NGO Another Way (Stichting Bakens

Verzet), 1018 AM

SELF-FINANCING,

ECOLOGICAL, SUSTAINABLE, LOCAL INTEGRATED DEVELOPMENT PROJECTS FOR THE WORLD’S

POOR

|

FREE

E-COURSE FOR DIPLOMA IN INTEGRATED DEVELOPMENT |

|||||

Edition 02 :22 July, 2013.

(VERSION EN FRANÇAIS PAS DISPONIBLE)

Summaries of

monetary reform papers by L.F. Manning published at http://www.integrateddevelopment.org.

Chicago Plan Revisited Version II: An insufficient

response to financial system failure. (Posted 11 May, 2013.)

Comments on the (Jaromir

Benes and Michael Kumhof) Chicago Plan Revisited Paper.

Debt bubbles cannot be popped : Business cycles are policy inventions.

DNA of the debt-based economy.

General summary of all papers

published.(Revised

edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

Manning plan for permanent debt reduction in the national economy.

Measuring Nothing on the Road to Nowhere.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

There’s no such thing as affordable housing.

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple Starts

Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

![]()

This

work is licensed under a Creative

Commons Attribution-Non-commercial-Share Alike 3.0 Licence

MEASURING NOTHING ON THE ROAD TO NOWHERE: THE

MYTHS OF INFLATION AND GROWTH MEASUREMENT.

By

Sustento Institute, www.sustento.org.nz

July, 2013

email:

manning@kapiti.co.nz

This

paper shows conclusively that the existing world economic order is approaching

a state of structural collapse as the sum of accumulated systemic inflation (Ms

in the paper) plus the bank residual (R in the paper) approaches nominal GDP

leading to debt default and the destruction of GDP.

The

policy response to such a systemic collapse requires all of:

(a) Reducing

deposit interest rates toward zero [in progress]

and

(b) Managing the money supply

and

(c) Controlling cross border capital flows

and

(d) Stimulating productive investment

and

(e) Reversing income inequality.

Paper

released 9th July 2013.

EXECUTIVE SUMMARY.

More people working

efficiently for more hours increase productive output. The same people working

more efficiently for the same number of hours increase their productivity. Both

are forms of economic growth. Orthodox economics generally discounts real

productivity gains and fails to effectively measure economic growth. By using

the basic accounting equation and the debt model described in the paper,

economic “growth” can be better managed without creating the boom and bust

cycles that are typical of orthodox approaches to money supply. The paper

suggests there are few measured productivity gains in the debt-based financial

system. All “price” is inflation and most nominal GDP increases now represent

systemic inflation.

The paper also shows how

productive sector consumer price (CPI) inflation is misrepresented in key

economic data. CPI inflation measured as an increase in consumer prices over

time cannot simply be subtracted from the nominal increase in the value of

Gross Domestic Product (GDP) to provide an economic “growth” figure because the

average percentage “value” of inflationary increases in GDP is only half the

percentage CPI price rise.

Since the

Neither approach has worked

because neither approach satisfies the basic accounting equation given in

equations (1) and (2) discussed in this article, resulting in decades of poor

economic outcomes and devastation for countless millions of people around the

world.

BACKGROUND.

Recently, there has been a

great deal of discussion about a monetary reform program called the Chicago

Plan. The IMF has modelled that proposal in a working paper called “The Chicago

Plan Revisited” (CPRII) ( see Jaromir Benes & Michael

Kunhof, IMF working paper WP/12/202

final version 12th February, 2013). The proposal entails replacing existing interest-bearing

bank debt with debt-free, interest-free money called Treasury Credit in an

effort to stabilise the world’s monetary system. The CPRII modelling uses a

Friedman nominal money growth rule formula (CPRII equation 31, and p.61 top)

for the reformed monetary system. That controls inflation in the productive

sector only if just the right amount of new money is allocated to the

productive transaction accounts used to generate “optimal” economic output. As

discussed below, setting money growth equal to a subjectively established

growth rate of output is insufficient in a debt-based system, whether that debt

is bank debt or secondary (Savings and Loan) debt. Benes and Kumhof also use a

“conventional forecast based interest

rate [

This paper suggests the Friedman

money rule and

Figure

1 shows M3* 0.945 and GDP plotted against time for

{kind=link}

{kind=link}

Due mainly to the increase in New Zealand’s negative

net foreign currency assets, the investment sector in New Zealand has grown at

5.9%/year while its nominal GDP has grown at 5.2%/year over the same period.

That is partly why prices in the non-productive investment sector there are

“overvalued” and why neither the Friedman rule nor the

[Figure 1.

The author’s paper the DNA of the debt-based

economy demonstrates that GDP equals the outstanding

principal on productive capital investments (fixed capital formation). Were the

growth of 0.945* M3 to exactly follow the growth of nominal GDP, the prices of

existing assets in aggregate would

closely mirror nominal GDP.

The reasons why the Friedman

and Taylor rules cannot apply, and the myths underpinning present inflation and

growth measurement are now discussed.

THE RELATIONSHIPS BETWEEN MACROECONOMICS AND THE BASIC ACCOUNTING

EQUATION.

Dollar references in this paper are to the

It is impossible for deposits to be lower than the existing

interest-bearing debt in the capitalist system after subtracting the country’s

net foreign currency debt and the banks’ net worth that they have “captured”

from the deposit base. Otherwise the basic accounting equation (1) below is not

satisfied.

Debt is linked to deposits, the current account and capital transfers by

equation (1) :

(DC + NFCA) = M3 + Residual (R) (1)

Assets = Liabilities

+ Net

worth

The formula in equation (1) represents the basic accounting equation. The Residual is positive in the equation (1) format, while NFCA is negative for debtor countries.

Equation (1) can easily be

expressed for the post CPRII monetary reform proposed in The Chicago Plan and

other financial reform proposals using debt-free, interest-free money, as in

equation (2):

Assets = Liabilities +

Net worth.

Treasury Credit + Residual debt + NFCA

=Deposits + Residual (R) (2)

In equations (1) and (2):

DC =

Domestic Credit.

NFCA =

Net Foreign Currency Assets of M3 institutions plus those of the Reserve

Bank ( in

(RBNZ)).

M3 =

Deposit liabilities of M3 institutions plus those of the Reserve Bank ( in

Residual R = Aggregate retained bank profits

+ paid up capital.

Treasury Credit =

Debt-free, interest-free central bank credit.

Residual debt = The

sum of [remaining bank debt during the reform transition period + any central

bank lending to banks or investment

trusts for

government and private productive capital investment].

Equation (1) is the basic accounting equation stated from the banks’

point of view.

In

The orthodox

(Friedman and Taylor type) monetary policy rules fail because they consider

only the productive economy whereas they have to satisfy the basic accounting

equation (equation (1)) that also includes the non-productive investment

sector, the accumulation of bank net worth and the external investment

position.

In contrast to orthodox

economics, the author’s modified Fisher Equation of exchange fully satisfies

equation (1). It is :

DCm

=(GDP)/Vy +Ms +Dni +Db+R - Dnfca+Nb (3)

Where:

DC = Domestic Credit.

DCm = Domestic Credit plus secondary debt Nb borrowed

through non-bank lending institutions (NBLI). (DC = DCm-Nb).

GDP/Vy = The debt and cash used to create GDP

(Dmy= Dmt+M0y).

GDP = Gross Domestic Product.

Vy = The speed of circulation

of productive transaction accounts.

Dmy = The productive transaction

account balance used to generate GDP.

Dmt = The portion of Dmy

arising from bank debt.

Dni = Debt

supporting non-inflationary economic growth.

M0y = The portion of Dmy

contributing to the non-inflationary cash transactions M0y * Vy

. (M0y * Vy is

included in Dni).

Ms = Accumulated systemic

inflation arising from net after tax deposit

interest paid on the total system debt DCm.

Dnfca = Net foreign currency assets resulting

from the current account and capital transfers from the rest of the world.

Db = Bubble debt (debt in

excess of the systemic debt requirements).

R = Bank residual retained profits and paid up

share capital not being part of the money supply M3.

Nb =

Secondary non-bank debt.

Note that the original version of the equation has been updated because

it erroneously incorporated the whole of the accumulated current account

deficit in the model instead of NFCA as required by equation (1).

The modified Fisher Equation (3) is reconciled with the basic accounting

equation as shown below:

(DC + NFCA) = M3 + Residual

(R) (1)

Assets =

Liabilities + Net worth

Where :

NFCA = The net foreign currency

assets of the M3 banking institutions and the central bank.

DC =

Domestic Credit = DCm

-

M3 =

Deposit base of the M3 banking institutions.

The formula represents the basic accounting equation, where DC is Domestic Credit plus secondary non-bank debt, M3 is the total bank deposits, NCFA is the Net Foreign Currency Assets of the banking system and Residual is the net worth of the banking system. The Residual is positive in the equation (1) format, and NFCA is negative for debtor countries.

Substituting the terms from equation (3) into equation (1) gives:

Assets = Liabilities + Net worth

DCm =[GDP)/Vy +Ms +Dni

+Db +Nb ] + R - Dnfca (3)

(DC + Dnfca) =[ Dmy +Ms +Dni

+Db +Nb]

-Nb + R (4)

Where from equation (1):

M3 = [Dmy+ Ms +Dni

+ Db] (5)

Figure 2 shows the main

elements of the author’s debt model.

{kind=link}

Statistics are publicly available for all the variables in equations (4)

and (5) except for Vy, Ms Dni and Db.

Initially, empirical estimates have to be made in the

calculation of Ms and Vy because the physical data for

them is not yet directly available. There is no reason, however, why data for Ms

and Vy cannot be physically collected. The model is validated by

solving equation (4) or (5) for Dni and Db as shown in Figure 4

and Figure 6.

{kind=link}

{kind=link}

Equations (4) and (5) require

no other multipliers or assumptions.

Since the productive investment account balance (My)

used to generate GDP can be estimated by analysing physical cash flows in the productive

economy, a straightforward application of equation (3) will produce the

“bubble” debt Db as a residual once Dni has been

estimated. A positive rate of change of Db indicates bubble

formation in the economy while a negative rate

of change means bubble decay. Dni

can be calculated using equation (9). A key objective of macroeconomic policy

settings is to ensure Db = 0, that is, that there is just enough

debt growth to provide for the system costs (investment sector, plus productive

sector inflation) and support the cash-based transactions and other

non-inflationary increases in the economy.

[Figure 2.

The Schematic Debt Model.]

There is another crucial relationship developed by the author. This is

referred to above. In a debt-based financial system:

[GDP]=Outstanding debt

principal on productive capital investment. (6)

Equation (6) implies that the minimum theoretical domestic credit

DC required in the present debt system to support the productive

economy is:

DC = GDP/Vy

+ [GDP ] (7)

Suppose now that Dnfca and Db were zero as

“assumed” by the Friedman and Taylor rules. Cancelling the zero terms in

equation (4) (bearing in mind that Dnfca is the debt representing

NFCA, and Dmy is the debt representing GDP/Vy ) leaves in

that special case:

(DC + Dnfca) =[ Dmy +Ms +Dni

+ Db] + R (4)

DC

= GDP/Vy+ Ms + Dni + R (8)

Comparing equations (7) and (8) leaves in that special case:

GDP/Vy + [GDP] = GDP/Vy

+ Ms +Dni + R

[GDP] =

Ms +Dni + R (9)

In the special case of no

foreign debt and no bubble, GDP comprises systemic inflation Ms that

incorporates new debt to fund inflation, plus

new debt Dni to fund non-inflationary growth, plus the non-circulating bank residual

R. When Dnfca and Db are non-zero, DC, GDP and the terms

in equation (9) will vary because they are each dependent on the size of DC.

The debt model enables the effects of price (P) and output (Q) which

together form GDP to be studied in a way that orthodox economic seems to be

unable to do. As discussed later on, orthodox economics is

also mismeasuring productivity increases.

The debt model is far from radical. It is simply a revision of the original

Fisher equation of exchange still applicable to the productive economy:

M*V =

P*Q : [in the debt model (My * Vy = GDP)] (10)

Where:

M = money supply.

V = speed of circulation of M.

Q = output of goods and services.

P = price level.

Several important consequences follow from the revised Fisher equation

model and from the equations referred to above. The points discussed below are

not in order of priority.

Accumulated Current account

deficit plus capital transfers from abroad and the Net Foreign Currency Assets

of the banking system (NFCA).

The accumulated current

account and direct capital transfers from the rest of the world play a key role

in economic performance because the Net Foreign Currency Assets form part of

the money supply M3. On the other hand, accumulated deficits on a current

account deficit and capital transfers increase foreign ownership of a debtor

country’s economy, making the current account itself more difficult to manage.

Capital inflow (NFCA) increases the money supply M3 in the receiving (creditor)

country, increasing systemic inflation Ms there, and vice versa for

a debtor country. There are no “ifs” or “buts” about this.

The only practical way for

debtor countries to overcome this problem is to reverse foreign debt growth

using an effective tool such as a Foreign Transaction Surcharge (FTS) proposed

by the author to manage capital flows. [ For more information see Using a foreign transactions surcharge (FTS) to manage the

exchange rate.] It cannot be done by monetising the foreign debt

because while doing that might lower the exchange rate it also inflates

domestic costs, negating the benefit of the lower exchange rate.

Current accounts also dominate

the domestic interest rate structure in debtor countries because foreign

investors have to be encouraged to buy and own the debtor country’s assets. The

debtor country has to “compete” with the rest of the world to attract that

investment by offering relatively high financial returns. Since the domestic

systemic inflation Ms is the net interest paid on the

Domestic Credit (plus the net interest on Nb), domestic inflation

cannot be properly managed in the presence of substantial interest-bearing

foreign debt. Many economists will claim

That makes “free trade”

proposals like the Trans Pacific Partnership Agreement (presently being

negotiated in secret) suicidal for the domestic economy of debtor countries

unless they provide for effective control of capital flows in the national

interest.

They don’t.

Productive

Sector Inflation.

Domestic Credit (DC) and secondary

debt (Nb) must typically be funded from the productive economy. In

this paper,

Domestically, cost-push

inflation is systemic and is the net deposit interest Ms

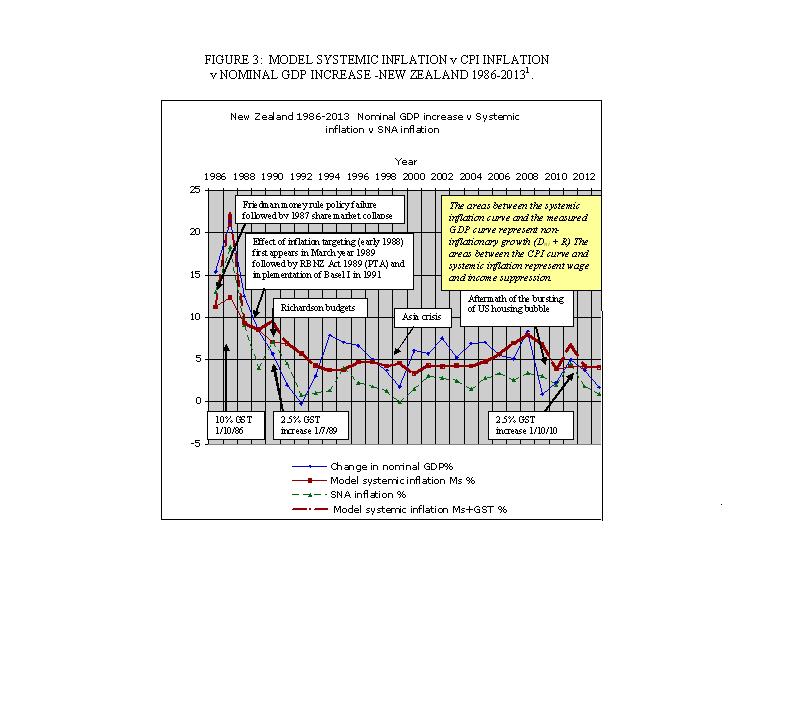

shown as Model Systemic Inflation in Figure

3. In

The main methodological issue

in calculating Ms is working out the net tax payments on the

interest because the tax represents a transfer payment to the government and so

remains in the productive economy. The effective tax rate on those receiving

deposit interest is the average tax rate paid over all the tax-payer’s income,

not the top marginal tax rate applied to that tax-payer’s income. Accurate

estimation of the net aggregate deposit interest lies beyond the scope of this

paper and is subject to further research. The NZ Department of Inland Revenue

can provide data on the tax paid on each income band and the numbers of people

in each band. An accurate assessment of tax may therefore be possible but it is

complex. In practice, it may be better to create new reporting and data series

to accurately calibrate the debt model deposit interest. The model is fairly

sensitive to the tax rate, so Figure 3 is preliminary

pending further work on the tax deductions on gross deposit interest.

Managing productive sector inflation

depends on eliminating deposit interest as far as possible. That is why

measured CPI inflation is very low in countries like

[Figure 3 : Model Systemic Inflation v. CPI Inflation v. Nominal

GDP increase New Zealand 1986-2013.]

Deposit interest rates used

to calculate systemic inflation are from Reserve Bank of

GDP

could be managed by changing the financial system to minimise systemic

inflation by reducing interest rates toward zero, and by managing the money

supply to fully utilise the physical economic resources available to the

economy, greatly reducing CPI inflation.

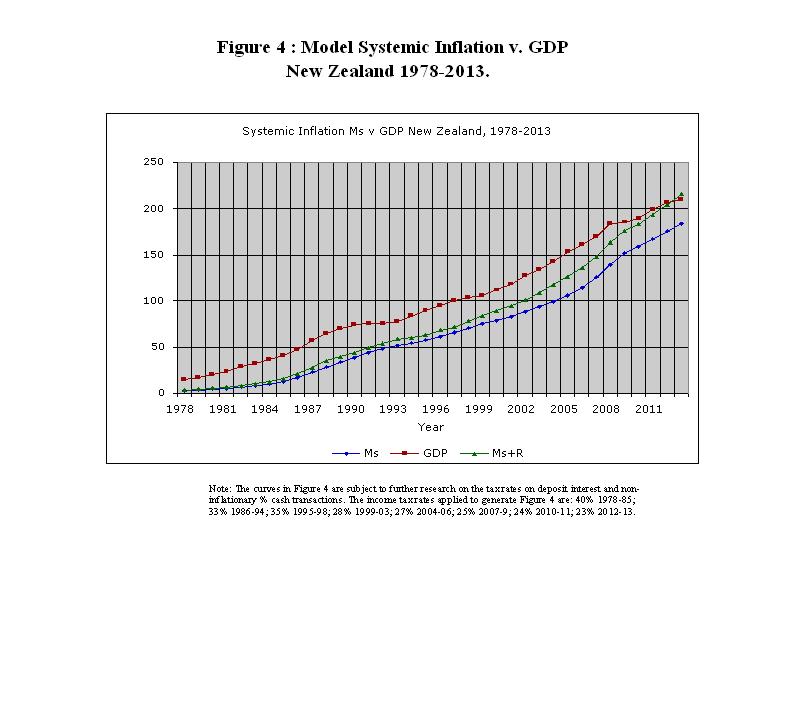

Since the debt model requires

exponential debt growth, Ms is also an exponential function. Figure 4 shows that the

accumulated inflation-free GDP component has been shrinking as a proportion of

GDP in

[Figure 4 :

Model Systemic Inflation v. GDP

Figure

4 suggests Dni has all-but disappeared

in

Figure 4 shows why real

incomes in many developed economies have been stagnant or falling in recent

decades. As shown later on (using the Fisher equation of exchange), the real

impact of systemic inflation is being masked by the suppression of

incomes.

There has been no aggregate

real growth in

Zero

Deposit Interest is Impossible in a Capitalist System.

GDP in the debt model is the net

outstanding principal on productive capital investment (fixed capital

formation). The reason this is so is set out in the author’s paper the DNA of the debt-based economy. In the capitalist system there must be debt

to enable the purchase and exchange of capital goods.

In a reformed financial system based on debt-free money, the money to purchase and exchange capital goods is borrowed from deposit holders at interest on a Savings and Loan (S&L) basis instead of from commercial banks. Consequently, there must be an “incentive to save”, otherwise there will be leakage from investment sector to the productive sector causing very high demand-pull inflation in the productive sector. In fact, all the main monetary reform proposals such as the Chicago Plan (CPRII), the Manning plan for permanent debt reduction in the national economy, the Positive Money proposal in the UK, and the AMI proposal in the US feature S&L lending.

When deposit interest rates are

close to zero, demand-pull inflation is limited only when savers choose to

hoard for a rainy day despite receiving little or no deposit interest (as was typical

in pre-industrial times), or where they choose to invest in dividend-bearing

investments or in direct productive investment for profit. This is commonly

called the “opportunity cost” of capital. A major difference between the modern

economy and that in pre-industrial times is that the relative amount of “saved”

money in the investment sector is proportionately much greater now than it used

to be.

With low interest rates and systemic

inflation there would be little property speculation because there would be

little aggregate capital gain. Instead, the investment property market would be

governed by the net return on investment such as, for example, net rental

income.

The core solution to rising

property and equities prices around the world is therefore to manage the debt and

money supply while reducing deposit interest rates to a level just sufficient

to provide an “incentive to save”. The only proposal currently complying with

the debt model and the accounting equation that does this is the author’s “The Manning plan for permanent debt reduction in the national economy.”

MEASUREMENT

OF GROSS DOMESTIC PRODUCT (GDP).

Orthodox economics divides the

increase in the nominal value of GDP into two parts: “inflation” and “growth”. In the original Fisher equation of

exchange, (equation 10), that still applies directly to the productive sector

in the debt model, changes in output on the variables (using Newtonian

notation), assuming speed of circulation Vy is constant, are given

by:

(My + dMy/dt)

*Vy = (Q + dQ/dt) * (P +

dP/dt) (11)

Therefore:

(P + dP/dt) =

((My + dMy/dt) / (Q + dQ/dt)) *Vy (12)

and the price increase:

dP/dt = ((My

+ dM/dt) / (Q + dQ/dt)) *Vy – P (13)

If there is no price change,

(dP/dt = 0). Then:

P=1 =

(My + dMy/dt) / (Q + dQ/dt) *Vy (14)

Suppose Vy =

10, My=100, Q= 1000/year

and P=1.

If dMy/dt changes

by 20, to maintain P=1, dQ/dt must

change by 200 because from equation (14)

P =

(My + dMy/dt) / (Q + dQ/dt) *Vy (14)

1 = (100+20) /

(1000+200) *10

At

constant price and speed of circulation, producing 20% more goods requires 20%

more money, that is, wages and incomes. Changes

in productive transaction account money My and output Q are always

and necessarily proportional when P and Vy are constant.

If, on the other hand, there

is an annual 10% increase in prices, (dp/dt = 10%/ year), to get the same rate

of output at the end of the year requires:

P =

((My + dMy/dt) / (Q + dQ/dt)) *Vy (14)

1.10 = (100+31 ) /

(1000 +200) *10 at year end

1.10 = (131) / (1200) *10 at year end

The Fisher equation presented

here is a macro-economic snapshot at a point in time. At the end of the year

the goods in the example are being produced at the rate of 1200/year

when the productive transaction account money supply is 131 (instead of 120)

and prices are 10% higher than the previous year. However, the situation over

any period is dynamic, not static. All the variables are increasing over time

so they have to be “averaged” over the period in question when using the annual

output measure of GDP.

In the example, at the end of

a full year when P=1.1, there is then a rate of production 1200/year. During

the year, 1100 goods,[(1000+1200)/2],

have been produced at an average transaction account money supply M of

115.5 [(100+31)/2] and a linearly averaged price of 1.05 as shown below:

P =

(My + dMy/dt) / (Q + dQ/dt) *Vy (14)

1.05 = (100 + 15.5) /

1100* 10 averaged

and:

GDP (PQ) = My*Vy

1.05*1100

= 115.5*10

1155 = 1155

The real annual GDP is

therefore 1155, (1100*1.05), produced at an average price of 105 using an

average productive transaction account money supply of 115.5. In that case, the nominal GDP increase is

155, (1155- the production rate at the start of the year, 1000) or 15.5%.

In the present system of

national accounts (SNA) the “inflation” of 10% of 1000, (100), would be

deducted from the nominal GDP growth, (155), leaving just 55 as measured “real

growth” instead of (in the example) 155- 50, (5% of 1000), or 105.

In current practice, the

aggregate GDP measured over time represents the

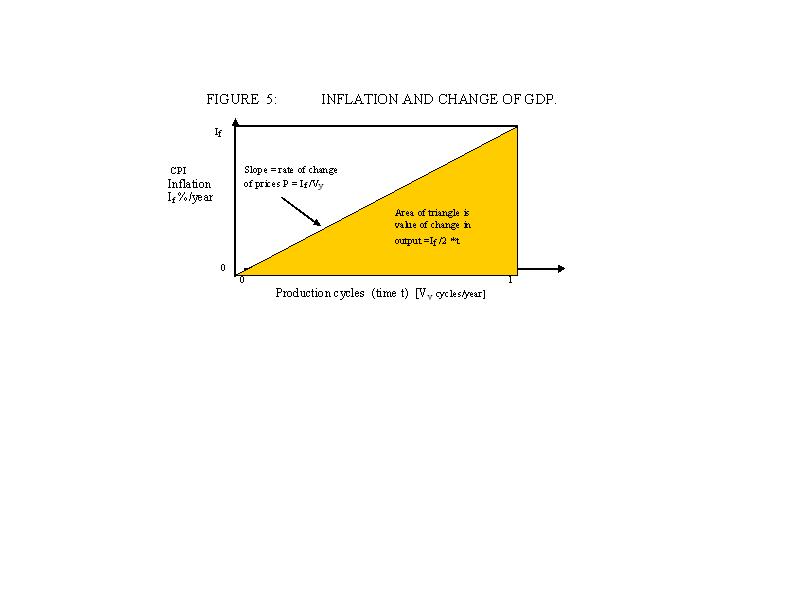

The need to “average” price P can also be shown diagrammatically, as in Figure 5., where the

increase in nominal GDP is the increase in the monetary value of economic output

over a period of time whereas the CPI is the (arbitrarily determined) price level

at any given time. In Figure 5 the GDP value of

the price change If%/year over time t is the area If*t/2,

so that:

{kind=link}

% GDP value change = If*t/2 (15)

A CPI

consumer price inflation rate of 2% over time represents a1% inflation in the

aggregate value of goods and services produced during that time, not

2% as is universally assumed. The standard practice of subtracting a percentage rate of CPI inflation from

the nominal growth in the value of GDP output over any given period is therefore

incorrect.

[Figure 5 :

Inflation and change of GDP.]

Even when prices P are arbitrarily

constrained, much greater changes in GDP would be possible if aggregate

incomes were allowed to rise (such as by getting unemployed workers back to work).

The failure to increase incomes proportionately to output is ideological. If

P=1.05 and Vy = 10 as in the example above and production Q is increased to

1500, then:

P =

(My + dMy/dt) / (Q + dQ/dt) *Vy (14)

1.05 =

(100 + 57.5) /

1500 * 10 averaged

Prices P remain the same but there

is a 36% increase in incomes (42/115.5) and a 36% increase (400/1100). There is

no reason why economic output cannot be increased to make use of all the available

economic resources without causing systemic

inflation as long as deposit interest is close to zero and the money supply

increases in proportion to output.

Austerity policies around the world

have failed so dismally because they have arbitrarily suppressed aggregate

incomes, leading to the decay of accumulated non-inflationary growth shown in Figure 4.

MEASUREMENT OF PRODUCTIVITY.

True productivity increases, which

are not typically accompanied by an increase in the money supply, can worsen the measured economic output

because they reduce prices. They are deflationary. Inflation, on the other

hand, increases prices P and the money supply M, not the amount of goods

Q.

There can be no increase in Q unless

there is more production. If the given total work hours and productivity

remain the same, Q must be the same whatever the price level may be. For Q to

increase there must be either more work hours or plant (more labour or capital)

and/or an increase in productivity (more goods and services produced with the

same number of work hours and capital input).

Applying the Fisher equation, a productivity

increase of 10% without an increase in the money supply will cause a fall of

9% in prices:

P =

M / Q *

V

P = ((My + dMy/dt) / (Q + dQ/dt)) * Vy (14)

0.909 = (100 +0) / (1000 +100) * 10 (productivity)

An increase in production resulting

from a population increase of 10% adds 100 to the rate at which output Q is

being produced. To avoid inflation and keep P=1, the money supply would have to

be increased by 10% to 110 because the production increase is monetised (unlike

the productivity gain above which is not monetised) :

P =

((My+ dMy/dt)

/ (Q + dQ/dt)) * Vy (14)

1.0 =

(100+10) / (1000+ 100) * 10

(production)

Suppose now the population increases

by 10% at constant work hours per person and there is also a 10% rise in productivity.

Adding the concurrent effects of

both the 10% productivity increase and the extra production from the 10%

population increase gives:

P = ((My

+ dMy/dt) /(Q +

dQ/dt)) * Vy (14)

0.909 =

(100 +0) / (1000 +100) * 10 (10% productivity)

1.0 = (100+10) / (1000+ 100) * 10 (10% population)

Solving the combined effects of the

10% productivity gain plus the10% increase in production resulting from

population change for price P:

P = ((My + dMy/dt) /(Q + dQ/dt)) *Vy (14)

P =

(100+0+10) /(1000

+100+100) * 10

0.917

= 110 / 1200 * 10

While increases in monetised production

are nominally isolated by measuring GDP output and prices P, as previously

discussed, real productivity increases are not automatically measured in

official output statistics because they are usually masked by price reductions.

In the case of the 10% productivity

increase on its own in the above example, the price level is 9.1% lower [(1-0.909)*100].

When the increased productivity is combined with the concurrent increase in

monetised production due to the 10% population increase, the price level P is

still 8.3% lower [(1-0.917)*100] than it was before the two increases occurred.

To maintain prices P=1.00 with a productivity increase of 10% and a concurrent

population increase of 10% the money supply would have to be increased from 110

to 120 as shown below.

P = (My + dMy/dt) / (Q + dQ/dt) * Vy (14)

1.00 = 120 / 1200 * 10

Orthodox

measurements of GDP and “productivity” fail to reflect real increases in

productivity contributions to output Q. They also miscalculate the measured

monetised growth, as previously discussed. GDP measures the combined PQ side of

the original Fisher equation while disregarding the MV side of the equation.

Using half the Fisher equation for measurement purposes is mathematically

insupportable.

Orthodox methodology determines the

price level P by surveys of consumer prices that are then weighted to produce a

hypothetical average consumer price called the Consumer Price Index (CPI),

which is then used to indicate the price level P contributing to the GDP (PQ).

In orthodox economics and the system

of national accounts (SNA), productivity is typically measured as the increase

of total output PQ for each unit of input (capital and labour), not the

increase of production Q itself, even though the physical increase in production

in many sectors is known and could be used as the basis for accurate

measurement. For example, the primary industries, manufacturing, tourism, but not,

in general, service industries and government, despite attempts to measure

quantitative outputs. The definition and methodology of “productivity” measurement can be found for

This fatal mistake dramatically

affects the entire system of national accounts and the measurement of economic

success in the world economy.

According to the relevant

“productivity” statistics for

If measured “productivity”

PQ/hour rises by 2% and measured price inflation P is, say, 2%, the effect of

that inflation in P of 2% has to be deducted from the real productivity

increase discussed above. The calculation below shows there would then be an

“inflation- free” productivity increase in Q of 0% instead of 2%. Using the

Fisher Equation, the 2% measured “productivity” increase in the rate

of output PQ is really made up of 2% inflation and 0% productivity

gain.

In that case:

P% = My% /Q%*Vy (Vy is held constant at 1.0) (10)

1.00 =

1.00/1.00 * 1.0 (the effect of a 0% productivity gain)

1.02 = 1.02/1.00 * 1.0

(plus the effect of 2% inflation)

1.02 =

1.02/1.00 * 1.0 (total P%*Q% from both effects = 1.02)

Defining productivity

increases in PQ/hour does not necessarily create real increases in output Q.

Assuming they do so automatically is nothing less than wish fulfilment. The

whole concept of improving productivity is increasing Q/unit input (labour and

capital), not the total output PQ.

In practice, CPI inflation in

The measured “productivity”

increase in the example below is a myth.

Using the Fisher equation (10)

again to illustrate the above example:

P% = My %/ Q% * Vy (Vy is held constant at 1.0)

1.02 =

1.02/1.00 * 1.0 (the effect of 2% inflation)

1.00 =

0.99/0.99 * 1.0 (plus the effect of a -1% productivity gain)

1.02 =

1.01/0.99 * 1.0 (total P%*Q% from both effects = 1.01)

Aggregate

changes in production Q can be assessed when output PQ and the price level P

are both known, but productivity changes can only be assessed using both sides

of the Fisher Equation of exchange.

The

relationship between the author’s debt model, inflation and GDP.

As set out in the author’s

papers referred to in this article, the payment of interest on debt in the

debt-based financial system creates systemic

inflation that forces up the productive transaction account money supply My.

In the debt system, if My did not rise, the financial system would

collapse because incomes in the productive sector are continually being

transferred from income earners to deposit holders. The immediate effect is to

reduce the purchasing power of income earners so they literally cannot buy the

goods and services they have produced. Hypothetically,

deposit holders (“savers”) could buy the excess goods and services but that

doesn’t happen because of the “incentive to save” referred to earlier in the

article and because “savers” alone cannot physically absorb the surplus. Instead, in

aggregate, households and businesses are forced to take on the new Ms

debt, which is the systemic inflation arising from net after tax deposit

interest paid on the Domestic Credit (DC) plus

interest paid on secondary debt NBLI, (Nb). The additional servicing

of that additional debt load Ms is a primary cause of increasing

income inequality around the world. In practice, if Ms in the debt

model (equation 3) increases at 4%/year the money supply My in

the productive transaction accounts must also increase by at least 4% assuming

speed of circulation Vy and price level P remain constant as shown

in the examples above.

Equation (9) on page 9 tells a

big story. Stripping out foreign debt and the bubble D b (that is,

in the special case where Dnfca and Mb are both zero),

for the reasons set out on page 9:

[GDP] =

Ms + Dni + R (9)

In the special case of

equation (9), if Ms did not grow, nominal GDP growth would be

largely determined by the monetised value of non-inflationary growth Dni.

For the change in Ms to be zero, deposit interest rates must also be

zero. Since, as already explained above, that is not possible, there will

always be some increase in Ms and therefore some systemic inflation.

That applies whether the financial system is based on bank debt or on Savings

and Loan (S&L) debt.

The main difference between

bank debt and S&L debt is that in the latter case the bank Residual (R)

does not grow as quickly. The innermost secret of the debt-based capitalist

system is laid bare for all to see.

The

net unearned interest income Ms is a fundamental baseline of nominal

GDP growth as shown on Figure 2. Adding less than Ms to the credit aggregate

DCm must contract the measured economy.

Excess

non-productive debt produces excess deposits that typically increase M3 and

systemic inflation as well as inflating non-productive investment sector

prices. As shown above, additional debt-free cash-based purchasing power

introduced to the productive system over and above systemic inflation produces

real growth as long as there are sufficient available human, natural and

physical resources available to the productive economy. That growth is generated

by more hours worked, such as by increases in the working population, reduction

in unemployment, and longer working hours, while the additional contribution of improved productivity can be best

measured by physically measuring the physical quantity of Q/hour, not PQ/hour.

Within the framework of a

capitalist system any monetary reform proposal must introduce more

money into the system (even if it is introduced debt-free) before monetised

“growth” as it is currently measured can occur and, in the relative

absence of traditional bank loans, most of that new money must be on-loaned at

interest through S&L interest-bearing accounts to fund the investment

sector. In the various monetary reform proposals the interest paid on the

S&L accounts will still generate an exponential growth in Ms and

some systemic inflation. Both could, in theory, turn out to be greater than

they are today unless they are carefully managed.

It is

impossible to “produce” a higher GDP (PQ). It is only possible to produce more

(or fewer) goods and services Q. Too much new money Mv will create

inflation. Too little money will induce systemic collapse. The balance in the

productive sector is sensitive because the dynamic productive transaction

account balance Mv is just a few percent of GDP. My

presently circulates (at least in New

The

debt model (equation (3), Figure 2) provides an extremely simple way to match systemic

inflation and non-inflationary growth with extra output enabling GDP to be

increased at near-constant prices.

The difference between

systemic inflation and measured CPI inflation in the present financial system

reflects on-going suppression of wages and incomes. Governments have suppressed

economic “growth” because inappropriate orthodox inflation targeting in the

presence of systemic inflation Ms has meant that incomes have been

unable to grow fast enough to absorb existing output let alone increased

potential output. With the single exception of 1995, systemic inflation in

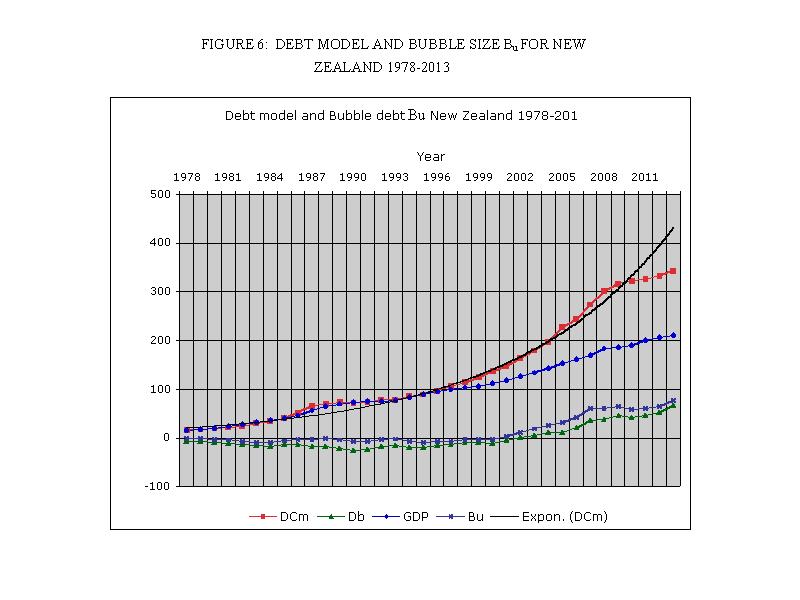

Figure 6 shows the debt model

(Figure 2) solved to obtain a preliminary estimate of the bubble debt Db

in equation (5) for

M3 = [Dmy+ Ms +Dni

+ Db] (5)

Figure

6 shows that orthodox monetary policy bears little relationship to the

mechanics of the debt-based economy. The non-bank debt Nb has to be

added to the bubble debt Db to get the bubble value Bu in

Figure 6 because Figure 6 is based on the total debt

DCm whereas Db is derived from the equation for DC. There

are discernable (quantifiable) bubbles relative to the trend curve of Bu

in

Bubble value Bu

= Db

+ Nb (16)

On

the basis of the preliminary analysis in Figure 6 the 2009 bubble Bu does not appear to have unwound and M3

growth is out of control. That means the Reserve Bank of New Zealand is right

to be concerned about rising prices in the investment sector in New Zealand

because they too appear to be out of control.

The exponential rise in

systemic inflation Ms is inexorable.

It is unlikely that the 2005-2009 debt bubble in

[Figure

6 : Debt Model and Bubble Size Bu for New

Zealand, 1978-2013.]

The bubble debt has been calculated from equation (5) as Db=

M3-(Dmy + Ms+Dni). The separation of (Dni + Db) into Dni

and Db needs further research. For Figure 6 it has been

obtained as the difference between the measured nominal GDP increase and the

change in (Ms+R).

The role commercial banks play

in the capture of GDP has never before been revealed. The banks capture economic growth from the

community at large as shown on Figure 4. Hence equation (9):

[GDP] = Ms + Dni + R (9)

Where:

Ms = Systemic inflation

Dni =

Non-inflationary growth

R = Bank residual captured from GDP.

Figures 4 and 6 indicate that

unless the exponential growth of the model systemic inflation (Ms)

is halted, the

CONCLUSION.

This paper hints that the

Exponential debt-growth and

productive sector inflation are synonymous with capitalism. This point is

discussed at length in the author’s paper Capital is Debt.

Governments and economic policy

makers have striven to make square policy pegs fit round economic holes

subjecting the world and its people to boom and bust cycles with immeasurable

consequences.

This paper suggests that sound

monetary management can produce dramatically better economic outcomes

worldwide. To do so will mean abandoning the myths about inflation, growth, and

monetary mechanics that underpin orthodox macroeconomic policy and at the same

time fail to satisfy the basic accounting equation.

Abandoning those myths will mean:

-

strictly managing cross border capital flows using

powerful tools such as a Foreign Transactions Surcharge.

-

using the revised Fisher equation of exchange

(equation (3) outlined in this paper (or similar) to enable the money supply to

be properly aligned with potential economic output.

-

introducing broad monetary reform such as the Manning Plan (or similar) to keep

interest rates as close to zero as possible.

-

constraining secondary debt growth as the use of

interest-bearing bank debt is phased out in the course of implementing monetary

reform proposals.

-

ensuring that the macroeconomic model chosen satisfies

the basic accounting equation at all times.

-

abandoning the methodological fallacies in the

calculation and use of the CPI inflation index and GDP calculations.

-

introducing a valid methodology to measure and account

for true increases in productivity and/or production.

Bubbles occur in the investment sector due to uncontrolled debt growth Db

while, at the same time, the productive sector is suppressed through arbitrary

orthodox macroeconomic policy settings. The debt bubbles have occurred because

of fundamental misconceptions about the way the financial system works.

Lowell Manning,

Wellington,

07 July, 2013.

Summaries of monetary reform

papers by L.F. Manning published at http://www.integrateddevelopment.org.

Chicago Plan Revisited Version II: An insufficient

response to financial system failure. (Posted 11 May, 2013.)

Comments on the IMF (Benes and Kumhof) paper “The

Chicago Plan Revisited”.

Debt bubbles cannot be popped : Business cycles are policy inventions.

DNA of the debt-based economy.

General summary of all papers

published.(Revised

edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

The Manning plan for permanent debt reduction in the national economy.

Measuring Nothing on the Road to Nowhere.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

"Money

is not the key that opens the gates of the market but the bolt that bars

them."

Gesell,

Silvio, The Natural Economic Order, revised English edition, Peter Owen,

![]()

This work is

licensed under a Creative

Commons Attribution-Non-commercial-Share Alike 3.0 Licence.