NGO Another Way (Stichting

Bakens Verzet), 1018 AM

SELF-FINANCING,

ECOLOGICAL, SUSTAINABLE, LOCAL INTEGRATED DEVELOPMENT PROJECTS

FOR

THE WORLD’S POOR.

|

FREE E-COURSE FOR DIPLOMA IN

INTEGRATED DEVELOPMENT |

|||||

|

Downloads (updated 03 October 2011) |

Edition 01 : 23 October, 2014.

HOW THE WORLD’S POOR CAN IMPROVE THEIR QUALITY OF

LIFE AND MEET THE MILLENNIUM DEVELOPMENT GOALS.

PRACTICAL MONETARY REFORM.

(Stichting Bakens Verzet has

endorsed the Earth Charter.)

Return

to : Stichting Bakens Verzet Homepage.

BEYOND PIKETTY: THE ANATOMY OF

INEQUALITY

By

Sustento Institute

Version 4: 22 October 2014

CONTENTS.

1. Executive

Summary.

2. Introduction.

3. The “Golden

Rule” and the Fundamental Laws”

4. Verifying

Piketty’s “first law”.

5. Verifying

Piketty’s “second law”.

6. Reconciliation

of growth, saving and inflation.

7. What is

“capital”?

8. Inequality and

bubbles

9. Conclusions.

10. References.

Acknowledgement:

The author

acknowledges the invaluable input and editing by Terry Manning, NGO Bakens

Verzet Holland www.integrateddevelopment.org

1. EXECUTIVE SUMMARY

This paper

establishes the source of inequality using Thomas Piketty’s recent book

“Capital in the Twenty-First Century” as a reference point.

Saving as measured in each country’s national accounts

has a growth component and an inflation component.

The source of systemic inequality

is the inflation component of Saving plus bubble debt.

Systemic inequality

is defined by a set of 8 macroeconomic accounting principles:

1. The present

(reflated) value of all past real growth ∑gr is the Gross

Domestic Product, GDP.

2. The present

(reflated) value of all past saving ∑sr is the produced

tangible wealth as measured in each country’s national accounts.

4. The value of total wealth is the present

value of all past saving imputed by market transactions to include intangible

and non-produced wealth.

5. The sum of

existing (non-reflated) outstanding productive investment principal ∑P is

the Gross Domestic Product GDP.

6. Outstanding

investment productive principal ∑P = the present reflated value of all

past real growth ∑gr =

GDP.

8. Using Piketty’s

terms, numerical inequality will decrease only when the rate of

return “r” on the national capital falls below the real economic growth rate

“g” divided by the ratio “β” of national capital (national wealth) to

national income.

Inequality is

endemic to capitalism and debt-based economies.

Wealth is

transferred upward through the deposit interest rate mechanism whereby the net

interest paid by original debt holders under their debt contracts finds it way

as unearned income to current deposit holders’ accounts. That unearned income

is funded from nominal GDP growth and confers higher values on all traded national capital, not just its

income producing portion. That is what increases inequality.

Reversing that

structural inequality under the present system requires (r<g/β), or, in

simple terms, that capital “runs at a loss” even when deposit interest is zero.

The capital (wealth) base would then gradually deflate without affecting

economic growth. This would not be capitalism as it is presently practised

because new wealth would then tend to be distributed according to earned

income.

Housing remains a core issue within the

capitalist system worldwide because most domestic housing is economically

unproductive. Its capital cost can only be repaid over time out of increased

productivity passed on to income earners. Each expensive new house built means

part of a factory or farm or other productive enterprise might be lost.

Building expensive houses instead of cheaper ones has produced a wealthy

over-housed minority and a poor under-housed majority. The same argument

applies to public infrastructure, services and transfers.

The tax reforms Piketty

proposes in Part Four of his book would reduce inequality much as happened when

the “U” shaped wealth profiles were formed in some countries during the 20th

century (as shown at Figure 4.5 of his book). The reforms did not prevent the

revival of capital inequality as their effects were whittled away over time.

The reforms failed because the crucial roles credit creation and public policy

play in income and wealth distribution have been neglected in recent decades.

Rising structural inequality suggests that the

financial system itself needs to be modernised. There are several viable

options available, including combinations of “bottom up” local currency

proposals where the local currency can be used to pay taxes, “top down” approaches based on interest-free

public money, and much broader use of cooperative economic activity.

This paper also shows that the “fundamental

laws” Piketty proposes in his book do not withstand scrutiny. There is no

causal link between income and wealth inequality measured by Piketty’s ratios

(β= national capital/national income) and his two productive sector

ratios, (β= s/g (savings/accumulated growth)) and (β = α/r),

where “α” = the ratio of annual capital income to annual national income”

and “r” = the annual rate of return on capital.

2. INTRODUCTION

Piketty’s book “Capital in the Twenty-first Century”

is primarily a study of inequality. The heart of his book and his “laws” (as

further defined below) is that the percentage (r-g) gives rise to a

capital-based unearned income that is surplus to the monetary requirements of

the productive economy.

The equations from

Piketty’s book are applied to official economic statistics for

Piketty’s own data

set for

“Capital in the

Twenty-First Century” is founded on three concepts. These are:

1) A so-called

“golden rule” (r>g) where “r” is the

percentage (%) annual rate of return

on capital (national wealth net

of debt, as Piketty defines it) [p50] and “g” is the real growth rate of annual

economic output (Piketty uses National Income instead of Gross Domestic Product GDP) as measured by

the international System of National Accounts (SNA).

2) A “First Fundamental Law of Capitalism” (α= r

x β) where alpha “α” is the ratio of

annual capital income to annual national income given as a percentage,

“r” is the percentage annual rate of return on capital, beta “β” is the

ratio of national capital (national wealth, as Piketty defines it) to national

income [p52].

3) A “Second Fundamental Law

of Capitalism” (β= s/g) where beta “β” is as already defined, “g” is

the accumulated “long run” annual real growth, (apparently stated as an annual

percentage), and “s” is the accumulated “long run” savings which appears to be

the “ net savings rate” derived from the national accounts (also apparently

stated as an annual percentage) [p166].

A) Referring to

Piketty’s indicator (β= s/g) (as defined above):

The long-term

productive sector ratio (s/g) for

The paper shows

that Piketty’s ratio (s/g) is a

measure that reflects the relationship between prices and output in the productive economy. Asset prices are

defined by the aggregate physical transfer of Saving “s” from the productive

economy to the non-productive investment sector as shown in Figures 2,4,7,and

13.

B) Using Piketty’s

indicator (β = α/r) (as already defined above):

In Figure 8, the

annual rate of return on capital “r” from Piketty’s equation (r=α*g/s) is

compared with an actual estimated rate of return on capital for

The result shown in

Figure 8 suggests there is little or no relationship between the calculated

annual rate of return on capital using Piketty’s equation and the actual rate

of return for

3. THE “GOLDEN RULE” AND THE “FUNDAMENTAL

LAWS”

“The Golden Rule”

Piketty says the

“Golden Rule” (r>g) is “the central thesis

of this book” [p77] because “an

apparently small gap between the return on capital and the rate of growth can

in the long run have powerful and destabilizing effects on the structure and

dynamics of social inequality”.

Piketty neglects

debt (and money) in his book altogether except during a brief discussion on

public debt (pp. 547-552). That neglect is fatal to his thesis.

Plainly, Pikkety’s

“net” investment return (r – g), applied to market activity in the productive

sector, will inflate asset prices if it is positive. It will do so

because “r”, the annual percentage (%) rate of return on net national wealth as

Piketty defines it [p50] on the one hand, and “g”, the annual real growth rate of economic

output (Gross Domestic Product or GDP- Piketty uses National Income-) as

measured by the international System of National Accounts (SNA) on the other, both give rise to exponential functions

over time. For example, if “r” were 7%/year, $1000 of wealth would increase

to $2000 over 10 years. If on the other hand “g” were 3.5%/year, it would take

20 years for $1000 of “g” to increase to $2000.

The historical “r” and “g” curves will therefore diverge rapidly. That

divergence is the primary indicator of growing inequality.

This paper shows in

detail that the only way to avoid asset price rises in the capitalist system is

for the numerical after-tax rate of return on capital to be well below the real

economic growth rate “g”. That, however, is the antithesis of capitalism. Asset inflation and exponential wealth

expansion are therefore inherent in the capitalist system unless capital

(money) is physically destroyed for example by bank failures, as happened

during the great depression of the 1930’s.

When “r” is greater

than “g” (r>g) the financial system is subject to inflation and investors

may typically be able to accumulate surplus deposits over and above those

resulting from economic growth. Piketty does not tell us how the increase in

investment sector deposits creates the redistribution of wealth to investors

from the rest of society but his “golden rule” is a good indicator a transfer

is happening.

Describing how the

transfer actually takes place calls for an understanding of the dynamics of

debt-based financial structures and of “saving”.

The saving “s”

Piketty uses is the “net saving” from the national accounts using the System of

National Accounts (SNA). It is supposed, according to Piketty, to fund the net

increase in physical capital assets at cost resulting from the growth of

economic output (Gross Domestic Product or GDP). This paper shows that the aggregate saving

“s” in the national accounts is less than the aggregate nominal GDP growth

because the national accounts wrongly deduct consumption of fixed capital from

gross capital formation whereas the actual financial flows, being the

repayments of principal on outstanding productive sector debt, should instead

be used.

The expressions

(r-g) and the “golden rule” (r>g) ultimately refer to inflation although

Piketty does not seem to be aware that is so. Figure 1 shows the actual

accumulated numerical figures ∑s for saving “s” and ∑g for real

growth “g” for

The inflation transfer mechanism makes the curves for

“s” and “g” in Figure 1 diverge.

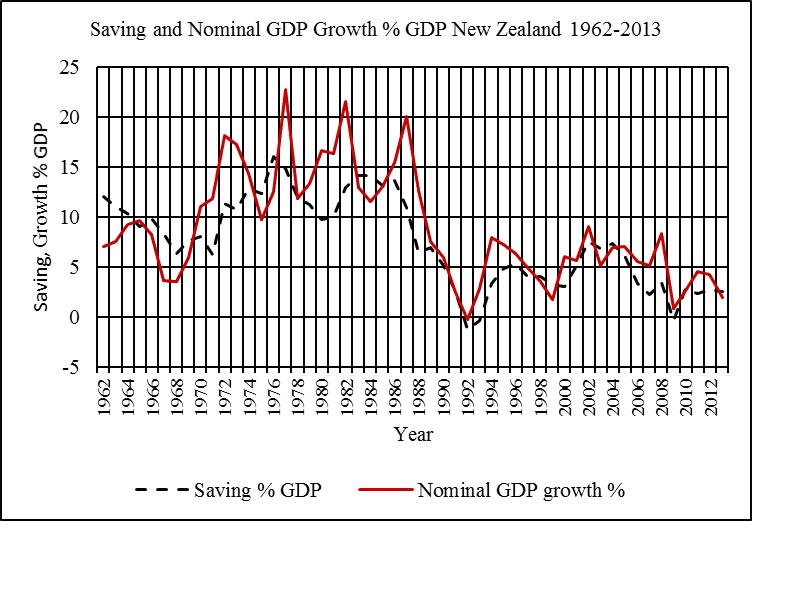

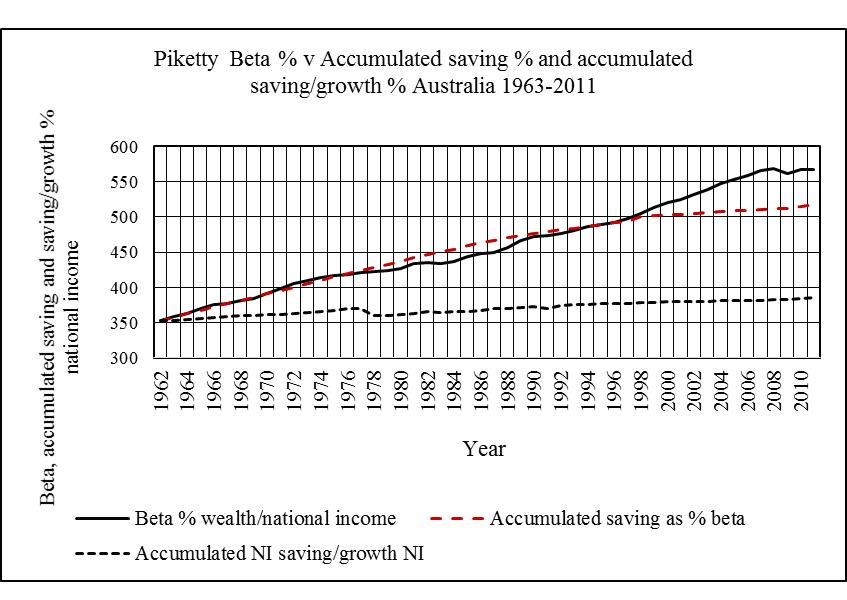

Figure 1. Accumulated “s”

and real GDP growth “g” New Zealand 1962-2013.

{kind=link}

Piketty’s “First Fundamental

Law of Capitalism” (α= r x β)

Piketty himself

says the “first law” is a tautology (p52). (Capital Income/ National Income = r

* net national wealth / National Income) says (Capital income = r * net

national capital (wealth)) because the national income cancels out from each

side of the equation.

The “first law”

states that income from capital is the [capital base (net national capital or

wealth as Piketty defines it)* the average annual rate of return “r” (or

“yield”, p52, on that wealth.)] The “first law” fails to link the productive

economy properly to the investment sector even though productive sector incomes

must be used to physically pay the capital income represented by “r”. The

non-productive investment sector does not produce anything itself and Piketty

(p45) makes abundantly clear that rentiers historically didn’t work and that

their (unearned) income came from their ownership of wealth.

Figure 2 shows

measured national account SNA “Saving” “s” plotted against nominal percentage GDP growth for

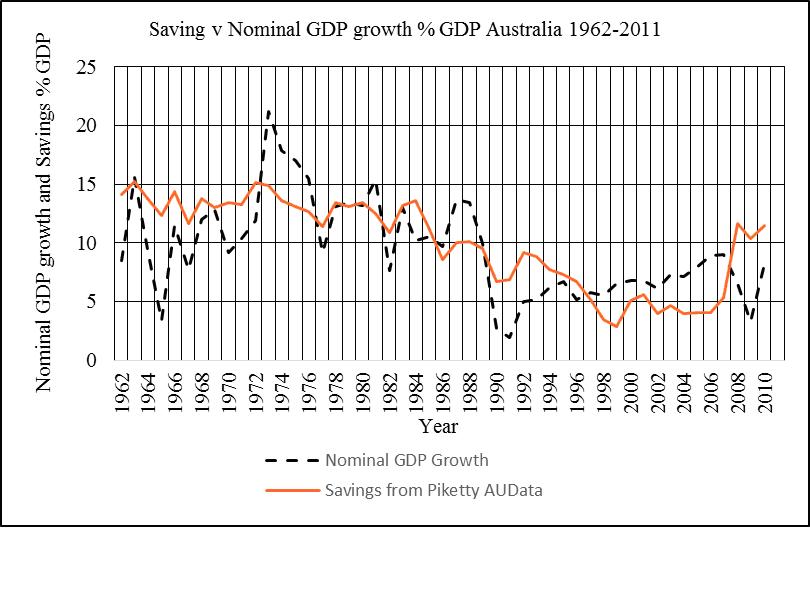

Figure 3 shows the

same for

That new debt

causes the inflation that creates the wealth inequality seen around the world.

Figure 2. Saving and

Nominal GDP Growth as % GDP New Zealand 1962-2013.

{kind=link}

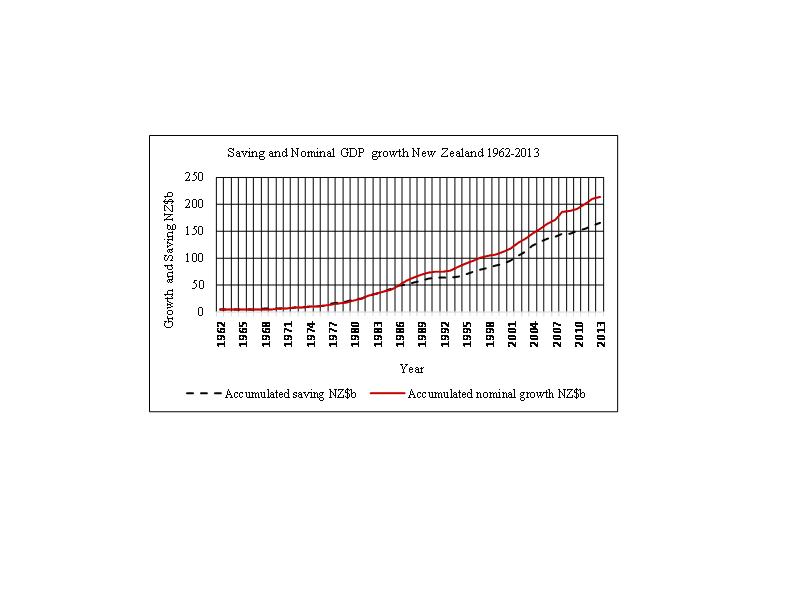

Figure 4 shows the

accumulated data for nominal GDP growth and saving “s” from Figure 2 for

Figure 3.

Saving and Nominal GDP Growth as % GDP

Australia 1962- 2011.

{kind=link}

Source: Piketty

Zucman dataset

Figure 4. Accumulated Saving and nominal GDP growth : New

Zealand 1962-2013.

{kind=link}

Source:

When the Saving

figure as shown in Figure 2 is (arbitrarily) corrected for New Zealand by about

23% to cover the difference between the (higher) physical capital repayment

flows and the (lower) rate of depreciation (consumption of fixed capital) used

in the SNA accounting system, the GDP and outstanding investment principal

curves fall on top of each other as is shown conclusively in Figure 5 for New

Zealand.

GDP is therefore

the sum of outstanding investment principal.

Figure 5. Outstanding

investment principal v GDP New Zealand 1962-2010.

{kind=link}

Sources:

The Savings Myth (http://www.integrateddevelopment.org/lowellsavingsmyth20110522.htm ;

The

DNA of the debt-based economy http://www.integrateddevelopment.org/lowellDNApaper20110805.htm

An independent test

for “r” is to compare the figures for (rdt = αdt/β)

derived from the “first law” in Piketty’s (Piketty-Zucman data) Table 3b with

the formula (rdt = αdt* g/s) which is derived as

discussed below. The “saving” in the productive sector that funds

non-productive investment relates directly to the growth of productive sector

debt required to fund the net after-tax interest on the country’s deposit base.

[Manning 2011a, Manning 2013a]. This

means that while (r>g) may indeed be an indicator

of divergence between net national capital and national income it cannot

numerically define it. This is shown

beyond doubt in Figure 7 below.

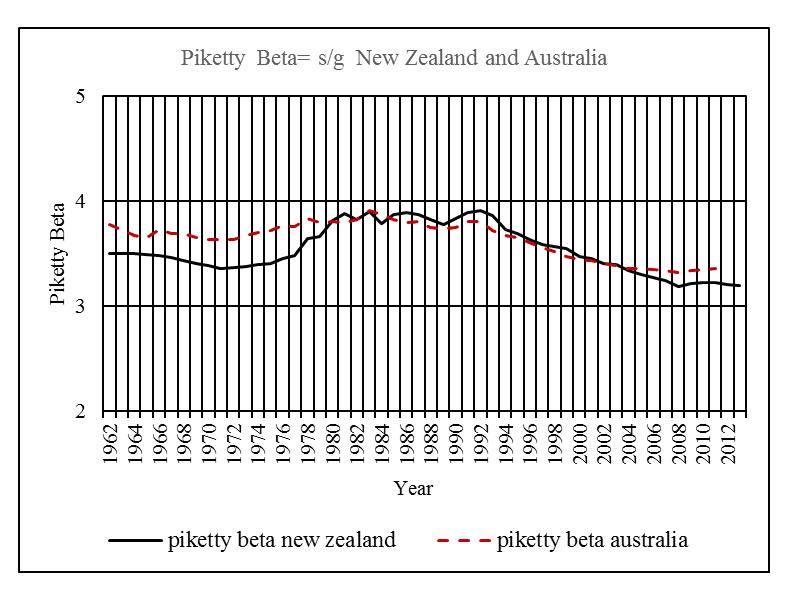

Piketty’s “Second Fundamental Law of Capitalism”

(β= s/g)

Piketty discusses

his “Second Fundamental Law of Capitalism at some length [pp 168-176]. The

second “law” says that (β= s/g) where beta “β” and “g” are as already

defined and “s” is the “savings” (net after tax) from the national accounts

[p166].

Piketty’s effort to

link the productive economy to wealth as he defines it is confused. For

Piketty, national wealth includes the “stock” of the current monetary value of

every investment asset, and he lists those at several points. He divides them

into farmland + housing + other domestic capital (both private and public) +net

foreign capital. At page 47, Piketty

says natural resources such as “petroleum,

gas, rare earth elements, and the like” are included in that capital, but

he does not focus on the difference between the wealth itself (the assets) and

the monetary “value” given to those assets.

He further confuses

his definition of wealth when he writes [p196] that “By definition, the law (β= s/g) applies only to those forms of

capital that can be accumulated. It does not take account of the value of pure

natural resources, including “pure land …”.

Farmland is

apparently not “pure land” “prior to any

human improvements.”

As discussed below

for

Piketty defines the

annual rate of return on capital or yield “r” as a net % return “over

the course of a year” [p52]. His dataset for

Although Piketty

talks about his second “law” (β= s/g) throughout his book, his own work

shows it to be false. His Table 5a [Piketty-Zucman Wealth-Income data Set

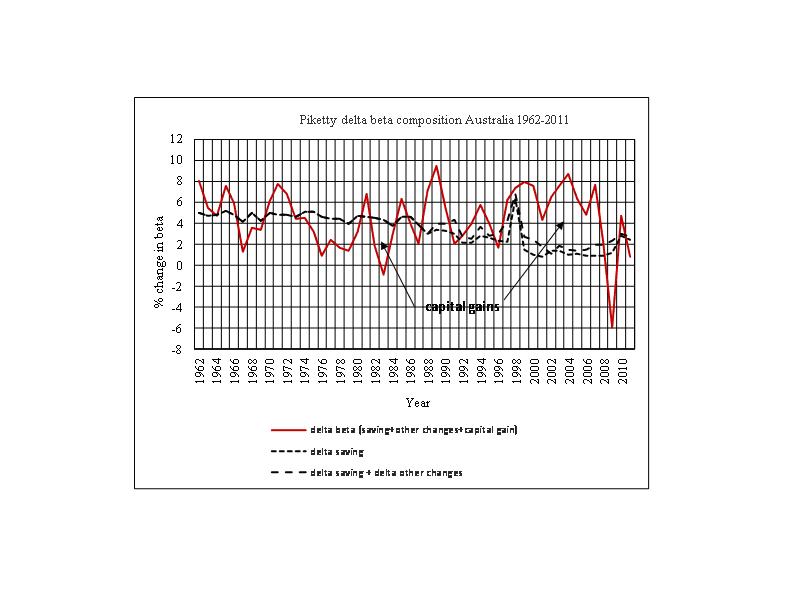

∆β

7.5% =

0.3% (gwst from saving)

+ 1.4% (Ot ) + 5.9% (qt

).

In other words,

almost none of the change in “β” in

Piketty claims his

“second fundamental law” has to be applied over the long term. Figure 7 shows

“β” from Figure 6, the growth in “β” from savings “gwst”

from Figure 6 and accumulated “st/gt” also from Figure 6 accumulated

over a half century.

Figures 6 and 7 use

Piketty’s own data. They confirm the work of the author of this paper and show

that Piketty’s own “laws” are wrong.

Figure 7 shows the

changes in “β” are related to savings “st” not to

the change in savings/growth (st/gt).

Allowing for the

issues already discussed for

In aggregate

people have to “save” some of their income even in the absence of growth to pay

for the “hand held out at the market gate” [Manning 2013b]. That seems to have

happened in

Figure 6. Composition of ∆β

- Australia 1962-2011 (Piketty Table 5a).

{kind=link}

Figure 7. Piketty’s %

increase in “β” related to % increase in Saving and % increase in

Saving/Growth- Australia. 1962-2011.

{kind=link}

In

a debt-based system, central bank policy to manage inflation by raising

interest rates reduces the demand for new debt (because the price of debt

rises) while at the same time transferring more purchasing power from

consumption in the productive sector to the investment sector through systemic

inflation [Manning 2011a].

Existing asset prices rise only until investors

withdraw from active non-productive investment as the passive interest return

on deposits increases. At that point the price of investment assets falls and

debt cancellation through physical repayment, business failure and household

default begins. Changing interest rates have a similar effect on investment

markets as major world events do: they cause a shift in the mix of active

investment in relation to properties, equities and bonds that can lead to

systemic collapse in both the productive and investment sectors.

The resulting

additional SNA “saving”, part of “s”, accruing from the higher interest rates

is dissipated in inflation in both the productive and the investment sectors and

the consequent reduction of consumer demand and productive investment typically

causes

an accompanying recession. If that

failure were to continue over a lengthy period without new debt creation there

would soon be little money left in the productive economy and few productive

assets left. That is what happened during the 1930’s depression. To avoid

deflation in the productive economy the money supply would have to be increased

through higher government spending or some other stimulatory monetary policy as

has happened recently around the world through quantitative easing.

Piketty fails to

address these financial system mechanics even though they form the basis for

establishing asset “values” under his “second law”.

4. VERIFYING THE FIRST LAW

The two “laws”

(β=s/g) and (α= r * β) are not truly independent because (from

(s/g=a/r) they give other forms like (r=α*g/s).

These derived

relationships are at the heart of Piketty’s suggested long term decline in the

rate of growth in developed countries though he does not prove them. The

decline in the rate of economic “growth” has a far simpler explanation related

to the increasing proportion of services in developed economies. It is much

harder to increase productivity in services than it was to increase industrial

productivity during (say) the industrial revolution, while increases in

bureaucratic complexity and compliance costs often lower quality of life

instead of improving it.

Consider

(r=α*g/s) in Figure 8, using “α” = 30% , indicated by Piketty as a

typical value for it [p53].

Mathematically, the only time “g” can be 0 is if (r=0) or (s/α =0).

However, Piketty is not working “mathematically”, because he considers “s” and

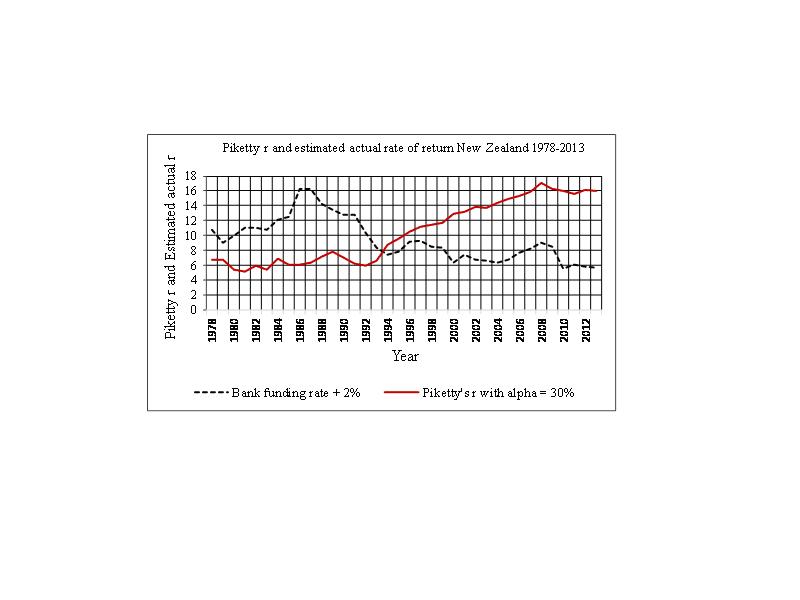

“g” to be aggregates accumulated over the long term. Figure 8 shows Piketty’s

“r” compared with an actual estimate for it (using the bank funding rate + 2%)

calculated from the aggregated dataset for

Figure 8. Piketty’s “r”

compared with Actual rate of return, “r”, New Zealand 1978-2013.

{kind=link}

Piketty’s “r” in

Figure 8 is derived as (r=α*g/s) from the accumulated historical data used

in Figure 1 where “α” is the pre-tax

figure he refers to throughout his book. The after-tax figure “αdt” that Piketty calculates in

his data set for Australia [Piketty-Zucman Wealth-Income data Set Australia – Table

3b] is about half the pre-tax figure used in

Figure 8 and it is reasonably constant through the whole period except

1999-2000 and 2005-2008 (when it was several percent lower). Using after-tax

figures in Figure 8 changes the position of the curve but not its shape. The

actual rate of return estimated from the bank funding rate is plotted on an

annual basis.

The plot for

Piketty’s “r” in Figure 8 gives an irrational result. An average rate of return

“r” over the entire wealth (net national capital) base of 16% as shown in

Figure 8 for New Zealand in 2013 is impossible when mortgage interest rates

there were less than half that. In

New Zealand’s gross

national income in 2012 was NZ$ 198b, so “α” was then about 53/198 or a

little under 27%, close enough as a first approximation to the 30% Piketty considers as a “typical” figure for

developed countries. Figure 8 therefore

gives a rational representation of Piketty’s “r” (before tax) as long as “α”

is reasonably close to 30%.

Piketty’s “α”

was also checked for an “extremely” high interest year (1988) when the Gross

national income (NI) in New Zealand was NZ$54.5b, total debt was NZ$57b, and

the comparable return on capital (from Figure 8) was 14.3%. Assuming similar

proportioning of investment returns in 1988 as in other years, the capital

income/national income ratio “r” would have been closer to 35% producing a

small peak in the Piketty “r” graph as shown on Figure 8 during the 1980’s.

This is much too small to affect the conclusion presented above that Piketty’s

“r” is unrelated to the actual annual rate of return on capital.

Figure 9 plots the

rate of return “r” (after tax) taken directly from Piketty’s data set for

Australia [Piketty-Zucman Wealth-Income data Set Australia – Table 3b] over the

last half century using Piketty’s two laws independently. The two laws give

completely different results proving that at least one of them is false.

5. VERIFYING THE SECOND LAW

Piketty says (p48)

that wealth is net of “the total amount

of financial liabilities (debt)” and that agrees with the approach taken in

the capital stock calculation used by the New Zealand Department of Statistics.

Figure 9.

Piketty’s book

hinges on the “U” shape in national capital over the period from the start of

WW1 to just after WW2 [Book Figures 3.1, 3.2]. He writes that that “U” shape is

due almost exclusively to war debt and wartime inflation and the effects of the

1930’s depression. For example, average inflation in

How the change in

wealth came to form Piketty’s “U” is set out below without using either of his

“laws”.

The two source

papers [Manning 2012, Manning 2013a] suggest that the

cumulative outstanding productive investment principal at cost ∑P and the

accumulated saving ∑st are both numerically equal to nominal

GDP as shown in Figures 4 and 5.

Both Piketty’s “st”

and Saving “s” must be after-tax figures

because government spending is already included in “total consumption” in the

national accounts. The principal repayments actually paid by firms are physical

monetary flows whereas the residual Saving recorded in the national accounts is

an accounting abstraction, despite the strenuous efforts made by statistical

authorities to generate an appropriate figure for “Consumption of Fixed

Capital”. For an example of those efforts see “Measuring Capital Stock in the

New Zealand Economy” 3rd Edition, published by Statistics New

Zealand,

Nobody pays

anything called “consumption of fixed capital”. Instead, principal is repaid on

capital items bought, in addition to interest. The repayments on productive

assets must be funded from the gross operating surplus resulting from business

activity in the productive sector. Payments of interest and capital relating to

non-productive investments like housing must come from the work incomes of

income earners: typically from wage increases generated by higher labour

productivity.

Capital repayments

in the productive sector must be more than the amount shown in the national accounts

for the consumption of fixed capital. If that were not so, the banking system

would have no residual security over the capital items they have funded as

those assets approach the end of their useful life. For example, commercial

vehicles have a scheduled life of around 7 years, but are typically paid off

over 5 years or less. Residential buildings are allocated a 70 year life cycle,

and are frequently paid off over 20 to 30 years. The “Savings” “s” in the SNA

accounts, on the other hand, merely reflect post depreciation (amortisation)

asset values which comprise tax-based accounting entries. Real residual

monetary values are shown by the purchase price less actual repayments.

Once an appropriate

correction to the consumption of fixed capital is made for those actual capital

repayments, the SNA saving should equal the increase in productive capital

(Gross capital formation less capital repayments) at current (typically

inflated) prices. That is the basis of the Savings Myth [Manning 2011b]. SNA Saving

“s” should be the net new capital creation and that must also equal nominal GDP

growth as shown in Figures 4 and 5.

Theoretically at

least, the productive economy is a closed circuit of financial flows where real

financial surpluses are used to fund gross fixed capital formation at cost

(Manning 2013a). That re-investment creates debt, either to the income earners

and businesses who have produced the assets or to the banks. The resulting

deposits attract interest that contributes to systemic inflation.

Further research is needed to confirm how the

additional principal repayments (total principal repayments – consumption of

fixed capital) added in Figure 5 to the figure for “consumption of fixed

capital” could (or should) be shown in the national accounts. The total

principal repayments would be recorded in the national income and outlay

account (Table 3.2) where “consumption of fixed capital” is shown now, reducing

national disposable income. The gross operating surplus (with GDP and gross

fixed capital formation) may therefore be understated in the income and

expenditure account of the national accounts (Table 3.1). The residual “Saving”

“s” would then consequently increase by the same amount in the national income

and outlay account to rebalance the accounts. Otherwise the additional capital

repayments would suppress consumption as a percentage of GDP and mask the

systemic inflation discussed in the source papers. Masking (from somewhere)

seems to be a primary reason the observed CPI inflation as it is

customarily reported in statistics is

less than the systemic inflation discussed in the source papers. The suggested

changes would not affect real economic

growth. They would affect nominal reported GDP growth and the way inflation

is reported.

The national

accounts produced under the System of National Accounts (SNA) are only as

accurate as the data on which they are based and the data series are constantly

being reviewed. For example, the

Quite apart from

required amendments to the data used in the national accounts, Saving in the

national accounts is independently subject to wide margins of error because it

is a small number resulting from subtracting much larger numbers each of which

is itself subject to considerable error. That is especially the case when

Saving “s” is small.

Compulsory savings and pension schemes add to

the “saving” problem because they reduce demand in the productive economy unless

all the withdrawal of purchasing power they cause is re-invested in new capital

goods. If that re-investment does not occur the withdrawals become part of

nominal “saving” that is diverted into investment sector inflation. This is

because the hoarded “saving” is either left in bank accounts at interest or is

added to the deposits used to trade existing assets in the non-productive

sector. Indeed, in the case of

Since the deposit

investment pool (the total financial

deposit base less the relatively small amount of deposits used in the physical

production of goods and services) follows

GDP (after substituting actual repayments for depreciation) [Manning 2012,

Manning 2013a] a percentage increase in GDP (Piketty uses national income Y)

tends to produce a similar percentage increase in wealth however that wealth is

calculated. If the investment pool

deposits increase by 10% all investment prices in aggregate, including the

prices of non-produced capital, will also increase assuming the proportion of

active investment in equities, property and bonds, remains constant. If, on the

other hand, investors withdraw from active trading in existing assets thereby

increasing the proportion of passive interest-bearing deposits, the circulating

pool of active deposits used for investments will fall and so will investment

prices. Shifts between the investment categories can also occur with changes in

public policy, taxation, or external events.

Investment in the

productive economy, as it must do, creates nominal GDP growth derived from

multiplying price “P” and production “Q” in the Fisher equation (MV=PQ) where M

is the money supply and V is its speed of circulation. It does not separate out

inflation. The new debt used to purchase new capital assets determines wealth

growth. Figure 7, which refers to

The most extreme

case of low growth and high saving in New Zealand was in 1980 when saving “s”

was 16% of GDP and economic growth was -1.7%! During the high inflation period

the gross operating surplus (and with it gross fixed capital formation) soared

while “old dollar” principal repayments were being made in rapidly inflating

currency. The high interest rates were bound to produce a very large national

account “saving” figure that was obviously not all spent on creating real

growth, especially in years like 1980. Instead “s” in those years represented

productive sector inflation.

After replacing actual principal repayments for the

existing “consumption of fixed assets” in the national accounts “SAVING”

=NOMINAL GDP GROWTH in the productive economy.

External deficits occur in

debtor countries when investment income and current transfers from the rest of

the world are negative there. Their effect is to dynamically reduce the

national disposable income (and ultimately domestic production and consumption)

unless the loss of purchasing power in the debtor country is replaced by new

debt. That is a primary reason why the domestic debt level in debtor countries

like New Zealand (which runs a large and persistent current account deficit) is

often much higher than the domestic deposit base.

Current account

deficits reduce the Gross National Income in debtor countries and increase it in

surplus countries. The deficits in debtor countries are funded from new

domestic private debt there. In perfectly “free” capital markets the resulting

deposits in creditor countries are returned to debtor countries as foreign

capital investment (foreign ownership of the debtor nation’s businesses,

property, land and resources). The net balance between domestic debt and

domestic deposits at any time can be readily seen from the credit and monetary

aggregate reconciliations published monthly by central banks the world over.

Returning deposits must create an investment bubble (as discussed in section 8)

to the extent they are invested outside of the debtor country’s productive

economy in existing capital assets like housing and other property.

Mixing production

and consumption figures with capital outlays as the national accounts do in the

SNA system is also problematic because it obscures the underlying financial

system mechanisms. Production and consumption cycles in the real economy

require very little money (very roughly half of the monetary aggregate M1)

because, conceptually, the same money is recycled many times each year [Manning

2012]. On the other hand, new capital items have to be fully funded from

incomes and the gross operating surplus in the Gross domestic product and

expenditure account, (Table

In earlier times,

under the “savings and loan” economic model, the debt to purchase new assets

was provided by savers. That increased

the debt

base by the same amount as in the present system but not the deposit

base. There were therefore relatively fewer new deposits available to

inflate the investment sector. The extent of asset inflation then became a

function of the speed of circulation of the available deposits as discussed

below.

Asset “values”

making up the total national wealth cannot be linked to the productive economy

the way Piketty attempts to do.

For example, the

national capital accounts record changes in the net value of produced capital assets. Statistics departments

construct various tables for what they define as “capital stock”, such as Table

4.3 of the

If a broad net

national capital (wealth) figure for New Zealand made up of the net national

stock from the national accounts plus all the other excluded assets referred to

above is used, “β” for New Zealand in 2013 indeed comes out at about 6 as

Piketty suggests, but he fails to explain how the assets he has included

in the national capital are obtained from his aggregate saving “s”. In his

dataset for

The

Piketty’s (s/g)

calculation for

Piketty’s “second

law” is therefore false. His “β” is not a function of (net saving st

/real growth gt). It is

instead a function of net saving.

{kind=link}

Note: “β” for

In practical dollar

terms, all price is inflation [Manning 2011a, Manning 2013a].

“Growth” is a

representation of new production added by population and productivity

increases. New production relates solely to the quantity of goods and services, not to their price [Manning

2011a].

Looking at the long

run, as Piketty says we must do, all production is derived from

growth because in the “beginning” there

were few people and little money and, apart from a few short interludes, no

inflation at least in England, over a period of some 600 years. The main

inflation interludes in England prior to WWI were first the plague that halved

the population there during the second half of the 14th century

thereby doubling the per capita money supply (though at that time the majority

of working people were still serfs), secondly the currency debasement of the

mid Tudor period 1546-1583, and thirdly during the Napoleonic wars at the end

of the 18th century. At those times most of the English economy was

still unmonetised. Even in 1800, 70% of

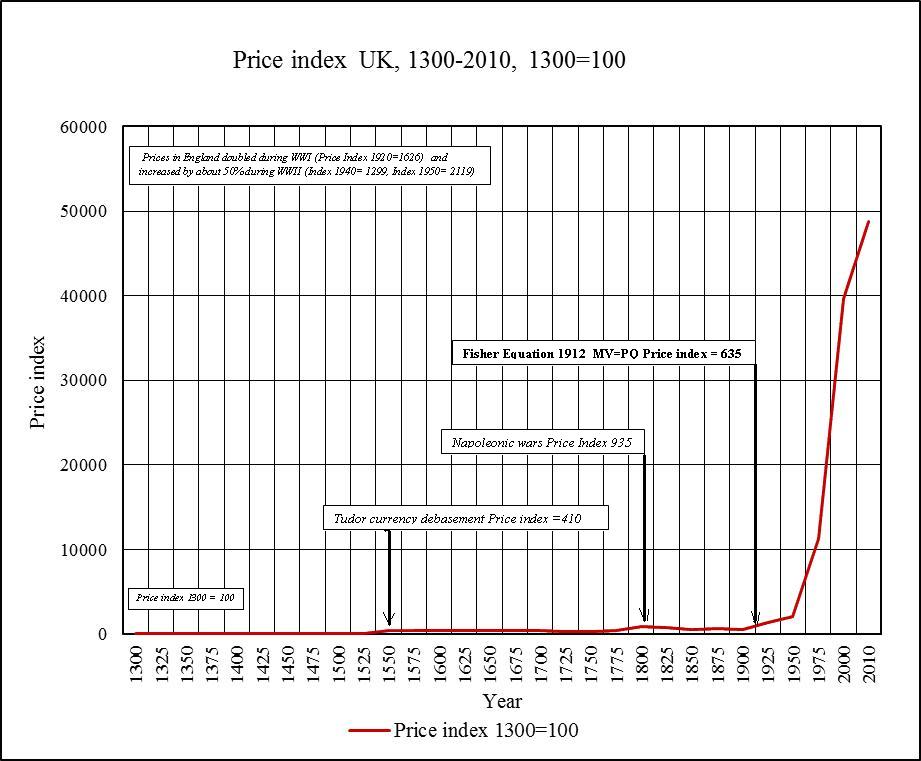

Figure 11 shows inflation for

In

The opposite argument applied during the depression

years and wartime period when wealth “values” were destroyed first through

business and bank collapse, then by wartime destruction and military

consumption. As prices rose during wartime, the purchasing power of (some of)

the rich declined because government imposed interest rates and

capital controls meant that the purchasing power and “wealth” of the

rich fell in nominal terms. Rapid inflation increased nominal incomes and

saving among workers without the corresponding relative capital growth accruing

to the rich. There is nothing magical about that and no “fundamental laws” are

needed to explain it. The phenomenon is clear from Figure 10 where “β” in

Stabilising “β” is simply

a matter of ensuring (s=g), that is, that the money supply (domestic deposits)

increases only in line with increased real production. At that point the domestic deposit base

increases at the same rate as real GDP and other things being equal:

For stable investment prices inflation must be zero

and, using Piketty’s terms, the rate of return “r” on total wealth must then be

(r = g/ β)

Figure 11 : CPI

(Consumer Price Index) England 1300-2000.

{kind=link}

Sources:

Inflation figures 1800-2000: O’Donoghue J, Goulding L (Office for National

Statistics Great Britain). Inflation figures 1300-1800 from Gregory

Clark “The Price History

of English Agriculture, 1209-1914” and Allen G, (House of Commons

Library) “Consumer Price Inflation since

6.

RECONCILIATION OF GROWTH, SAVING AND INFLATION

The concepts of

growth, saving and inflation will now be reconciled with each other.

Nominal GDP growth

includes inflation. Production resulting from previous growth costs more each

year in nominal terms as inflation increases. Each year after the growth first

takes place (and when new assets are created) inflation “revalues” the current

monetary worth of that growth. The revaluation is always positive except in

recession and depression years.

In Figure 12 the

growth figures for

GDP measures

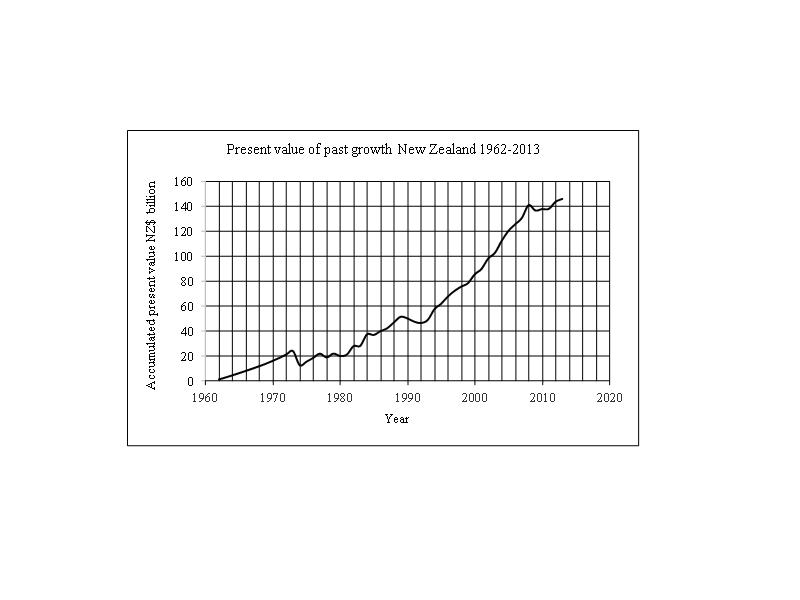

present growth plus all past growth at current prices.

Figure 12. Reflated

growth figures New Zealand 1962-2013.

{kind=link}

One primary reason

there was so very little growth through the middle ages was that there was very

little money. Much of what there was was physically hoarded and not invested

because there was virtually no inflation and very little to invest in. As

Piketty says, until the industrial revolution, most wealth was inherited not

earned.

This is because

according to the Fisher equation (M*V = P*Q)

[see Fisher, I (1912) “Elementary Principles of Economics”] GDP relates

to the quantity of goods and services Q the economy produces

multiplied by its price P. (GDP = P*Q).

“Q” is independent of “P” so that a smaller “Q” means lower GDP unless

there is an offsetting rise in “P”. In

the Fisher equation “M” is the money supply and “V” is its speed of circulation

While the Fisher

equation is typically applied to the productive economy it can equally well be

applied to the investment sector in relation to national capital where a

subscript “i” is added to the Fisher parameters M,V,P,Q to indicate the

investment sector as distinct from the productive economy.

The “value” of national capital is then determined by

the available investment sector funding, being the deposit base excluding money

needed for physical production of goods and services and its velocity of

circulation “Vi” as required by the Fisher equation (PiQi=MiVi), where:

“PiQi” is the traded

“output” or investment sector

“GDP”, the “value” of national capital

exchanged over a given period,

“Mi” is the

available investment sector money supply and

“Vi” is the

transaction velocity of that investment sector money.

That approach

allows the change in net national capital to be calculated at any point in time

as long as the asset elements and their respective prices are identified. For

example, the cumulative traded “value” of tradable assets “PiQi” might be

$100b, “Mi” about $200b and “Vi” about 0.5. If “Mi” increases by 10% while “Vi”

remains constant, “MiVi” would increase by 10% to $110b and the national wealth

(reflected by market prices) would also increase by 10%.

A similar approach

applies to saving too. Nominal GDP appears to be the cumulative sum of past

investment measured as the difference between gross capital formation and

principal repayments, that is, the outstanding productive sector debt [Manning

2013a, Manning 2012]. In short, production increases with investment in the

productive sector. No investment there means little or no monetised production.

Even the servants and labourers in pre-industrial times used (expensive) tools

and materials when they produced goods and services.

New Zealand GDP was

NZ$ 211 billion in 2013 and accumulated SNA “saving”, was NZ$ 169 billion. As previously

demonstrated in Figure 5, the difference

of NZ$ 42 b between GDP (NZ$ 211 billion) and accumulated saving (NZ$ 169

billion) represents the additional capital repayments physically made over and

above the “saving” figures, net of inflation, presently recorded in the

national accounts.

The reason

productive investment principal is closely related to GDP is conceptually very

simple. Tools and equipment wear out and infrastructure and buildings have to

be replaced, so that past saving lives on in current capital expenditure (gross

capital formation). New investment

replaces old investment as recorded by “consumption of fixed capital” in the

national accounts. It may be qualitatively different but in principle it

produces the “same” amount of output Q. Since the value of new productive assets is included in GDP figures, the value

of the increase in new capital stock cannot exceed measured GDP growth. Investment

is

growth because it generates new production. If that were not so the investment

would not be made.

The “missing” 20%

or so of GDP (see Figure 5, where a difference of 23% was assumed) referred to

above is predominantly due to actual repayments involving amounts over and

above the “age and efficiency profile” [depreciation or amortisation]

statistics departments use to define the consumption of fixed capital (and

therefore the residual “saving” figure “s” ) in the national accounts.

Housing is a

problem the world over because once it is constructed it is usually

economically unproductive. Servicing

the debt and principal repayments on it can only come from productivity

increases passed on as higher incomes to income earners or in the form of

reduced consumption with all its consequences for growth.

Housing has become

unaffordable for an ever increasing number of families because real disposable

incomes have not kept pace with real productivity increases (or sometimes even

with consumer price inflation) while at the same time inflation has increased

asset prices. Moreover, consumption patterns have changed with relatively more

disposable income spent on items that were previously “free” or un-monetised,

or on transfer payments associated with structural unemployment and welfare

caused by economic austerity policies.

The cost of living

has changed in ways that the consumer price index CPI fails to include.

The change in

affordability is dominated by inflation, that is, by interest rates. One

exception in recent times was when US financial institutions distorted the

The monetary cost

of maintaining the established productive base created by historical investment

and growth is very high. Once the investment price of a capital asset at cost

has been repaid, (and the initial value of the asset is fully depleted) it is

usually replaced. The replacement programme vastly exceeds new productive

capital investment which is why the figures in

Maintaining a

“savings” base to produce the current GDP output in

Cumulative

historical savings calculated as outstanding principal on productive capital

goods and cumulative historical growth at current prices are both equal to GDP.

They are flipsides of the same orthodox economic coin:

(Saving=Investment)

(S=I) where the investment is used to pay for the new

capital goods the economy produces.

7. WHAT IS CAPITAL?

Table 4.3 “Net

capital stock by asset type” found in the New Zealand Statistics Department

publication “Measuring Capital Stock in the New Zealand Economy” edition 3,

March 2013 indicates there is minimal net financial capital.

In the present

debt-based financial system, financial assets are generally offset by

counterpart liability. That is due to the double entry bookkeeping of the

banking system whereby (domestic credit = deposits + net foreign currency

holdings + bank equity + residuals). The secondary debt (on-lending) market

follows the same pattern.

This does not mean

financial assets in a debt-based financial system are evenly distributed among

the population. The opposite is true: broadly speaking the rich have the assets

while the poor have the debt.

National accounts

only include non-financial, produced, fixed assets. Piketty has not shown how

his national account-based factors “r”, “α” , “s”, “g” , that all relate

to about half of the national capital, can be extrapolated to form “net

national wealth” by way of his single multiplier “β”. Simple ratios such

as Piketty’s short term indicators (β= α/r) and ( β = s/g) only

confirm that the “value” of wealth is largely a function of inflation because

the value of national wealth “β” obviously includes both new and past

inflation.

The

At the same time,

unlike

In 2013, the

present value of the portion of New Zealand’s national capital measured in

Table 4.3 of the New Zealand national accounts was NZ$ 620b.

The material presented

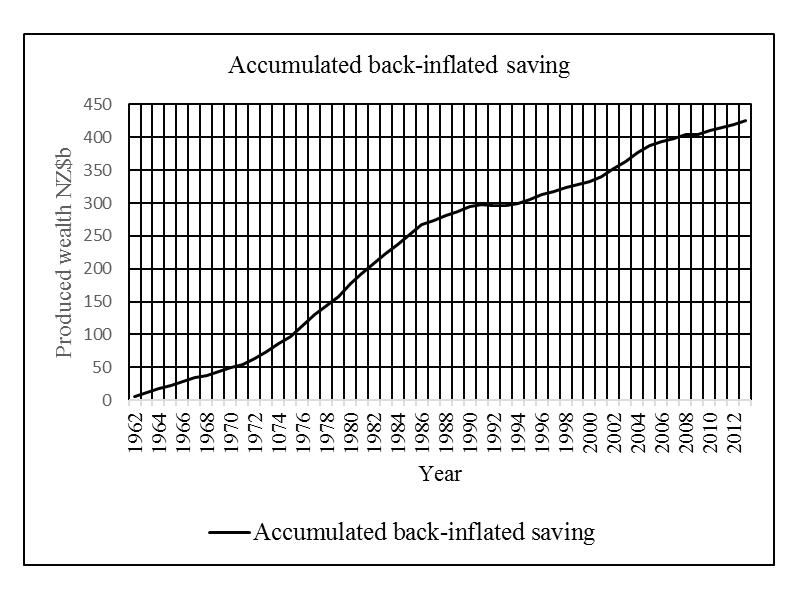

in this paper suggests that reflating the annual savings in the same way as was

done for past growth in Figure 13 gives a present value of produced wealth that

can be compared with the NZ$ 620b shown in the national accounts for 2013,

assuming the national accounts data is rational.

The accumulated

saving for

The revaluation

exercise for Saving gives a value of produced wealth in New Zealand from

1962-2013 of NZ$ 424.9b or 68.6% of the produced wealth figure shown in the

national accounts. That agrees well with the 67.5% of GDP provisionally

obtained for accumulated growth over the same period. The proportion would

probably remain similar were Saving upgraded to take account of capital

repayments as discussed in section 5 because the accumulated growth in Figure

12 would also be higher.

Figure 13. Accumulated

back-Saving = Produced Wealth New Zealand 1962-2013.

{kind=link}

(lowellpiketty13)

Total produced

wealth is the accumulated present value of past Saving.

As a corollary, the “value” of

“all wealth” in the absence of bubble debt (section 8) appears to be the

present value of past Saving proportionately extended on the basis of supply

and demand through market transactions to apply to intangible and non-produced assets.

8. INEQUALITY AND BUBBLES

The previous

sections of this paper describe the physical accounting relationships between

growth, nominal GDP, saving and wealth.

Using a similar

approach to the one already used above for past growth, produced capital (wealth)

appears to be the present value of past increases in nominal GDP as set out in

section 7 above.

That produced

capital is owned by households and businesses that collectively make up the

private sector, and the government. In

New Zealand (from National Accounts Table 4.3) about half the produced capital

(about NZ$ 300b of the total of NZ$ 620b in 2013) is in the form of residential

buildings while the rest is non-residential buildings, other construction,

transport equipment, plant, machinery and associated equipment and some less

tangible assets.

The total net financial

wealth owned by households in

Where there is

practically no longer interest paid on deposits, as in the world’s major

economies like the US, Japan and much of the EU, inflation is very low and

wealth there is expanding slowly if at all.

There is still some

inflation in the

When deposit

interest rates are zero there is no financial transfer from borrowers to

deposit holders and therefore no systemic inflation (Manning, 2012). Paying

interest to deposit holders means deposit holders literally get something for

nothing. That is the biblical definition of usury. The rationale for offering

interest on most deposits is twofold: first to protect holders from inflation

and secondly to pay deposit holders for “risk” even though there should be

little or none in a stable modern banking system. Protecting deposits from

inflation through interest rates is a myth because the source papers (Manning

2012, Manning 2013a) show that the interest itself is the cause of systemic

inflation. The higher the interest rate, the higher the inflation, as is

obvious from a cursory glance at any developed country data set from the time

US President Nixon abandoned the US$ gold peg (August 15, 1971) through the

resulting 1970’s oil shocks until the Basel I accords were implemented in the

late 1980’s. In recent decades, banks have paid competitive interest rates to

depositors so as to maintain central bank reserves (liquidity) as required

under international banking rules. If they do not pay enough interest their

deposits will shift to other banks that pay more. This would create a liquidity

crisis because they would not be maintaining enough reserves at the central

bank to cover perceived banking risk.

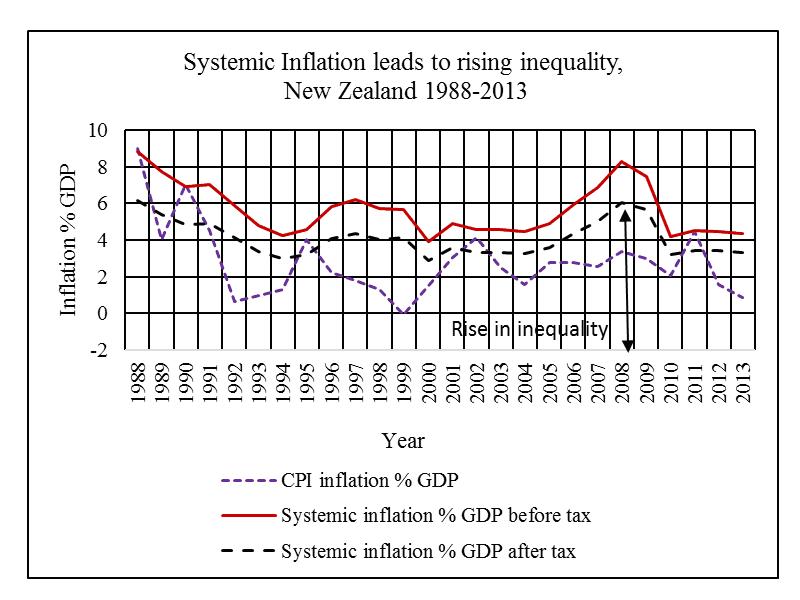

Figure 14 shows how

wealth and inequality develop (in the absence of Quantitative Easing provided

to financial institutions). The difference between the systemic inflation after

tax and CPI inflation shown in Figure 14 seems to be the combined effect of

orthodox non-productive saving as described in Section 6.

Figure 14.

The source of inequality in New Zealand

1988-2013.

{kind=link}

(lowellpiketty14)

Central banks set

the floor for interest rates by (arguably, arbitrarily) establishing a base

rate at which they will lend fresh liquidity to their participating commercial

banks. Raising or lowering that rate effectively controls lending rates to

borrowers because, when the price for new money rises, borrowers are unable to

borrow as much as they could before, and, overall, new lending falls.

The fundamental

issue is that, in aggregate, the borrowers are not the same group as deposit

holders. If borrowers already had deposits,

they would not typically be borrowing more because it costs much more to borrow

than it does to use their existing deposits. Interest rates for borrowing are

always higher than deposit rates by an amount equal to the bank spread (the

difference between the borrowing or “claims” rate and the “funding” or deposit

interest rate).

Inequality

increases in proportion to the debt held by an ever-increasing number of poor

people relative to the corresponding deposits held by an ever-decreasing number

of rich people.

The process of the

concentration of deposits in ever fewer hands is gradual. That is why Piketty

says inequality has to be viewed over the long term. Just as there is a close

association between growth, savings, GDP and “wealth” there is an equally close

association in debt –based financial systems between domestic credit

(debt), the money supply M3 (excluding inter-institutional lending or “repos”)

and GDP. The relationship has become clearer as the influence of cash

transactions in generating economic activity has fallen to very low levels in

industrialised countries. When cash was “king” some investments could be made

from hoarded cash outside the debt-based banking system. That is why from 1900

or earlier until 1990, the ratio (GDP/M3) in

The increase in

MONEY relative to GDP has directly caused asset inflation and that increase is

itself caused by deposit interest together with (some) bubble debt.

This gives

practical substance to Fulbrook’s profound observations (Fullbrook,2014

p7) That “any increase in the market value of either K [capital] or Y [income] decreases by an equal amount the market value of the other and vice

versa …… It is not an accumulation

that takes place when capital-2 increases, but rather an appropriation [His emphasis]. While this paper suggests that

his “K” would be limited to produced capital, it establishes his

notion of transfer or appropriation through saving and inflation from the

productive economy by the investment sector.

The two kinds of

saving Fullbrook refers to (Fullbrook, 2014 p8) are inflation, his “sv”,

the percent of savings going into existing assets, and growth, his “sr”,

the percent of savings invested in the productive economy.

As an example,

consider the monetary figures for

The M1 monetary

aggregate was: NZ$ 36.8 billion

M3 excluding repos

was: NZ$

256.1 billion.

The GDP was: NZ$

211.6 billion

The

Subtracting GDP

from M3 left a residual of NZ$ 44.5 billion.

If that residual

were reduced by the non-interest-bearing transaction account total M1

(including cash in circulation), which was NZ$36.8 billion in 2013, only NZ$7.7

billion (just 3.6% of GDP) would remain unaccounted for in systemic inflation.

That sum unaccounted for represents “bubble” debt, being new debt and its corresponding deposits

generated by the banking system outside the productive economy, for

example, to pay the outflows resulting from current account deficits when a

country is importing too much and living “beyond its means”.

Much (but far from

all, in

The real “bubble”

in

Further research is

needed to accurately identify the true “bubble” balance but the M1 balance

shown in the New Zealand Reserve Bank data for 2013 should probably be reduced

by:

a) Most cash in

circulation (say NZ$ 3 billion of a total of NZ$ 4b), which is mostly hoarded in the informal

economy (in the drug trade and other

illegal activities)

b) The deposits used in

productive transaction accounts to physically generate GDP that the author

estimates at about 5.5% of GDP or NZ$ 11.6 billion

c) The transaction deposits used in the investment

sector to physically generate the transfer of existing assets (say 2.5% of GDP

or NZ$ 5.3 billion)

The total of (a),

(b) and (c) is NZ$ 19.9 billion which is much less than the M1 monetary

aggregate of NZ$ 36.8 billion shown in the example above for

That suggests

therefore, bearing in mind the relationships between GDP, savings, and

“wealth”, that the entire wealth base in

That is not the end

of the story, either, because

The reverse applies

to surplus countries like

Plainly, in the

case of “bubble” deposits, deposit interest accrues to those who sold their

domestic assets in return for their bank deposit. From that point on, they miss

out on subsequent capital gains from the increase in the price of the asset

they have sold, but they retain the capacity to buy another asset, while the

deposit remains permanently in the financial system unless or until the

corresponding original debt has been repaid. On the other hand, as far as

foreign investment goes, the accumulated net foreign asset imbalance can only

be rectified by reducing the debtor country’s current account deficits. As long as the current account debt keeps

growing, so does the investment “bubble” it has created, leaving the debtor

country at constant financial risk.

Over time, the

investment sector (taking New Zealand as an example) has expanded beyond the

economic growth rate by an amount equal to the inflation represented by the

difference between real economic growth on the one hand and (nominal GDP plus

the added impact of “bubble” debt as described) on the other.

Since

The amount of

interest transferred from borrowers to subsequent deposit holders from the two

sources described above is an accounting identity that can be quantified at any

point in time. Its direct result in

That is why so many

economists and officials in debtor countries like

Piketty among

others observes that unequal wealth distribution is also growing from absurdly

high “earned” incomes. While that is true and those “earned” incomes further

distort the distribution of wealth and increase inequality, they are not

themselves the cause of wealth “generation”. They are a “normal” part of

productive sector GDP and their effect on wealth inequality can be addressed by

more appropriate progressive taxation .

9. CONCLUSION

Piketty’s “golden rule” and his “laws” do not

withstand scrutiny. His own data

set for

The heart of Piketty’s book and his “laws” is that the

percentage (r-g) gives rise to a capital-based unearned income that is surplus

to the monetary requirements of the productive economy. That surplus income is created through

inflationary deposit expansion that forms part of Saving “s” in the SNA system

of national accounts.

Contrary to Piketty’s

claims, wealth is transferred upward through the deposit interest rate

mechanism whereby the net interest paid by original debt holders under their

debt contracts finds it way as unearned income to current deposit holders’

accounts. That unearned income is funded from nominal GDP growth and directly

confers higher values on all traded national

capital in both the productive economy and the non-productive investment

sector.

Inflation coupled

with interest rate controls and high taxation caused the “U” shapes in the

“β” graphs (national capital/national income) shown in Chapter 3 of

Piketty’s book. Neither of his “fundamental laws” explains the historical

events he refers to in his book.

After replacing

principal repayments for the existing “consumption of fixed economy assets” in

the national accounts “SAVING” =NOMINAL GROWTH in the productive sector.

GDP = the sum of

existing outstanding productive investment principal.

GDP =the

accumulated present value of all past real GDP growth in the productive

economy.

Produced capital

(wealth) = the accumulated present value of all past saving.

National capital

(total wealth as defined by Piketty) = the value of produced capital extended

to include produced intangible and non-produced assets. It is determined

directly by the size of the domestic deposit base (including deposits resulting

from bubbles).

In the absence of

bubbles, asset inflation will cease when deposit interest is zero.

In the absence of

bubbles (and only then ), using Piketty’s terminology, when deposit

interest rates are zero the rate of return “r” on the national capital will be

the economic growth rate (gt/ β). At that point, using Piketty’s typical

figures for “β” of 6 and “g” of 2%, “r” would be just 0.33%, not the 5%

Piketty refers to throughout his book.

Many developed countries with low interest rates

referred to in Piketty’s book may already have a rate of return “r” on national

capital of less than 1% because national capital is a function of deposits and saving,

not “growth”.

10. REFERENCES

(All the papers by

Manning L are published at www.integrateddevelopment.org)

Manning L 2011a,August 2011)“The Interest-Bearing debt System and its

Economic Impacts”v. 5 Interest-bearing debt system and its economic impacts.

(Revised edition).

Manning L 2011b (September 2011) “The Savings Myth” v.

7

Savings Myth. (Revised

edition).

Manning L (October 2012) “The

Missing Links Between Growth, Saving, Deposits and GDP” v.3

Missing links between growth, saving, deposits and GDP.

Manning L 2013a

(February 2013) “The DNA of the Debt-Based Economy” v.3

DNA of the debt-based economy.

Manning L 2013b (April

2013) “Capital is Debt”

Manning L 2013c

(September 2013) “The End of Capitalism: Systemic Collapse” v.2

The end of capitalism : Systemic collapse.

Piketty Thomas, “ Capital in the Twenty-First Century”

English translation by Arthur Goldhammer, Belknap Press of Harvard University

Press, 2014

Piketty Thomas & Zucman Gabriel, “Capital is Back:

Wealth-Income Rations in Rich Countries”

July 26,2013. piketty@pse.ens.fr zucman@pse.ens.fr

Fulbrook Edward, “Capital and capital: the second most

fundamental confusion”, Real World Economics review, issue no 69, pages

149-160, 2014.

A. ORIGINAL PAPERS IN ALPHABETICAL ORDER.

NEW : Beyond Piketty : The Anatomy

of Inequality.

Beyond Piketty : The Anatomy

of Inequality.

Debt bubbles cannot be popped : Business cycles are policy inventions.

DNA of the debt-based economy.

General summary of all papers published.(Revised edition).

How to create stable financial systems in four

complementary steps. (Revised edition).

How to introduce an e-money financed virtual minimum wage

system in New Zealand. (Revised edition) .

How

to introduce a guaranteed minimum income in New Zealand. (Revised edition).

Interest-bearing debt system and its economic impacts.

(Revised edition).

Manifesto of 95 principles of the debt-based economy.

The Manning plan for permanent debt reduction in the national economy.

Measuring nothing on the road

to nowhere.

Missing links between growth, saving, deposits and

GDP.

Savings Myth. (Revised edition).

Unified text of the manifesto of the debt-based

economy.

Using a foreign transactions surcharge (FTS) to manage the

exchange rate.

(The

following items have not been revised. They show the historic development of

the work. )

Financial system mechanics explained for the first time. “The Ripple

Starts Here.”

Short summary of the paper The Ripple Starts Here.

Financial system mechanics: Power-point presentation.

B. REVIEWS.

Analysis of Jackson, A., Dyson, B., Hodgson, G. The Positive Money

Proposal – Plan for Monetary Reform, Positive Money,

Analysis of the New Zealand Initiative (NZI) paper by B.

Wilkinson : New Zealand’s Global Links : Foreign Ownership and the Status of

New Zealand’s Net International Investment. (Posted 11 May, 2013.)

Chicago Plan Revisited Version II: An insufficient

response to financial system failure. (Posted 11 May, 2013.)

Comments on the original IMF (Benes and Kumhof) paper

“The Chicago Plan Revisited”. (Posted 20 August, 2012.)

C. ARTICLES.

The end of capitalism : Systemic collapse. (24

August, 2013).

Increases in export income from price rises abroad are not

growth. (26 August, 2013).

There’s no such thing as affordable housing. (15 June, 2013).

What about a tax cut for the poor? (16 May,

2013).

D. OTHER.

Carroll,

W.K.; Sapinksi, J.P., The Global Corporate Elite and

the Transnational Policy-Planning Network, 1996-2006 : A Structural Analysis,

International

Sociology, Vol. 25 no. 4 pp. 501-538, Sage Publications,

Vitali

S. et al, The network of global

corporate control. Swiss Federal Institute of

Technology (ETH), Zurich, October, 2011.

The Transnational Insitute (TNI),

For the domination of the financial lobby in

European decision making see Wolff, M. and others, The

Fire Power of the Financial Lobby : A Survey of the Size of the Financial Lobby

at EU Level, Corporate European Observatory

(CEO) with the Austrian Federal Chamber of Labour and the Austrian Trade Union

Federation IÖGB), Brussels, April 2014.

Understating reality by using minimal salaries and excluding event

organisation, travel costs and taxation,

some 1700 financial lobbyists working for 700 organisations (450 of which are

unregistered) spend € 123 million a year on lobbying EU institutions, 30 times

more than NGOs, Trade Unions and Consumer Associations together. They account

for more than 70% of lobby meetings with EU institutions and have dominated

with up to a 94% participation 15 out of the 17 “Expert Groups” on financial

topics, the exceptions being the two “users” groups.

Super-secret negotiations are under way which would

still further expand the almost unlimited dominating power of the finance

industry. See Wikileaks Secret Trade in Services Agreement, under

negotiation, Annex 10. For

preliminary comments on it see Kelsey J, Memorandum on the Leaked

[Secret] TISA [Trade in Services] Financial Services Text which is

also published by Wikileaks.

By every measure, the big

banks are [37%] bigger [than in 2008], S.Gandel, fortune.com,

Time Inc, 13 September, 2013.

![]()

This work is licensed under a Creative Commons

Attribution-Non-commercial-Share Alike 3.0 Licence..