the CP as it presented. The asymmetrical

imbalances in debt, income and wealth aggregation remain unresolved.

The “People’s” money advocated

by CPRII needs to be made available and used by the

people, for the people, rather than by the banks for the banks. Otherwise the

Chicago Plan reforms cannot be a sufficient response to financial system

failure.

BACKGROUND OF CPRII.

Unless otherwise indicated,

all page references in this paper are to CPRII.

The BK paper has received a lot of attention around the world.

Much of it has been favourable. CPRII gives the

history of the CP at p. 28-29. The plan originated with Frederick Soddy in

1926. Professor Frank Knight (

The key feature of

the CP “was to call for the separation of

the monetary and credit functions of the banking system, first by ensuring 100%

backing of deposits by government-issued money, and second by ensuring that the

financing of new credit can only take place through earnings that have been

retained in the form of government issued money, or through the borrowing of

existing government-issued money from non-banks, but not through the creation

of new deposit money, ex nihilo, by financial institutions”. [p. 4]

For the productive

economy this is tantamount to a verbal restatement of the basic tenet of orthodox

economics, seen in almost every economics text published prior to 1980, that

Savings=Investment where investment is defined as new productive capital investment.

For the non-productive economy, the

non-productive “investment sector”, it is a clear statement that credit for the

purchase and exchange of existing capital goods must take place through the

on-lending of deposits as a “savings and loan” (S&L)

function. That on-lending creates secondary debt and increases the speed of

circulation of the financial system monetary deposits. The S&L

function is the opposite of funding the purchase and exchange of existing

capital goods through the creation of new interest-bearing bank debt and its

corresponding deposits that have become the norm over the past thirty

years. The differences between a

financial system based on savings and loan and one based on increasing bank

debt are explored in detail in a paper by the author Capital is debt published at www.integrateddevelopment.org.

CPRII DOES

NOT RESOLVE DEBT AND INFLATION ISSUES.

The current system

creates bank debt and maintains a low speed of circulation of the total

financial system deposits. Bank debt is typically cheaper than secondary debt

borrowed from non-bank institutions. In most industrialised countries there is

a reasonably close relationship between domestic credit and total debt defined

as domestic credit plus non-bank secondary credit but not between debt and

capital investment. One exception is the

That balance is much less than

the total debt.

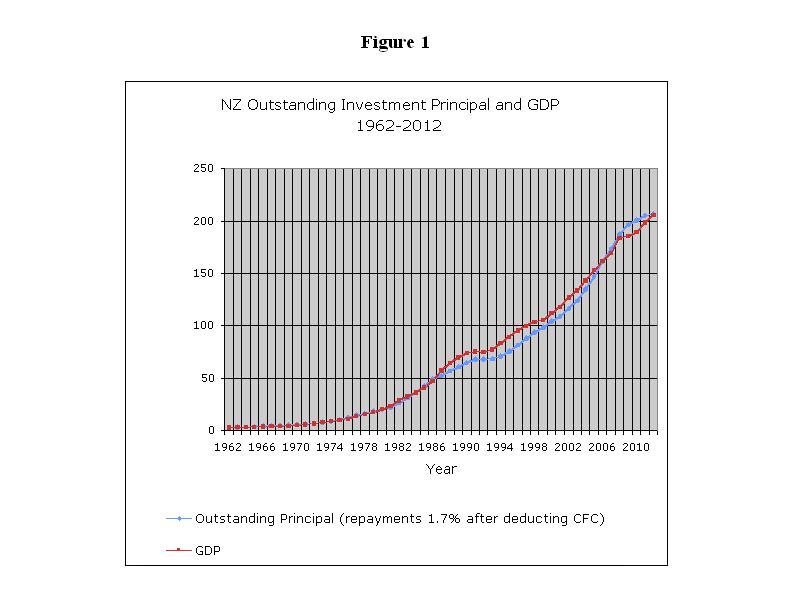

FIGURE 1 : OUTSTANDING INVESTMENT PRINCIPAL AND

GDP NEW ZEALAND 1962-2012.

{kind=link}

The outstanding

principal in Figure 1 has been calculated empirically. Figures 1 and 2 are

based on adding the net annual capital formation in any year to the cumulative

outstanding principal from the previous year and multiplying by 0.983. The

calibration “works” because the depreciation (consumption of fixed capital

“CFC”) shown in the national accounts is higher than the true loss of value.

The distorted tax business depreciation figures included in today’s tax laws

mask a large portion of the principal repayments. The GDP, Gross Capital

Formation and Consumption of Fixed Capital used for the graphs are taken

directly from the NZ National Accounts. It should be noted there are

substantial differences between the latest published series downloaded from www.stats.govt.nz on 15 April 2013

and the data published in the various earlier official data. This contrasts

sharply with the CPRII modelling under heading I [p.

44], where the depreciation rate rather than outstanding capital is used to

assess capital accumulation.

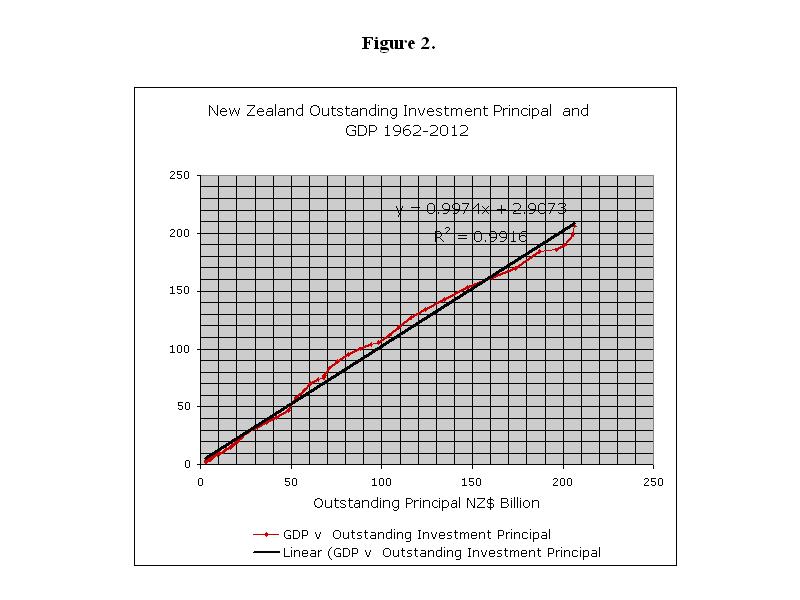

FIGURE 2 : OUTSTANDING INVESTMENT PRINCIPAL v.

GDP NEW ZEALAND 1962-2012.

{kind=link}

Principal

repayments are not “constant” over time as assumed, for simplicity, in the

figures. There could, for example, be changes in tax depreciation rules (such

as the recent removal of tax depreciation from residential housing investment

in

Contrary to the

modelling assumptions made by BK in CPRII there is no equilibrium in the investment sector

whatever stochastic shocks are applied in the modelling process. Instead,

economic performance (Figures 1 and 2) is specifically related to new capital

investment including new investment in non-productive assets on a 1:1 basis

whereas the money supply shown in Figures 3 and 4 is not.

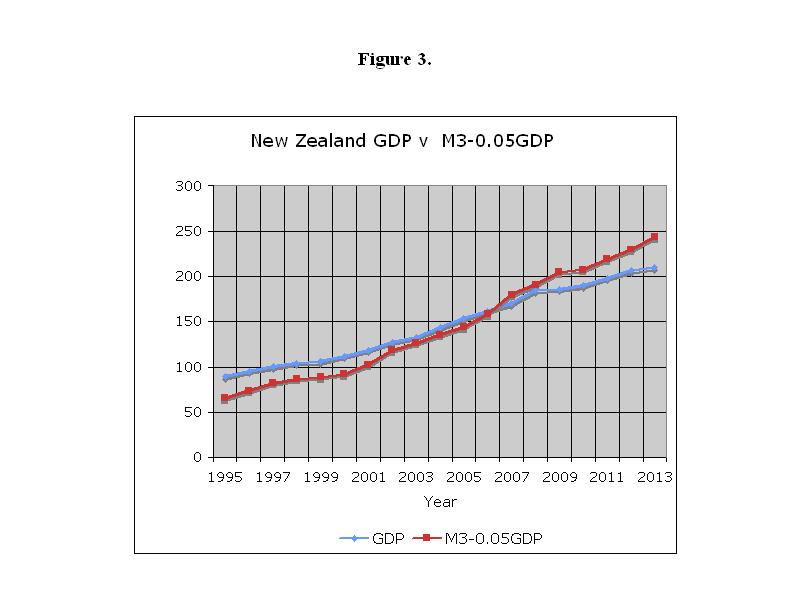

FIGURE 3 : GDP AND (M3-0.05 GDP) FOR NEW ZEALAND

1996-2013.

{kind=link}

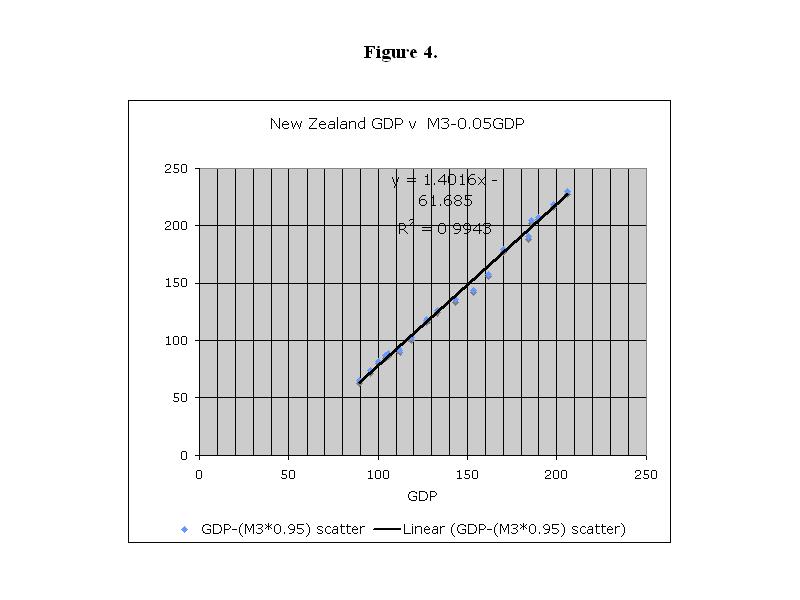

FIGURE 4 : GDP v M3-0.05 GDP NEW ZEALAND

1995-2013.

{kind=link}

While business

investment decisions rely on generating enough extra income to pay interest and

repay principal, debt servicing of non-productive investments like residential

housing is more difficult. Borrowers must typically decrease their consumption

or rely upon uncertain future income expectations. As long as the share of

productivity gains in the productive economy paid as incomes to income earners

(over and above what is needed by business to service its own productive

capital investment) is less than their debt servicing costs, it is

theoretically impossible to fund those costs out of the productive economy. The

reason is simple: Saving within the economy is used up to purchase new capital

investment (including new housing) as shown in Figures 1 and 2. Otherwise the

economy cannot grow and the market cannot clear all the goods and services it

produces.

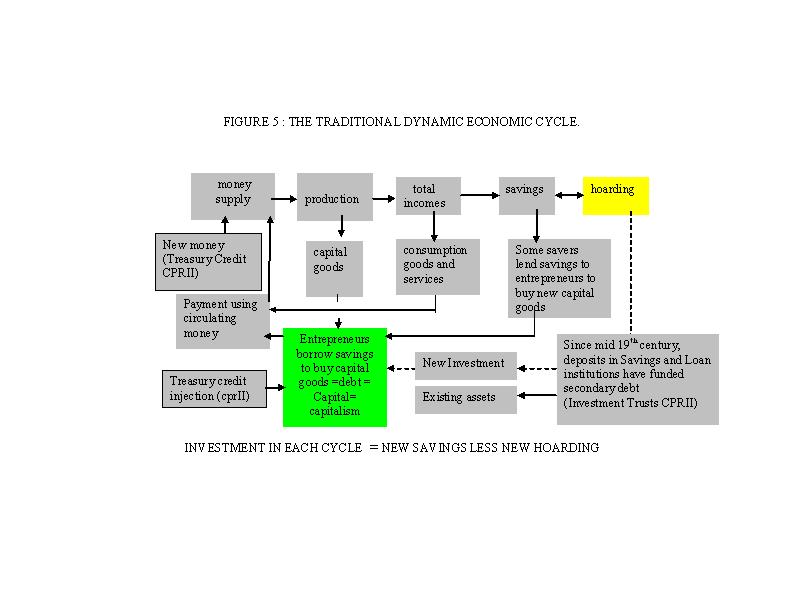

Figure 5 shows the basic

dynamic flows in a simple economy.

Figure 5 is broadly

similar to the structure proposed by CPRII. The money

supply (top left) is increased using government-issued debt-free money as the

productive capacity of the economy increases. Incomes equal to the value of new

capital investment are saved and then on-loaned to entrepreneurs. Some Savings

have traditionally been hoarded as shown at the upper right of Figure 5. When

hoarding increases, not enough savings are being recycled to clear the market

of capital and consumption goods and pay the non-productive debt servicing

costs. Either more money must then be injected into the system, the Treasury

credit in CPRII, or the S & L funds (The CPRII “Investment Trust” funds) have to be recycled faster.

In addition, the existing debt base must, as a minimum, be maintained to avoid

a collapse in existing asset prices. For that to happen, the secondary

(Investment Trust) debt and Treasury credit must together be at least as large

as the present debt base less transaction account balances and government

capital assets. The aggregate interest paid on that debt is likely to be as

much as it is now. The more interest there is the faster the money supply will

have to grow to keep pace with the purchase and exchange of non-productive

assets and provide for systemic inflation.

FIGURE 5 : THE TRADITIONAL DYNAMIC ECONOMIC

CYCLE.

{kind=link}

In figure 5 the investment in

each cycle = new savings less new hoarding.

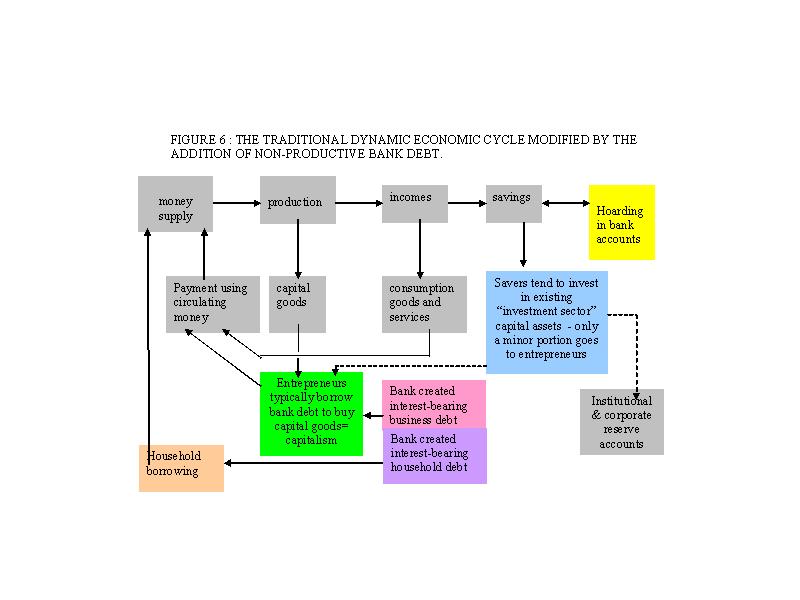

Figure 6 represents

the existing debt-based financial system where savings are decoupled from the

productive economic cycle by bank intermediation. As BK

say in CPRII, bank lending depends only on the banks’

willingness to lend and the customers’ willingness to borrow. This is the

concept of “endogenous” credit so widely discussed among economists today.

Among the screeds of jargon and complex mathematical modelling, the simple

truth remains that if savings can be recycled for profit as in Figure 5, they

will be. If interest-bearing debt can be created for profit as in Figure 6, it

will be. That is human nature.

Private debt is

fundamental to capitalism. Without primary and/or secondary private debt there

can be no private productive investment, no privately created GDP and very

little exchange of privately owned capital goods. Only the government would be

able to invest in capital goods by first injecting money to pay for their

production and then taxing that same money out of circulation afterward when

required. In that hypothetical case, hoarding could be constrained within the

bounds of the circulating money supply, initially the 5% or so of GDP of

figures 3 and

{kind=link}

Four of the major

claims made by Irving Fisher in

(a) Reduction of government debt and the interest

burden it creates.

(b) Much better control of credit cycles.

(c) Reduction in private debt.

(d) Elimination of bank runs.

BK claim there are

two further advantages:

(e) A long term increase in output of 10%.

(f) There is no liquidity trap, so that “steady

state inflation” can drop to zero.

The claimed advantages are

described at some length at pages 5-12 of CPRII.

The six claimed advantages are

now considered in turn.

THE SIX CLAIMED ADVANTAGES OF THE PROPOSAL.

(a) REDUCTION OF GOVERNMENT

DEBT & INTEREST BURDEN.

The details in the CPRII proposal are conclusive. The proposal can reduce

or eliminate government debt and its associated interest burden.

However, using CPRII to produce that outcome is unnecessary.

A nation’s authority to eliminate government debt by

exercising its sovereign right to seigniorage on the

creation of the nation’s money supply already exists, as it has always

done.

Most governments have always had the constitutional right to issue

money, as, for example, set out in the Constitution of the

Replacing

government debt with “public” money is simple. As government debt matures it is

replaced by an equal amount of debt-free interest-free deposits created as

journal entries in the Treasury accounts. The financial institution holding the

government paper cancels the debt by writing off both the debt (the institution’s

asset) and the credit (the cash deposit payment it receives) reducing both

sides of its balance sheet by the same amount but leaving its net worth intact.

Since the transaction affects rights under the original debt contract, the

relevant existing original bank deposits remain in the banking system

“magically” backed by public equity instead of private interest-bearing bank

debt.

Where banks

previously held the government debt they will have lost the bank spread on the debt

that has been retired, but the spread is very small in most major economies

today. On 16/4/2013, US Treasury 2/5 yr was 0.23%/0.70% , Japan 2/5 yr

0.13%/0.26%, Germany 2/5yr 0.03%0.34%, and China 2/5yr

2.99%/3.15%.

There are practical

ways to deal with the banks’ loss of bond income should the need arise, such as

by using controls on some deposit interest rates. In other cases (especially

the

There is no valid

reason to embed “public” money within a complex proposal such as the CP. Making

“public” money dependent on reforms like the CP raises suspicion that the

proposals serve primarily to preserve the present dominance of private

financial institutions.

(b) MUCH BETTER CONTROL OF

CREDIT CYCLES.

CPRII claims (p. 5) that

the CP largely eliminates “sudden changes

in the willingness of banks to extend credit [that] not

only lead to credit booms or busts, but also to an instant excess or shortage

of money, and therefore of nominal aggregate demand.”

BK write correctly

that in the present system with each new loan made “[T]he aggregate money supply has therefore increased” whereas

under CPRII “lending banks, now referred to as investment

trusts, would no longer be able to generate their own funding in the act of

lending” (p. 6).

The solution

provided in CPRII is thus two-fold. First, have the

government create the money supply (the quantity of money). Secondly, allow

investment trusts (that will include private banks) to provide the quantity of

credit (secondary debt) the economy needs to function. The credit comes either

as Treasury credit (CPRII

p. 79 Figure 1) from the government or by on-lending private deposits placed in

investment trusts (CPRII p. 6 top). In this scenario

the banks sit as intermediaries on the fringes of the system, clipping the

ticket, risk free, on nearly every financial transaction that takes place in

the economy. This represents a “free lunch” for the banks. Even were such a

proposal acceptable to the public at large, it would still be founded on two

monumental assumptions. The first is that the demand for money is independent

of the demand for credit. The second is that the demand for credit is limited

because it is provided through investment trusts that transfer physical

deposits from lenders to borrowers instead of by banks creating new credit

through the act of lending. Neither assumption bears scrutiny.

There is a direct

link in

M3 = DC +

NFCA + Residual (1)

Where M3 is the aggregate

deposit base, DC is Domestic Credit, NFCA is the Net

Foreign Currency Assets of the M3 institutions and the Reserve Bank, and

Residual is the net worth of the M3 institutions. In

Assets = Liabilities + Net worth.

(DC + NFCA) = M3 + Residual (2)

The Residual is positive in the equation (2) format.

In

At a national

level, debtor countries like

It is possible to

use the Net International Investment Position (NIIP)

in this work. NIIP includes capital flows as well as

current flows. Using NIIP changes the numbers a

little but not the principles being discussed.

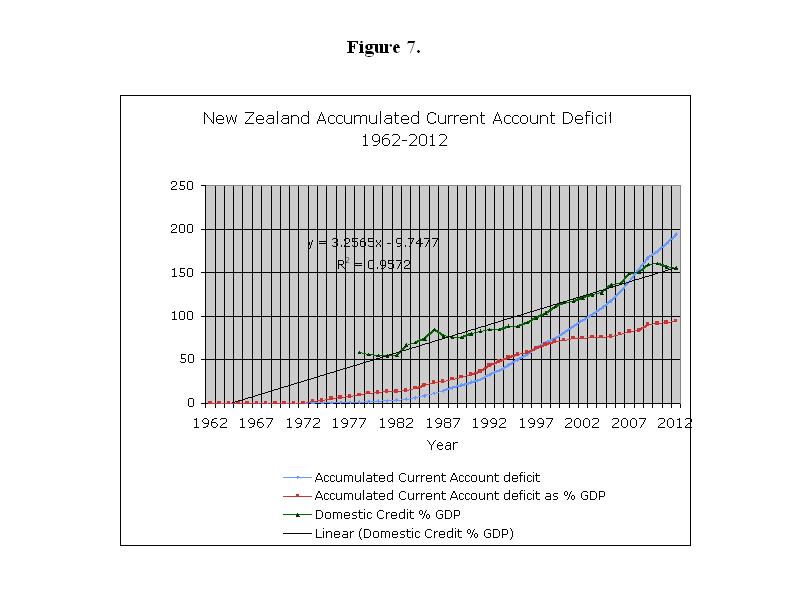

Figure 7 also shows the debt

(domestic credit) as % GDP in

Most of the

accumulated current account deficit, (NZ$ 194.3 billion–NZ$ 41.6 billion or

NZ$ 152.7b. of it), shows up as direct foreign ownership of

{kind=link}

The latest debt figures from Reserve Bank of

The demand for money is therefore not independent of

the demand for credit. This is because the need for foreign exchange funding

and the accumulation of residual by the financial system must be added to the

accumulation of productive capital investment. In CPRII,

when those sums are added to the unrestrained growth of secondary (investment

trust) debt discussed at pages 15-17 of this paper below, it becomes evident

debt cycles can still occur.

From 1978 to 2012

the slopes of the Debt/GDP and Accumulated Current Account (ACA)/GDP curves for

Much of the

additional debt in

Without the NZ$

194.3 billion accumulated current account deficit, New Zealand’s total debt

would apparently be just NZ 126.2 billion, being Domestic Credit $320.5 billion

less current account deficit of NZ$ 194.3 billion. Figures 1 and 2 show that,

in the present system, NZ$ 126 billion is far too little to sustain a NZ$ 200

billion economy which would need about NZ$ 200 billion (GDP) + 5% GDP for the

productive transaction accounts + NZ$ 28.5 billion (bank residuals) or nearly

NZ$ 240 billion. In that case, deposits would be NZ$ 210 billion, just a little

more than GDP instead of 1.4 x GDP as shown in Figures 3 and 4. Moreover, the

economy would be owned domestically instead of a large part of it being owned

by foreigners. New trade agreements like the proposed Trans Pacific Partnership

Agreement (TPPA) are likely to worsen these

structural imbalances unless strong provisions are put in place to protect the

current account.

CPRII (p. 57-58) claims

to take at least some of the

The sum used in CPRII appears to include “at least a conservative estimate of the liabilities of the shadow

banking system...” (p58 – top). That suggests that US$ 4.4 trillion, about

30% of GDP, needs to added to the liabilities side of CPRII

Figures 1-3 (p. 79-81) while about 30% of GDP needs to be added to the debt

side to satisfy equation (1). In other words the diagrams given in CPRII are about 30% of GDP too low. The author assessed the

error at about 25% in a previous detailed critique of the original paper which

can be found in Comments on the IMF (Benes and

Kumhof) paper “The Chicago Plan Revisited” at webiste www.integrateddevelopment.org. That critique was circulated

to BK on 30th August 2012. The claim at

p.14 that “Nobody has so far challenged

our economic model or the model simulations” is therefore factually

incorrect.

Leaving aside the

many other assumptions made in the CPRII model calibration

and the use of DSGE modelling for a macroeconomic

exercise like this, this error alone could be large enough to affect the model

simulation. This assumes the DSGE simulation itself

(pages 32 to 60) were valid. Even then it would still be subject to error

theory where potential error in each variable accumulates through the whole

model simulation. No sensitivity analysis is provided in the CPRII text so the impacts of changes in even a few of the

main variables are not available, rendering the simulation results suspect.

The extra debt is

mostly private debt and BK do not appear to consider

the impact of that private debt redemption on currency exchange rates, the

current account and trade.

The CPRII model calibration for the real economy uses US data “for the period 1990-2006 where available

..... to compute averages ”(p. 55). But for the calibration for balance

sheet data “we use a calibration based on

the final years preceding the crisis” (p. 55). It is hard to see how such

an approach can have either validity or reliability even if the analysis were

really just a “before” and “after” comparison.

A wider objection

to the CPRII analysis and simulation is that control

of the money supply (the deposit base) does not limit the supply of credit as CPRII claims.

Whether or not a

citizens’ dividend is used to convert existing bank debt into credit is

immaterial to the broad outcome of the reform. Investment trusts would still be

needed to channel savings deposits to borrowers. They also provide a pathway to

redistribute a citizens’ income so that existing bank debt can retired. In the

absence of a citizens’ dividend or an on-going citizens’ income, the investment

trusts will still function as S & L institutions to provide secondary

lending in the non-bank debt market as shown in Figure 5 of this paper.

The total debt

(less government debt that has been retired) remains much the same as it is

under the current system except that interest-bearing bank debt is replaced by

interest bearing secondary non-bank lending.

Figure 2 and

equation (1) clearly show that the debt base in the reformed system must be at

least a little more than GDP less the outstanding principal on government

investment even when the money supply is created debt-free. Otherwise there could

be no capital markets and no capitalism because there would be no way to fund

capital investment (see Figures 5 and 6).

The prudential

policy used for modelling CPRII [p. 52-53] is

different to that used for the existing system [p. 45] so changes in the model

results are unsurprising.

The

model calibration in CPRII based on 80% GDP is

therefore unsatisfactory.

In practice,

whether the lending is done through investment trusts or through other forms of

savings and loan institutions there will still be interest-bearing debt. That

total debt could quickly become greater than it is now because CPRII puts no restrictions on non-bank S & L lending

through investment trusts. The same funds can be on-loaned more than once.

The choice to fund

government spending using interest-bearing bank debt is a matter of convention.

Article 104 of the 1992 Maastricht Treaty setting up the Eurozone

constrains the direct supply of central bank debt funding to governments. That

constraint is not a constitutional necessity and it doesn’t apply to the supply

of money by individual sovereign governments, especially were it, for example,

in the form of electronic cash or large denomination coins.

When existing bank debt is repaid from

existing deposits as it matures, or where Investment Trust debt is repaid where

a citizens’ dividend is used, the corresponding deposits are removed from the

banking system. In the absence of new money injections, rolling over the new

secondary debt needed to fund a capitalist economy would require the speed of

circulation of the remaining investment deposits to increase and eventually

approach infinity. If the deposit base were to fall dramatically, the entire

economy would collapse due to massive deflation in the investment sector. On

the other hand, without an independent public monetary authority to properly

manage the new credit injection, there is no way to constrain the growth of

secondary debt. Instead, there would be a cascade of secondary debt from

multiple on-lending of the deposit base. Once an investment trust accepts a

deposit, it must on-lend the deposit at a profit. It must pay interest to its

investors and charge a higher interest rate to borrowers, otherwise it would

quickly become insolvent. In the present system lending, and therefore the

deposit base, is nominally constrained by banking ratios and rules like the

The post reform secondary debt is not all shown on the

CPRII balance sheets (Figures 1-3 p. 79-81) because

it involves a physical and sequential transfer of deposits from lender to

borrower.

If the economy is

to grow under CPRII, there must be a continuous

injection of new non-debt credit into the economy through large-scale

government spending programs and/or by replacing the initial citizens dividend

with an on-going citizens’ income. Otherwise there would not be enough deposits

to meet the needs of both the productive economy and the investment sector. CPRII does not provide for any of this.

There is therefore no evidence that CPRII will limit the demand for credit and no evidence that

credit cycles will be better controlled notwithstanding asymmetric prudential

policy.

(c) REDUCTION IN PRIVATE DEBT.

The CPRII text does not prove there will be a reduction in

private debt; only that there will be a reduction in bank debt. So, in CPRII Figure 1 (p. 80) there is 80% of GDP in investment

loans backed by Treasury Credit and bank equity, exactly the same as there is

at present. The foregoing discussion shows it is theoretically impossible to

support a capitalist economy using a debt of 80% of GDP. That means that at

least some of the deposits must be

on-loaned through savings and loan institutions.

Under the CP

proposal “private credit is now only

extended [by the government] to capital investment funds” (p. 47).

Since 80% of GDP is insufficient to support the productive economy either the

government will have to lend more, or capital investment will also have to be

funded from secondary debt.

CPRII refers to this on

page 48 where there appear to be two kinds of trusts: Treasury funded

investment trusts to fund capital investment and privately funded trusts

initially established to “smooth” the retirement of bank debt when a citizens’

dividend is used to enable bank debt to be repaid. The aggregate surplus

citizens’ dividends have to be on-lent to net debtors as part of the transition

process. To prevent those deposits from being spent and adding to productive

sector transaction account money, the surplus deposits “could then be converted into the equity shares or non-monetary debt

instruments of the investment trusts envisaged by Simons”.[p. 48] However, the surplus deposits can only

become liquid as the secondary debt is repaid.

Note that the Manning plan for permanent

debt reduction in the national economy available a www.integrateddevelopment.org also requires the

surplus citizens’ income deposits to

be sterilised during a transition phase.

In practice, almost

all the system deposits will be either borrowed from the Treasury (capital investment) or on-loaned at least

once by private investment trusts.

Today, private bank

debt is unequally distributed in the population at large, so only a relatively

small proportion of it (it’s about one third in

Investment Trusts

cannot afford to pay interest on deposits unless they on-lend them. The only

possible conclusion is that there will be relatively little reduction in

private debt and that it is likely that private debt could increase through the

cascading effect of deposit recycling. Without a worthwhile incentive to save,

investment sector deposits could leak into consumption, causing rapid inflation

in the real economy.

(d) ELIMINATION OF BANK RUNS.

This claim might

seem at first sight to be valid in so far as the deposit base is fully secured

against reserves, but it is not necessarily so. There will probably be bank

runs just as there are now because the financial system will be no more stable

than it is now. There is nothing in the proposal that suggests there will be

less risk-taking by financial institutions. If the capital investment trusts

borrow Treasury credit (CPRII Figures 1 -3 p. 79-81) and private investment trusts

on-lend much of the deposit base, lending institutions would still collapse if

defaults on those loans were to exceed their (reduced) equity. If a financial

institution collapses, or even looks like doing so, depositors are still likely

to withdraw their deposits. All that happens is that the institution’s assets

(reserves) and liabilities (deposits) decrease by the same amount, rapidly

shrinking the institution’s balance sheet. However, that safety net applies

only to the current holders of the deposit base. It does not apply to the

investors who have on-loaned deposits through the investment trusts. They will

still lose that part of their

on-loaned deposits that cannot be recovered from the realisation of their loan

security, just as they do now. The aggregate deposits remain the same but the

investment trusts can be easily bankrupted with all the same outcomes as at

present. Many lending institutions could be more vulnerable than they are under

the present system because, according to BK Figures 1

and 3, their equity has been drastically reduced while the aggregate debt base

including secondary debt has not.

The statement at CPRII p. 49 that there is a large increase in the business

sector (manufacturers) balance sheets appears to be based on the assumption

that because manufacturers form one group of economic agents in the modelling

all business debt will be retired using a “manufacturers dividend” similar to

that proposed for households.

Such a proposal is morally and legally unsupportable

The statement [p. 49] that Manufacturers’ “principal

is instantaneously repaid through the citizens dividend” is manifestly

unjust because, in the US alone, it would represent a US$ 3 trillion gift to

business shareholders in addition to their own citizens’ dividend. Instead, the

citizens’ dividend should include the manufacturers’ debt, so the manufacturers

borrow from the private investment trusts like most other private individuals.

Under CPRII, while Manufacturers will no longer be carrying bank

debt in aggregate, most will still be carrying a similar amount of private debt

because the Manufacturers’ dividend will be asymmetrically distributed just as

private debt is.

The “riskless debt”

assumption made in the text is also incorrect as is the claim that the “steady state level of this borrowing is

however zero”. Business lending is always risky, and, as already discussed,

business debt must at least equal to GDP whether or not the money supply itself

is debt free. There might conceivably be some useful reason to consider

negative real interest rates for Treasury credit supplied to investment trusts

for new business capital [p. 51]. However, if that is done for business, the

same benefit should also apply to households, using, for example an on-going

citizens’ income payment. Otherwise, a negative real interest rate would

represent yet another handout to business shareholders.

The CPRII proposal as it is

presented does not eliminate bank runs because banks can still fail and

investors’ claims on the banks’ deposits can still exceed the banks’ deposit

base if the ratio of secondary lending to deposits exceeds 1. That applies

whoever legally “owns” the deposits and despite the strenuous efforts to take

account of loan losses in the model parameters. Perhaps, the only way to avoid

the moral hazard implicit in the proposal is to carefully manage secondary

lending as proposed in Available in the Manning plan for permanent

debt reduction in the national economy at www.integrateddevelopment.org which incorporates a

variable business citizens income for each full time equivalent employee but it

is not a lump sum payment as in CPRII. It would

probably also be subject to regulatory wage requirements.

(e) A LONG TERM INCREASE IN

OUTPUT OF 10%.

The preceding

discussions (Figures 1 and 2 above) show that when investment capital and

resources are readily available it is a simple matter to dramatically improve

relative economic outcomes far in excess of the 10% claimed by BK (actually 8% on CPRII Figure 5

p. 83). By far the main benefit in the CPRII proposal

is the direct funding of investment capital to business in the form of low

interest Treasury credit. Careful allocation of that credit will enable large

increases in output over a short time frame. That is one major reason

A US$ 500 billion net injection of productive capital

into the

The 10% long-term

output increase over 12 years is far too conservative.

The intent of the

model simulation is to compare economic outcomes before and after the CPRII changes are introduced. Such a comparison is bound to

be artificial because the format of the model forces an outcome consistent with

the modelling assumptions and calibration. The simulation results shown in CPRII Figures 4 to 7 (p. 82-85) in all likelihood

overestimate the performance of the current system and underestimate the

economic benefits of the plan.

The model simulation claims an

increase of output of 10% but, on the basis

of error theory, such numbers are meaningless. Based on 100 variables each with

10% error it is likely to have a 95% confidence limit of +/-

1000% or more. There are, however, far more than 100 variables in the

model.

With a confidence limit

of 95% one might be confident a numerical value of 1000 has a 95% probability

of being between -9000 and + 11000....but that would hardly be appropriate for

meaningful analysis. Error theory applies both to the model equations (p.

32-55) and to the calibration (p.55-61). The equations and numbers also assume

the DSGE modelling technique is applicable to this

kind of macroeconomic analysis. Even when the same errors apply to each

individual term used in modelling the existing system and the CP, they will not

accumulate symmetrically in the results if the equations, or even the weighted

use of the same equations underpinning the modelling are different, as is often

the case.

There are too many

modelling issues to discuss in detail in this paper. Just a few are mentioned

below to give some idea of their scope.

The BK analysis assumes everyone will respond the same way

under the different financial regimes though no evidence is offered for that

assumption. There could just as likely be dramatic changes in public perception

and confidence were the financial system to become more trustworthy,

transparent and accountable.

The model

parameters are all based on an equilibrium “optimization” over time spread over

all agents in each category. For example,

(p. 43) “All manufacturers have

the same initial stocks of deposits, loans and net worth” and “all manufacturers make identical choices in

equilibrium”. Even if there were any equilibrium there is no reason to

suppose such model boundary conditions exist now or would ever apply

symmetrically across different financial systems. The entire modern economy is

based on asymmetry gained through corporatisation, globalisation, and

institutional preferential treatment. An economy satisfying egalitarian model

assumptions would quite likely be more efficient and productive than the

present multinational oligopoly protected by a plethora of perks and patents.

Superficially

egalitarian model assumptions cannot properly be applied to an intensely

asymmetrical economy. Notwithstanding that, the CPRII

analysis seems to be weighted in favour of the existing system and against the CPRII reform proposals that could be used to reverse some

of the existing financial system asymmetry. The modelling bias may be

intentional: taking a very conservative approach may help mask some of the

other issues relating to the model methodology even though in doing so it

underestimates the economic benefits of the proposal. BK

could justifiably argue that if the CPRII proposal

“works” under the model parameters they have applied in their paper it would

work much better if more appropriate reform parameters were used.

It is easy to

increase economic output when all aggregate business debt has been forgiven and

when a low defined steady state

interest rate is conveniently built into the model variables (CPRII p. 51) and only directly affects decisions on

physical investment. “The government

subsidizes investment trusts to equalise the average funding costs of the

government and of the lowest-risk private corporations.” [p. 52]

As already noted, this by

itself should translate into very high output gains.

Undoubtedly, the

giant multinationals would be perceived as the lowest risk private

corporations.

Overall, the assumptions made

for key variables are ideological, not practical.

There is no reason

to suppose growth needs to be artificially restrained at 2% or inflation at 3%

or default for investment loans at 1.5%. The distribution of net worth is

managed so that manufacturers’ (corporations, banks) do not reach the point

where debt financing becomes unnecessary (CPRII p.

40). Everyone is perfectly rational. There is no relative flow of net worth

among different groups. Business mortgage property debt and residential

property debt are given the same risk weighting (0.5) even though business risk

is 100% and residential property 35% (p. 56). The same goes for keeping the

labour share of income fixed... and so on.

Nor is there any

logic in assuming a steady rate of consumption between constrained and

unconstrained households of 4:1 (CPRII p. 55). The

implication is that the relative household income distribution and expenditure

patterns will not change under the proposals. If the population at large does

not benefit from the changes there would, from the public perspective, be

little point in making them. This is especially important when considering the

existing lopsided wealth and income distributions.

CPRII will continue the

concentration of private wealth and income into fewer and fewer hands because

it does little, if anything, to reduce either the debt servicing burden placed

on the public at large or improve wealth and income

distribution.

There is an

acknowledged moral judgement in this statement. BK

can justifiably argue that the CP was never intended to benefit the public at

large but to stablilise the financial system. But

what would be the point in stabilising the system so the existing tiny

financial and business elite (the 1% of the “occupy” movement) can become

tinier and even more elite? Without a moral dimension promoting broad public

and environmental benefit, CPRII becomes just another

proposal to further consolidate the power of financial institutions.

(f) THERE IS NO LIQUIDITY

TRAP.

This claim is partly true.

The relative

proportion of transaction (non-interest-bearing) deposits to total deposits may

vary over time depending on the demand for debt and the interest rates expected

by the investor, which is the investment trust, in the secondary debt market.

The interest rate will be determined by the supply of new money. In CPRII this is done using a “nominal money growth rule that controls the broad money supply and

thereby inflation”[CPRII p. 10].

The CPRII modelling uses a Friedman nominal money growth rule

formula (CPRII equation 31, and p.61 top). That only

controls inflation in the productive sector if just the right amount of new

money is allocated to the productive transaction accounts used to generate the

economic output. However, measured inflation is not just about the amount of

new money, but where it goes. In the CPRII proposal

it seems to be directed into new production, which is good. However, as shown

in Figures 3 and 4 of this paper, setting money growth equal to the growth rate

of output is insufficient in a debt-based system, whether that debt is bank

debt or secondary S& L debt. BK also use a “conventional forecast based interest rate

rule” (CPRII equation 20) to model the policy

inflation rate (price stability) in the present system. The target inflation is

expressed in terms of the change in government debt and a “steady state nominal interest rate”.

Neither of the above formulae

represents the real economy because neither of them enables the basic

accounting formula equation (2) (p. 10) in this paper to be satisfied.

Assets = Liabilities + Net worth.

(DC + NFCA) = M3 + Residual (2)

Equation (2) can easily be

expressed for the post CPRII reform as in equation

(3):

Assets =

Liabilities + Net worth.

Treasury credit + Residual

debt + NFCA = Deposits +

Residual (3)

Where:

-Treasury credit is

the debt-free central bank credit,

-Residual debt is

the sum of [remaining bank debt during the reform transition period + any

central bank lending to banks or investment trusts for government and private

productive capital investment]. The Residual (the banking sector’s net worth)

is expressed in equations (2) and (3) as a positive quantity because it is not

part of the money supply.

-Deposits are the

total deposits (M3) in the banking system,

-NFCA is the net foreign currency assets of the financial

institutions.

Secondary debt from

the on-lending of deposits through the investment trusts is not fully included

in equation (3) because it resides nominally outside the banking system even if

the banks act as intermediaries. Despite that, the secondary debt is crucial

when calculating economic outcomes because it is fundamental to the health of

the investment sector. There are various ways to visualise the secondary debt

as a proportion of Treasury credit or as a proportion of deposits while bearing

in mind that secondary debt can be higher than either the deposits or the

Treasury credit due to the cascading effect of multiple on-lending of the investor

deposit base.

When the amount of

secondary debt exceeds the deposits in the investment trusts the investment

sector must inflate because interest-bearing trust deposits MUST be on-loaned if

the trusts are to survive. That WILL create an exponential price spiral in the

investment sector. That means that the CPRII proposal as it is

presented will fail.

Neither equation

(20) nor equation (21) in CPRII takes the above

factors into account so they are unsuitable for modelling purposes. That is why

Friedman monetarism failed and why inflation rate targeting and attempts to use

a

Deposits other than

transaction account deposits must

circulate in the Investment trusts. If they do not do so there will be

catastrophic inflation in the productive sector. As the

interest paid on investment accounts falls toward zero there will be little

incentive to save the money in them. Some of the money will migrate into

transaction accounts where it will be

used for consumption. The reformed CPRII system relies on a worthwhile “incentive to save”

being offered to investors. That interest necessarily causes inflation in the

productive sector. For more detail see the various papers by the author at www.integrateddevelopment.org. That means there

can be no steady-state inflation under CPRII. The

inflation level will instead depend directly on the average interest rate the

Investment Trusts pay to investors and that will depend upon how the investment

sector as a whole is managed.

Since the

injections of new Treasury credit are specifically directed toward productive

investment they will stimulate monetised economic growth as long as there are

unused or underused resources available within the economy. As previously

noted, most of that new money injection

must be hoarded or saved in the investment trusts.

There is no risk of

a liquidity trap if the Treasury credit creation is managed properly but there

will not be zero steady state inflation.

CONCLUSION.

CPRII is designed to

position the banking sector so it can continue to dominate world banking and

finance following the introduction of broad-based monetary reform. That reform

is proposed in response to the now widely acknowledged failure of the current

financial system based on interest bearing debt created ex-nihilo by private

financial institutions.

BK openly acknowledge

this in their paper at p. 20:

“The volume

of credit would still be mostly controlled by private financial institutions,

and the allocation of that credit would be completely controlled by them”.

This is the

opposite of the statement BK made in Part V A : Banks at p. 34 (top) in their earlier paper: “Under this [CP] funding scheme the

government separately controls the aggregate volumes of credit and the money

supply.”

In CPRII

the word “controls” has been changed to the word “influences”.

The heart of the CPRII proposal is to separate the monetary and credit

functions of the banking system. Bank-created credit (interest-bearing debt)

will be replaced by government-issued money (debt-free Treasury credit). All

other credit the economy needs will be generated either from investing retained

profits or from on-lending the (non-bank created) deposit base. That on-lending

will create interest-bearing secondary debt, which is ignored in the CPRII proposal [Figure 1 p. 79].

Cancelling

government debt with government-issued money could improve government finances

but a large pool of secondary debt will still be needed to fund the exchange of

financial assets in the investment sector. Otherwise the investment sector will

quickly collapse. In CPRII the prices for and

quantity of that secondary debt are open-ended. Banks, acting as intermediaries

for the pooling and allocation of that non-bank credit, will still charge their

bank spread and other fees for their services. CPRII

substitutes secondary debt for bank debt while at the same time reducing the

banks’ risk and exposure to bad debt.

Under CPRII the commercial banks retain their present domination

and discretion over how funds in the private sector are invested. This power is

now used first in the interests of their shareholders and then in the interest

of their “friends” at the cost of small and private businesses and investors

and the taxpaying public at large.

Effective monetary

reform requires that the volume, price and allocation of debt funding as well as

money be managed for the public good rather than for private profit. This does

not appear to be the real objective of the CPRII

proposals.

THE REFERENCED PAPERS

The

referenced papers :

00. Summary of papers published.

01. Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

02. How to create stable financial systems in four

complementary steps.

03. How to introduce an e-money financed virtual minimum

wage system in New Zealand.

04. How to introduce a

guaranteed minimum income in New Zealand.

05. The interest-bearing debt system and its economic

impacts.

07. The DNA of the debt-based economy.

08. Manifesto of the debt-based economy.

09. Unified text of the manifesto of the debt-based

economy.

10. Using a foreign transactions surcharge (FTS) to manage the exchange rate.

11. The Manning plan for permanent debt reduction in the national

economy.

12. Comments on the (Jaromir

Benes and Michael Kumhof) Chicago Plan Revisited

Paper.

13. Missing links between

growth, saving, deposits and GDP.

15. Measuring Nothing on the Road to Nowhere.

16. Debt bubbles cannot be popped : Business cycles

are policy inventions.

Return to :

Bakens Verzet Homepage

"Money is not the

key that opens the gates of the market but the bolt that bars them."

Gesell, Silvio, The Natural Economic Order, revised English

edition, Peter Owen,

This work is licensed

under a Creative

Commons Attribution-Non-commercial Share-Alike 3.0 Licence.